Here are the key takeaways from the blog on GSTR 10:

Purpose of GSTR 10: GSTR-10 is a final return form required for businesses whose GST registration has been canceled or surrendered, ensuring all tax liabilities and stock details are cleared.

Who Needs to File: Businesses whose GST registration is canceled, either voluntarily or by the authorities, must file GSTR-10, except for Input Service Distributors, non-resident taxable persons, and composition scheme taxpayers.

Filing Deadline: The return must be filed within three months of the GST cancellation date or the issuance of the cancellation order, whichever is later.

Penalties for Late Filing: Failure to file on time incurs a penalty of ₹200 per day, divided between CGST and SGST, without a maximum limit.

No Amendments Allowed: GSTR-10 cannot be revised after submission, so accuracy is essential during filing.

Refunds: Businesses may claim refunds for unutilized input tax credits on closing stock or excess GST paid, if applicable.

Importance of Timely Compliance: Filing GSTR-10 on time avoids penalties, ensures compliance, and closes the GST account smoothly with no pending dues

GSTR-10 is a special return form that businesses must file when their GST registration is canceled or surrendered. It’s also known as the Final Return. This form helps the government keep track of any tax liabilities or stock that might still be there at the time of cancellation.

The purpose of filing GSTR-10 is to ensure that everything is cleared between the taxpayer and the government when the business is no longer registered under GST. This includes paying any remaining taxes and providing details about the closing stock.

Filing GSTR-10 is important because not doing so can lead to penalties and legal issues. It ensures that all tax dues are settled properly, and non-compliance could result in fines or other legal consequences.

Who Needs to File GSTR 10?

GSTR-10 must be filed by any taxpayer whose GST registration has been canceled voluntarily or by the tax authorities. This applies to businesses that decide to shut down or stop their operations, as well as those whose GST registration is canceled for other reasons, like non-compliance.

However, there are some exemptions to this rule. The following types of taxpayers do not need to file GSTR-10:

- Input Service Distributors (ISD): These are entities that distribute input tax credits to other units of the business.

- Non-resident taxable persons: These are individuals or businesses that do not have a fixed place of business in India but are required to pay GST for a short period.

- Taxpayers under the composition scheme: Those who have opted for the composition scheme, which offers lower compliance but restricts their business to a certain turnover limit, are also exempt.

For most regular taxpayers, GSTR-10 is a must when their GST registration is canceled. It helps close the GST account properly and ensures that no dues or liabilities are left behind.

Due Date for Filing GSTR-10

The due date for filing GSTR-10 is within 3 months from the date of cancellation or the date when the cancellation order was issued, whichever is later. This means that as soon as a business’s GST registration is canceled, they have up to 3 months to submit the final return.

It’s important to stick to this deadline because failing to file GSTR-10 on time can lead to penalties, late fees, and even legal action. The government considers this final return as a way to settle any remaining tax liabilities and ensure that all details related to the business’s GST are properly closed. Filing on time helps avoid unnecessary complications and keeps the compliance process smooth.

Consequences of Not Filing GSTR-10

If GSTR-10 is not filed within the stipulated time, businesses face penalties and further legal consequences. The penalties for late filing are ₹200 per day, which is split as ₹100 for CGST (Central GST) and ₹100 for SGST (State GST). This penalty continues until the return is filed, and there is no maximum limit to the late fees, which means the longer you delay, the more you have to pay.

In addition to penalties, if the GSTR-10 is not filed for an extended period, the tax authorities can take legal action, which may include issuing notices or even prosecution. Non-compliance can severely impact the business or taxpayer, leading to problems with future registrations, issues with credit scores, and difficulties with government compliance.

To avoid these complications, it’s essential to file GSTR-10 on time and ensure all tax dues are settled properly. Compliance not only helps avoid penalties but also maintains a clean record with the tax authorities.

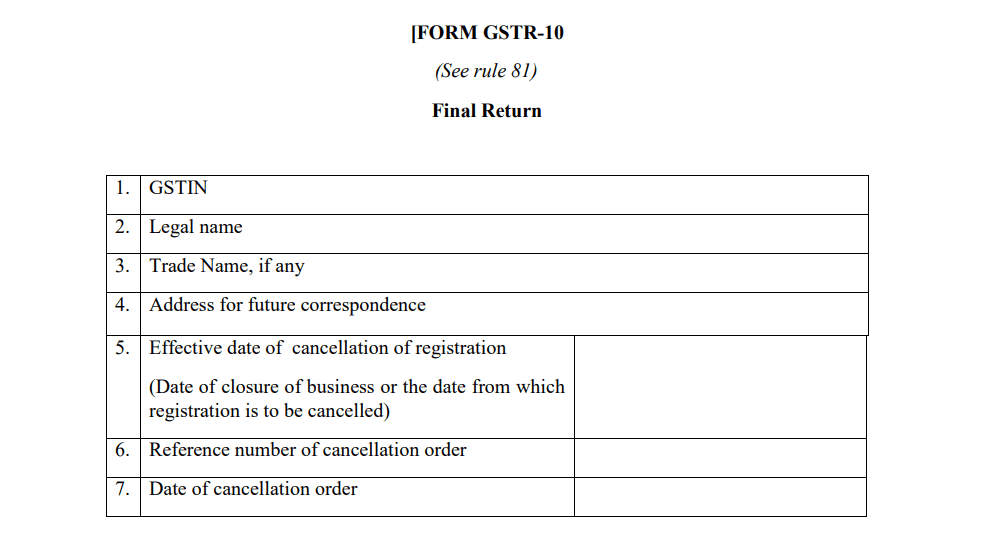

Information Required in GSTR-10

When filing GSTR-10, you need to provide specific information to complete the return accurately. Here’s a breakdown of the key details required:

- GSTIN (Goods and Services Tax Identification Number): Your unique GST registration number.

- Legal Name: The official name of the business or individual as registered under GST.

- Trade Name: If applicable, the trade name under which your business operates.

- Address for future correspondence

- Effective Date of Registration Cancellation: You need to mention the date on which your GST registration was canceled. This could be the date you voluntarily surrendered your registration or the date when the authorities canceled it.

- Reference number of cancellation order

- Date of cancellation order

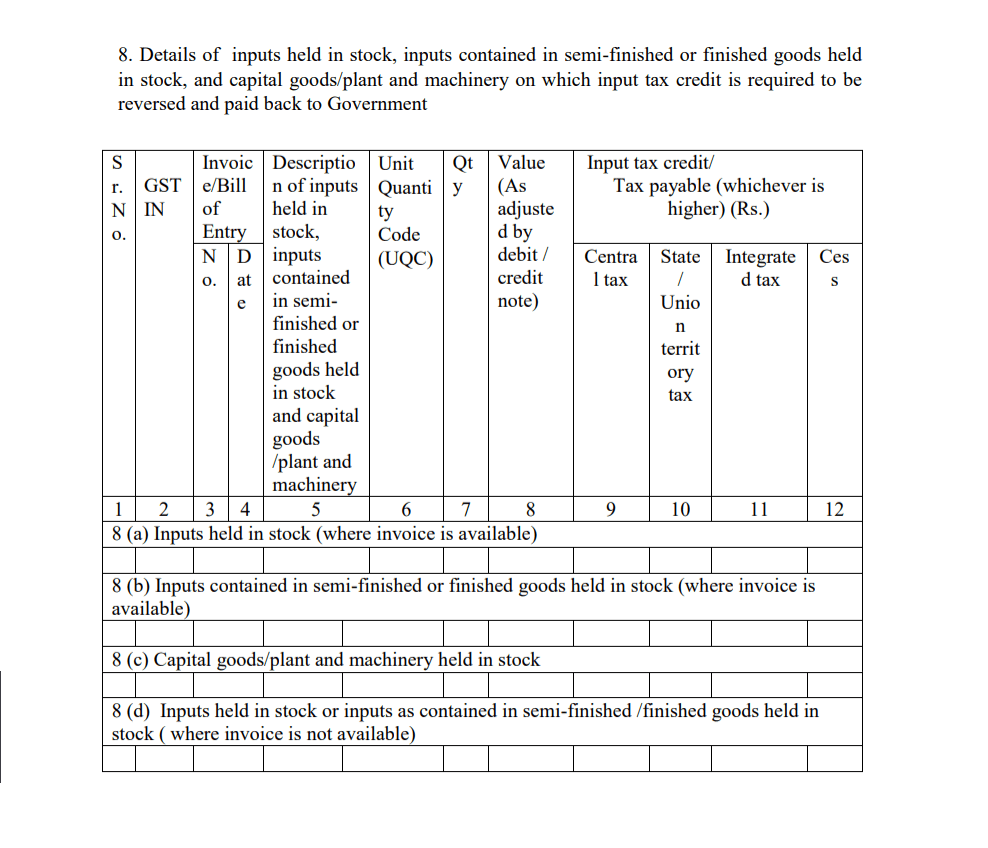

- Details of Closing Stock: The taxpayer must declare details of the closing stock on the date of cancellation. This includes:

- Inputs: Raw materials held in stock.

- Semi-finished goods: Partially completed products.

- Finished goods: Final products ready for sale.

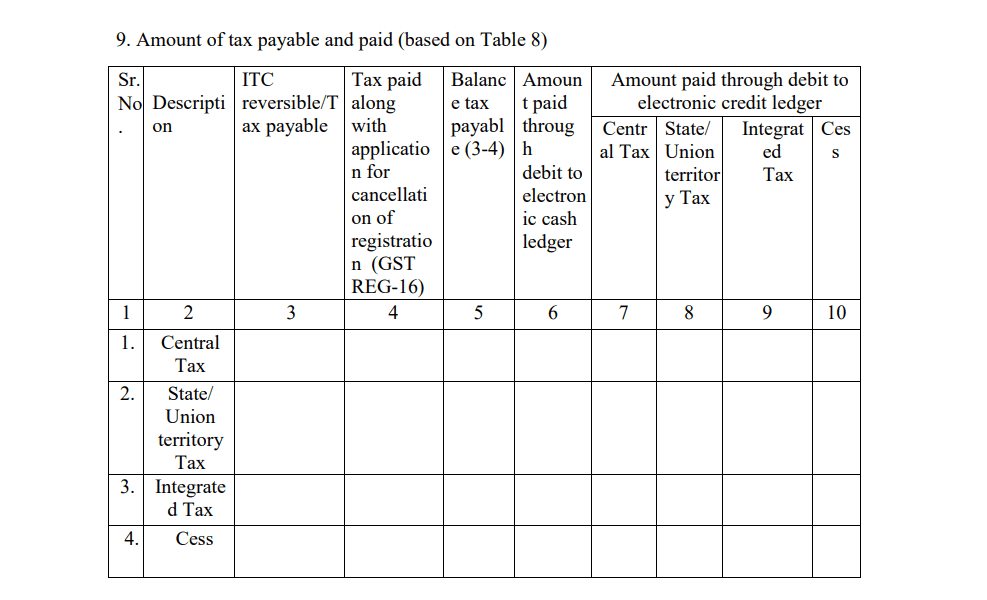

- Tax Liability:

- A summary of all tax liabilities that were due at the time of cancellation needs to be included. This helps settle any remaining tax amounts that the business may owe to the government.

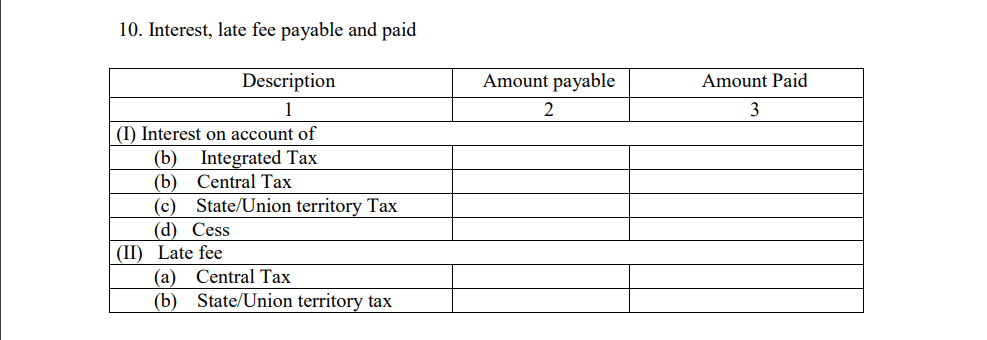

- Interest, late fees payable and paid

Providing all this information accurately ensures that your GSTR-10 is processed without delays and all tax liabilities are settled properly.

Steps to File GSTR-10

Filing GSTR-10 is a straightforward process that can be done online through the GST portal. Here’s a step-by-step guide to help you file your GSTR-10:

1. Log in to the GST Portal:

- Visit the official GST portal https://www.gst.gov.in/.

- Enter your valid credentials (GSTIN, username, and password) to log in.

2. Navigate to GSTR-10:

- Once logged in, go to the “Services” tab.

- Under “Returns,” click on “Final Return (GSTR-10)”.

3. Fill in the Required Details:

- You will see a form that asks for the details we discussed earlier, such as GSTIN, legal name, trade name, cancellation date, closing stock, tax liabilities, etc.

- Fill in these details carefully to ensure accuracy.

4. Preview the Return:

- After entering all the necessary details, review the information to make sure everything is correct.

- It’s important to preview the return before submission to avoid any errors.

5. Submit the Return:

- Once you are satisfied with the information, click on the “Submit” button.

6. File the Return with DSC or EVC:

- After submission, you need to authenticate the return. You can do this using:

- DSC (Digital Signature Certificate) for businesses, or

- EVC (Electronic Verification Code) for individual taxpayers.

- Complete the verification process and submit the return.

7. Make the Payment (if applicable):

- If you have any outstanding tax liabilities, the portal will prompt you to make the payment. Pay the necessary dues to finalize the filing.

8. Download the Form for Offline Preparation:

- Before filing, you can also download the GSTR-10 form from the portal. This allows you to prepare the form offline and then upload it when ready, ensuring a smooth filing process.

By following these steps, you can file your GSTR-10 easily and ensure that your GST registration is closed without any complications.

Common Mistakes to Avoid While Filing GSTR-10

Filing GSTR-10 is crucial, and making mistakes can lead to unnecessary complications. Here are some common errors to avoid when submitting your final return:

Not Declaring Closing Stock Properly:

Failing to accurately declare the closing stock (inputs, semi-finished goods, and finished goods) can result in legal issues. Underreporting the stock or failing to mention it correctly may lead to penalties or further scrutiny by the tax authorities.

Missing the Due Date:

One of the most frequent mistakes is missing the 3-month deadline for filing GSTR-10. Filing late leads to hefty penalties of ₹200 per day, and prolonged delays can invite legal action. Always ensure that you submit the return on time to avoid these fines.

Inaccurate Tax Liability Details:

It’s essential to make sure that all tax liabilities are cleared and reported correctly in the return. Errors in reporting your remaining liabilities can result in further taxes or penalties. Double-check your figures to ensure accuracy.

By avoiding these common mistakes, you can file your GSTR-10 without any problems and complete the closure of your GST registration smoothly.

Penalties and Late Fees

Filing GSTR-10 on time is crucial to avoid penalties and late fees. Here’s a breakdown of the penalties for missing the deadline:

Late Fees:

The late fee for not filing GSTR-10 is ₹200 per day.

₹100 for CGST (Central GST).

₹100 for SGST (State GST).

This fee is charged per day from the day after the due date until the return is filed.

Maximum Late Fee and Interest (if applicable):

While there is no specific maximum cap on late fees for GSTR-10, the longer the delay, the higher the amount you will have to pay.

In addition to the late fee, you might also have to pay interest on any outstanding tax liability that remains unpaid.

Compounding Effect of Non-Compliance:

If GSTR-10 is not filed for a prolonged period, the penalty amount can compound, meaning it can accumulate to a significant amount over time.

Moreover, continued non-compliance can trigger legal action from tax authorities, including notices, fines, and even prosecution in severe cases.

To avoid these costly penalties and legal trouble, it’s vital to file GSTR-10 within the given time frame and settle any pending tax dues promptly.

Amendments or Corrections in GSTR-10

Once GSTR-10 is filed, there is no provision to amend or revise the return. This means that any errors or omissions cannot be corrected after submission, making it crucial to get everything right the first time.

Here are a few precautions taxpayers should take before filing GSTR-10:

Double-Check All Information:

Ensure that all details, especially those related to closing stock, tax liabilities, and purchase/sales data, are accurate and up-to-date.

Carefully review the return form before submitting it, as mistakes cannot be corrected later.

Ensure Proper Calculation of Tax Liabilities:

Make sure all pending tax liabilities are fully settled and reported correctly in the return. Misreporting can lead to issues down the line.

Cross-Verify Documents:

Before filing, ensure that all required documents, such as invoice details and stock reports, match the information entered in the return.

Handling Errors After Filing

If you’ve made an unintentional mistake in GSTR-10, the only way to resolve the issue is by contacting the GST department:

- Reach out to the jurisdictional tax officer to explain the situation and seek advice on how to rectify the mistake.

- In certain cases, you may need to submit a formal letter of request or provide supporting documents to prove the unintentional nature of the error.

Since amendments aren’t allowed in GSTR-10, taking extra care during the filing process is key to avoiding future complications.

Refunds in GSTR-10

When filing GSTR-10, there are scenarios where a business might be eligible for a refund, especially during the GST cancellation process. One common case is the input tax credit (ITC) on closing stock. If the taxpayer has excess input tax credit that hasn’t been utilized, they may claim a refund of this amount.

Scenarios Where Refunds Can Be Claimed:

- Input Tax Credit on Closing Stock:

- If there is any unutilized input tax credit on raw materials, semi-finished goods, or finished goods, the taxpayer can claim this as a refund during the cancellation process.

- Excess GST Paid:

- In cases where the taxpayer has paid excess GST due to any calculation errors or adjustments, they can request a refund for the overpaid amount.

- Tax Refunds on Exports:

- Businesses involved in exports without the payment of IGST may claim a refund on the input tax credit related to these exports.

Process to Claim Refund Through GSTR-10:

- Declare Refund Amount in the GSTR-10 Form:

- While filing the GSTR-10 form, there is a section to provide the details of refund claims. The taxpayer should accurately declare the amount of input tax credit or excess GST paid that they are claiming as a refund.

- Submit Supporting Documents:

- Taxpayers may be required to submit supporting documents that justify their refund claim. These documents could include invoices, purchase records, and other relevant financial details that support the claim.

- Approval of Refund by Tax Authorities:

- Once the refund is claimed through GSTR-10, it goes through a verification process by the tax authorities. If everything checks out, the refund will be processed and credited to the taxpayer’s account.

Claiming refunds during the GST cancellation process is a key benefit for businesses, and it helps in recovering any unused input tax credit or excess GST paid. It’s important to carefully calculate and provide accurate information to ensure the refund process goes smoothly.

Conclusion

Filing GSTR-10 is a critical step for businesses that have canceled or surrendered their GST registration. It serves as a final return to ensure that all tax liabilities are cleared and that the business has no pending dues with the government. By filing GSTR-10, you formally close your GST account, providing clarity and legal compliance.

FAQ Section

Here are some common questions and answers related to GSTR-10:

Is GSTR-10 mandatory for all taxpayers?

No, GSTR-10 is only mandatory for taxpayers whose GST registration has been canceled or surrendered. It is not required for Input Service Distributors, non-resident taxable persons, and composition scheme taxpayers.

What happens if GSTR-10 is not filed?

If GSTR-10 is not filed within the due date, the taxpayer may face legal action and penalties. The late fees are ₹200 per day (₹100 CGST + ₹100 SGST), and continued non-compliance can lead to further consequences.

How can I check the status of my GSTR-10 filing?

You can check the status of your GSTR-10 filing by logging into the GST portal. Go to the “Returns Dashboard” section, and you can track the status of your filed returns.

Can I file GSTR-10 after the due date?

Yes, GSTR-10 can still be filed after the due date, but there will be late fees and penalties. The late fee is ₹200 per day, and it continues to accumulate until the return is filed.

Filing GSTR-10 on time is crucial to avoid penalties and ensure the smooth closure of your GST registration.

Related Posts:

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Everything To Know About GSTR 3

Everything To Know About GSTR 3

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

GSTR 6A: Everything You Need to Know

GSTR 6A: Everything You Need to Know

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

Complete Guide to GSTR-4A for Composition Taxpayers

Complete Guide to GSTR-4A for Composition Taxpayers