What is GSTR 3?

Right now, GSTR 3 is not in use, and businesses file GSTR-3B instead.

GSTR 3 is a monthly tax form that businesses in India file under the Goods and Services Tax (GST) system. It shows the total tax a business needs to pay for the month, based on its sales and purchases. It also tells how much tax the business can get back as a refund from its purchases.

Businesses file GSTR 3 after submitting GSTR 1 (sales details) and GSTR 2 (purchase details). The government checks all this information to make sure the right amount of tax is paid.

Right now, GSTR 3 is not in use, and businesses file GSTR-3B instead. This helps businesses follow the GST rules and avoid penalties.

Why is GSTR-3 important?

GSTR-3 is important because it provides a complete picture of a business’s tax liability for the month. It combines the details of both sales (from GSTR 1) and purchases (from GSTR 2), ensuring that the correct amount of tax is calculated. This helps businesses accurately determine how much tax they need to pay and how much they can claim back as refunds (input tax credit) for their purchases.

Additionally, GSTR-3 allows the government to verify the information provided by businesses, preventing tax fraud and ensuring compliance with GST laws. Filing GSTR-3 correctly also helps businesses avoid penalties and stay in good standing with the tax authorities. Although GSTR-3 is currently suspended, it played a key role in ensuring accurate tax reporting under the GST system.

Who should file GSTR-3?

Any business or taxpayer that is registered under the Goods and Services Tax (GST) in India and has transactions involving the supply of goods or services during a particular month is required to file GSTR-3. This includes:

- Regular Taxpayers: Businesses that are registered under GST and have taxable sales or purchases.

- Casual Taxpayers: Those who occasionally undertake business transactions but do not have a fixed place of business in India.

- Foreign Taxpayers: If a foreign business is making taxable supplies in India, they too are required to file GSTR-3.

- Non-Resident Taxable Persons: Non-residents who make taxable supplies in India.

However, it’s important to note that small businesses that have opted for the composition scheme (which allows them to pay a fixed percentage of turnover instead of normal GST rates) do not have to file GSTR-3. Instead, they file GSTR-4, which is a simplified return.

Details to be provided in GSTR-3

When filing GSTR-3, a business needs to provide detailed information about its sales, purchases, and tax liability for the month. The return is comprehensive and includes various sections that cover different aspects of the business’s financial transactions. Here’s a breakdown of the key details that need to be provided in GSTR-3:

1. Turnover Details:

- Total value of sales (both taxable and non-taxable supplies).

- Exempt, nil-rated, and non-GST supplies.

- Outward supplies (sales) that are taxed at different GST rates (e.g., 5%, 12%, 18%, etc.).

- Exports (if any).

2. Purchases and Inward Supplies:

- The total value of purchases made during the month.

- Input tax credit (ITC) available on purchases (the tax paid on purchases that can be adjusted against your tax liability).

- Purchases from registered suppliers and unregistered suppliers.

- Imports of goods and services, if applicable.

3. Tax Liability:

- The amount of tax you owe on sales (Output Tax).

- Input tax credit (ITC) claimed on purchases.

- Reverse charge details (if applicable). This happens when the buyer pays the tax instead of the supplier.

4. Details of Taxes Paid:

- Taxes paid under CGST (Central GST), SGST (State GST), and IGST (Integrated GST).

- Tax amounts paid through cash or input tax credit.

- Late fees, penalties, and interest paid, if applicable.

5. Interest and Late Fees:

- If there was any delay in filing the return, details of interest or late fees must be provided.

6. Refunds or Additional Tax Liability:

- Any claim for a refund (if applicable), such as for excess tax paid.

- If any additional tax needs to be paid after adjusting the input tax credit.

7. Other Information:

- Any amendments to previous returns (corrections or revisions).

- Details of advance tax paid (if any).

These details in GSTR-3 provide a clear picture of a business’s tax responsibilities, including how much tax it collected, how much it owes, and any adjustments it needs to make for the month.

The format of GSTR-3 is structured to collect all relevant data about a taxpayer’s sales, purchases, tax liabilities, and payments in a detailed manner.

Input tax credit in GSTR 3

The Input Tax Credit (ITC) is a crucial component in the GSTR-3 filing process. It allows businesses to claim the tax paid on purchases (inputs) against the tax liability on their sales (outputs), thereby reducing the amount of tax they need to pay. Here’s a detailed overview of how ITC works in GSTR-3:

1. ITC Reconciliation with GSTR-2

- Claiming ITC: In GSTR-3, businesses claim ITC based on the inward supplies (purchases) reported in GSTR-2. The ITC claim must match the details of the suppliers’ GSTR-1 filings.

- Reconciliation: It is essential to ensure that the ITC claimed matches the invoices uploaded by suppliers. Any mismatch or unreported invoices may lead to the rejection or reduction of the ITC claimed.

2. Conditions to Claim ITC

- Supplier’s Compliance: To claim ITC, suppliers must file their GSTR-1 accurately and on time. If the supplier fails to file GSTR-1 or reports incorrect invoice details, the buyer may not be able to claim the full ITC.

- GSTR-2 Matching: The details of inward supplies must match the supplier’s GSTR-1 for you to claim ITC in GSTR-3.

- Eligibility: The goods or services purchased must be used for business purposes, and the taxpayer must possess a valid tax invoice or debit note to claim ITC.

3. ITC Adjustment in GSTR-3

- Tax Payment Adjustment: After determining the eligible ITC in GSTR-3, businesses can offset their output tax liability (tax on sales) with the ITC from the inward supplies (purchases). This adjustment reduces the net tax payable.

- Liability Offset: The ITC can be used to pay off the tax liability in the following order:

- IGST liability

- CGST and SGST liability

4. ITC Reversal in GSTR-3

- ITC Reversal: In some cases, a reversal of ITC may be required if the input goods or services are used for personal purposes, are not for business use, or if payment to the supplier is not made within 180 days. The reversed ITC is added back to the tax liability in GSTR-3.

- Capital Goods: In cases where capital goods are sold or transferred, the ITC claimed on those goods must be reversed in GSTR-3.

5. Reporting ITC in GSTR-3

- Section for ITC: GSTR-3 includes specific sections where the total ITC available, ITC utilized, and ITC reversed must be reported. The form calculates the final tax liability after considering ITC claims and adjustments.

6. Verification of ITC

- GST Portal Verification: The GST portal performs an automated matching process, where it compares the ITC claimed by the buyer with the invoices uploaded by the supplier. Any discrepancies can lead to the suspension or rejection of the ITC claim.

- ITC Ledger: The ITC ledger in the GST portal tracks the ITC available, utilized, and balance carried forward for each tax period, providing clarity to taxpayers regarding their ITC status.

7. Common ITC-Related Issues

- ITC Mismatch: A mismatch between ITC claimed and the data filed by suppliers can lead to reduced ITC and may trigger compliance notices.

- Delayed Filing by Supplier: If a supplier delays the filing of GSTR-1, the buyer cannot claim ITC for that period, which can affect cash flow.

- Provisional ITC Claims: Businesses may face challenges due to provisional ITC claims, where ITC is claimed based on estimates when the actual supplier data is unavailable.

Input Tax Credit (ITC) is a vital part of the GSTR-3 filing process, as it helps businesses reduce their tax liability. Accurate reconciliation between GSTR-2 and supplier GSTR-1 filings, timely reporting, and compliance with ITC conditions are essential to successfully claim ITC in GSTR-3. Automated tools and regular communication with suppliers can ensure that the ITC claim process is smooth and error-free.

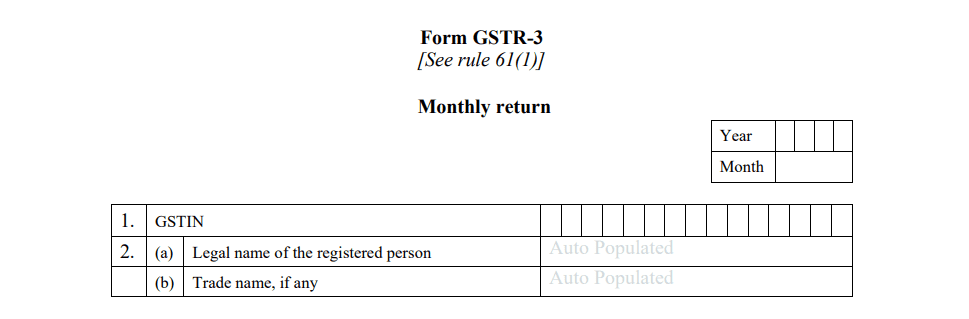

Form of GSTR-3

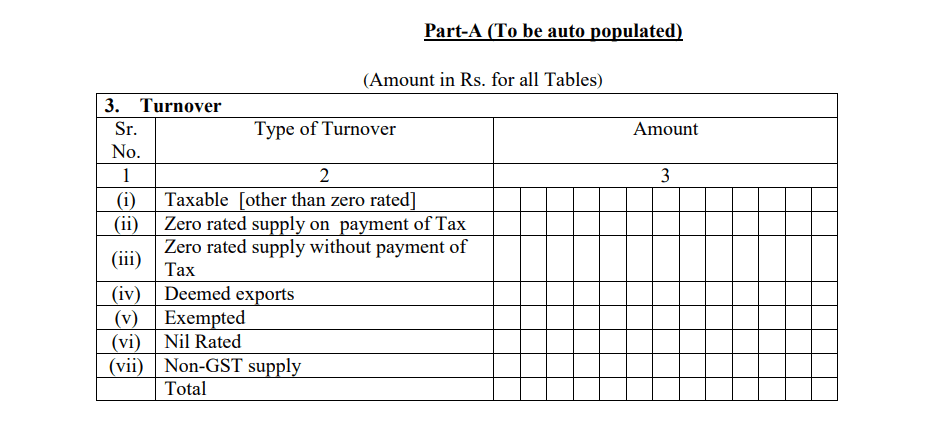

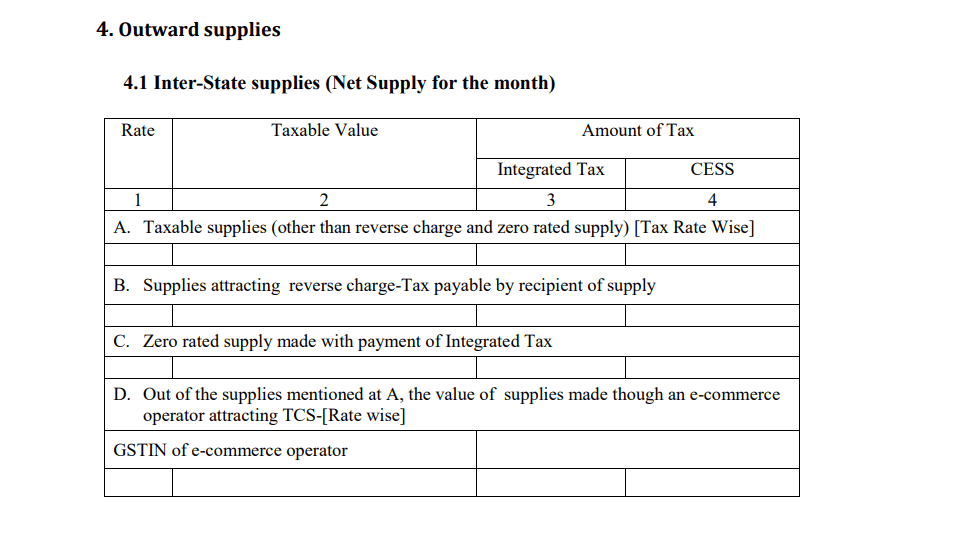

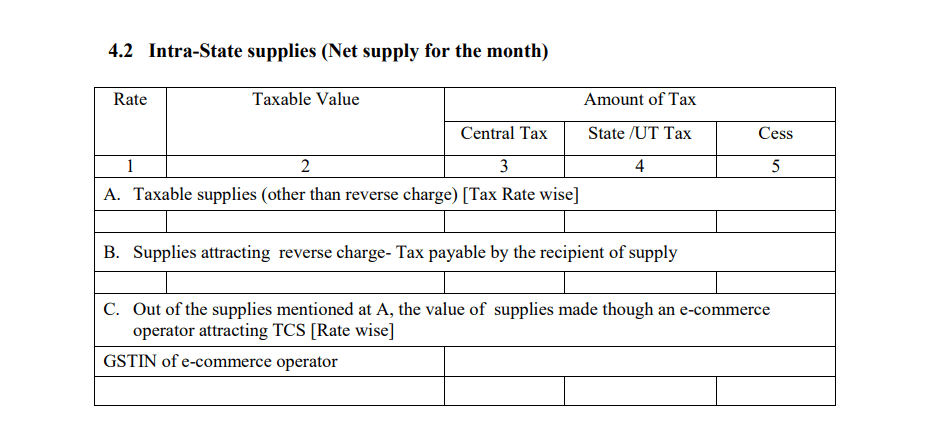

Part A: Auto-Populated Information

This section is auto-generated based on details from GSTR-1, GSTR-1A, and GSTR-2.

1. GSTIN: The Goods and Services Tax Identification Number (GSTIN) or provisional ID of the taxpayer.

2. Name of the Taxpayer: The legal and trade name of the taxpayer (auto-populated).

3. Turnover Details:

- Taxable Turnover: Sales that are subject to GST.

- Zero-Rated Supply with Payment of Tax: Exports with paid IGST.

- Zero-Rated Supply without Payment of Tax: Exports under Bond/LUT.

- Deemed Exports: Sales to Special Economic Zones (SEZ).

- Exempted Supplies: Goods or services exempt from GST.

- Nil-Rated and Non-GST Supplies: Items attracting 0% GST or outside GST scope (e.g., petrol, electricity).

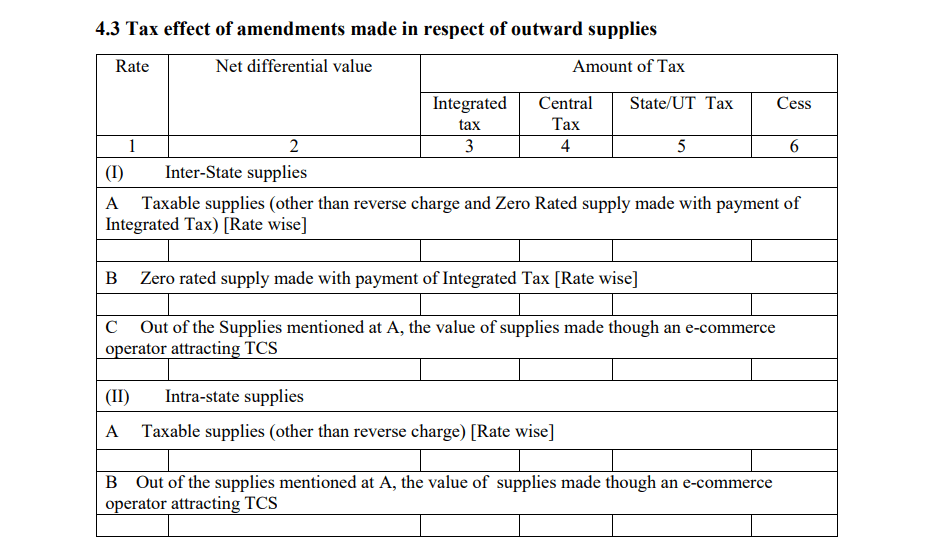

4. Outward Supplies (Sales):

- Inter-State Supplies:

- Taxable sales

- Sales attracting reverse charge

- Zero-rated supplies with IGST

- Sales via e-commerce operators (TCS applicable).

- Intra-State Supplies: Same as above but within the same state.

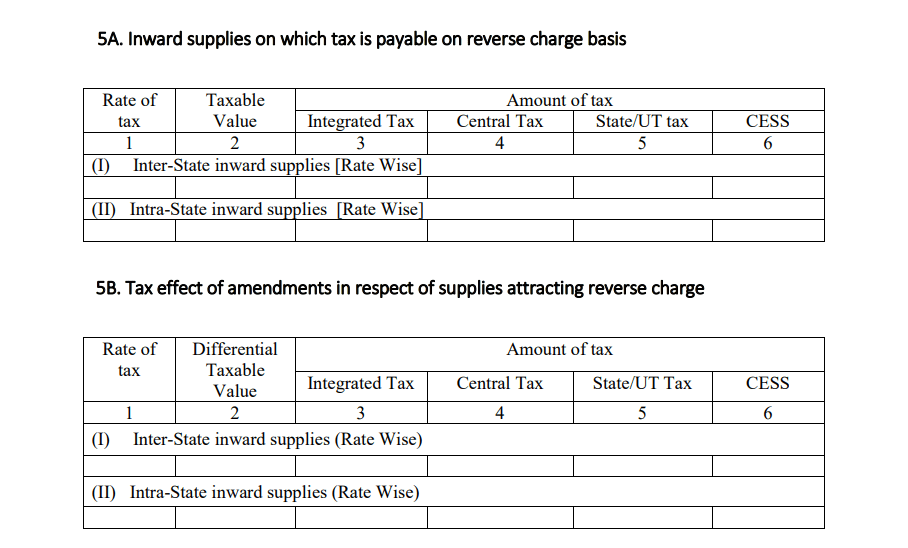

5. Inward Supplies (Purchases):

- Reverse Charge Purchases: Goods/services where the buyer (you) pays the GST.

- Amendments: Changes to previous reverse charge purchases.

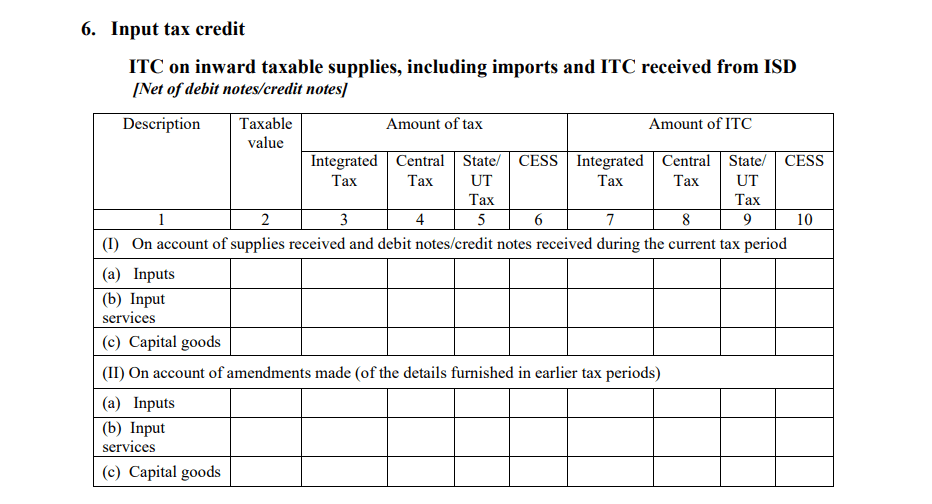

6. Input Tax Credit (ITC):

- ITC Claimed: For inputs, services, and capital goods.

- ITC Adjustments: Changes to ITC from previous months.

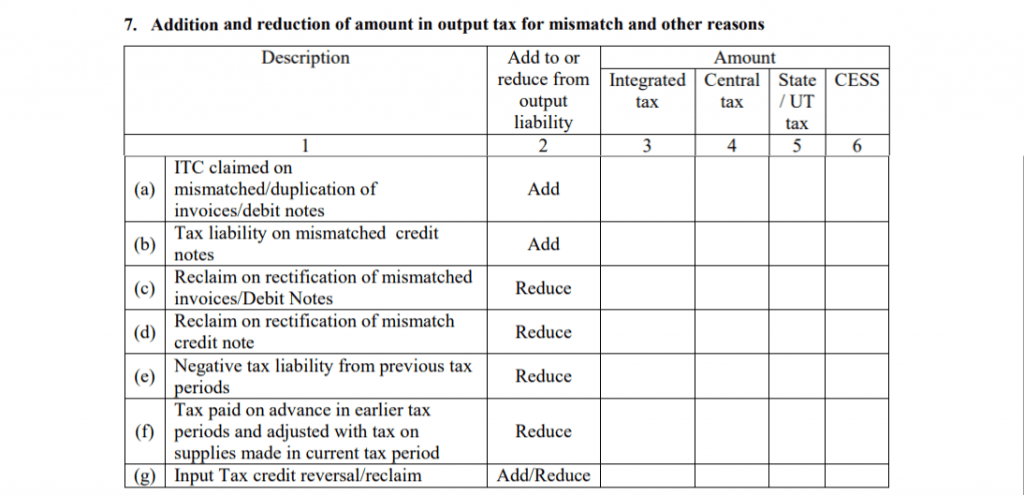

- Mismatch Adjustments:

- Tax due to mismatches in ITC or sales.

- Reversal or reclaim of ITC for mismatch adjustments.

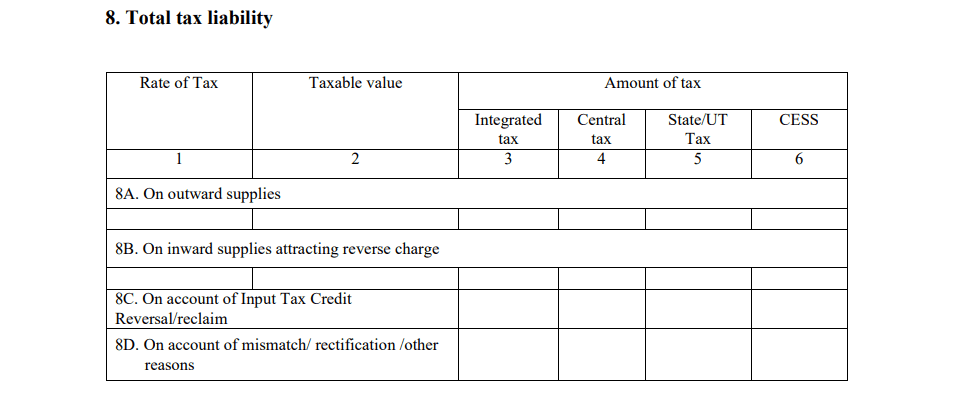

- Total Tax Liability:

- On Outward Supplies: Tax due on sales.

- On Reverse Charge Purchases: Tax due on reverse charge transactions.

- Due to ITC Reversals: Tax changes due to ITC reversal or reclaim.

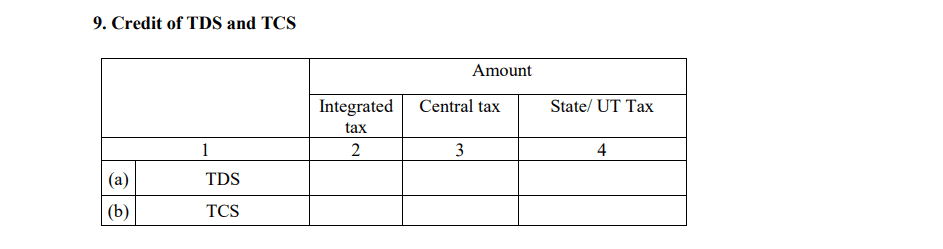

- Credit of TDS/TCS: Deductions for TDS/TCS (tax deducted at source).

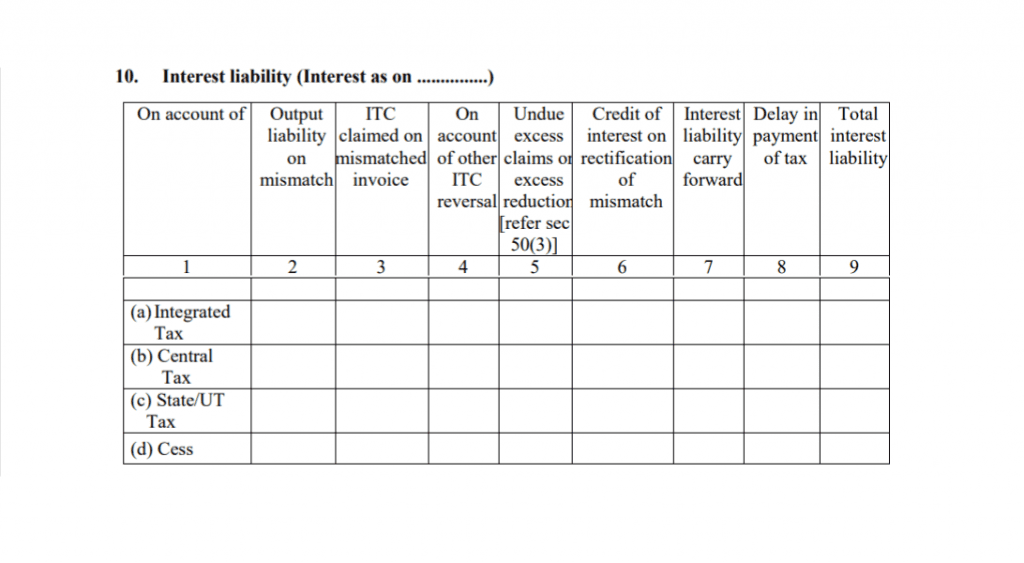

- Interest Liability: Interest on delayed payment of taxes at 18% per annum.

- Late Fee: Rs. 100 per day under CGST and SGST (Rs. 200/day total), with a maximum of Rs. 5,000. No late fee on IGST.

Part B: Taxpayer Input Information

This part is filled manually by the taxpayer.

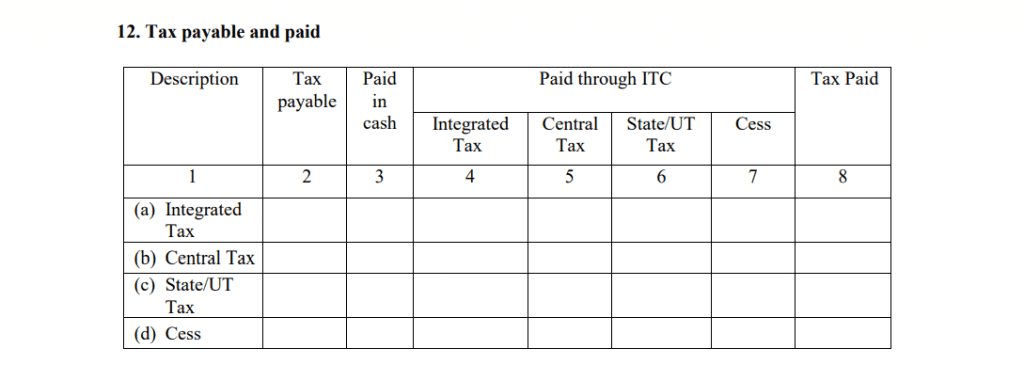

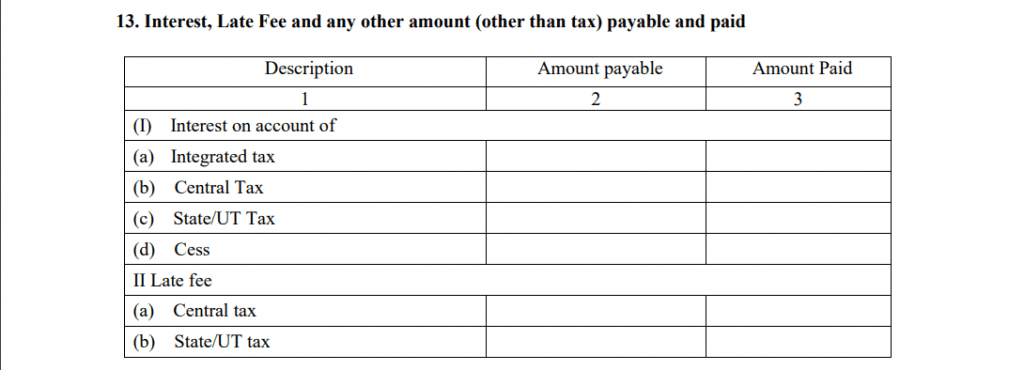

1. Tax Payable and Paid: Breakup of the tax paid through ITC or cash.

2. Interest, Late Fee, and Other Payments: Details of any additional payments due (interest, late fee).

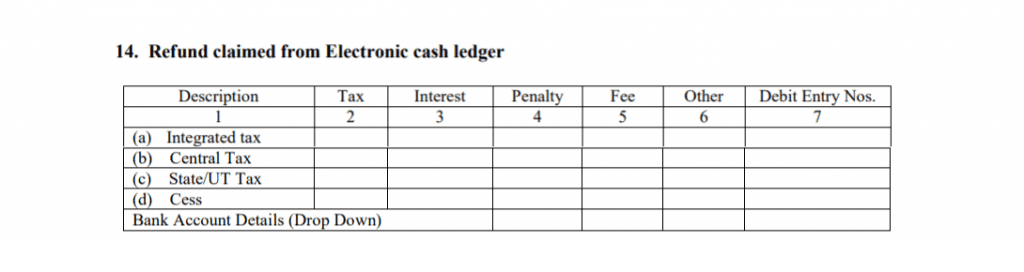

3. Refund Claimed: Refund details from the electronic cash ledger.

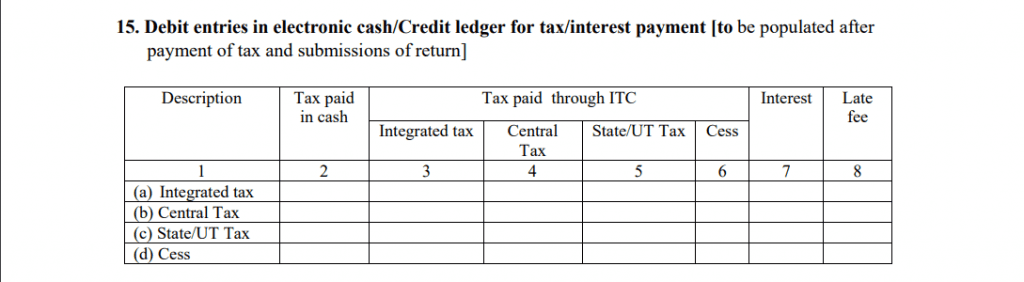

4. Debit Entries in Electronic Cash/Credit Ledger: Auto-populated details after the payment of tax and submission of the return.

Essential Rules for Filing the GSTR 3 Form

Filing GSTR-3 requires adhering to specific rules and guidelines to ensure accurate reporting and avoid penalties. Here are the essential rules for filing the GSTR-3 form:

1. Ensure Prior Filing of GSTR-1 and GSTR-2:

- GSTR-3 is based on the information provided in GSTR-1 (outward supplies) and GSTR-2 (inward supplies). Therefore, GSTR-1 and GSTR-2 must be filed first.

- Data from GSTR-1 and GSTR-2 are auto-populated in GSTR-3.

2. Maintain Correct Books of Accounts:

- Accurate and up-to-date records of all transactions are crucial. These records include sales, purchases, taxes collected, and taxes paid.

- Mismatches in your records can lead to reconciliation issues and potential penalties.

3. Filing Due Date:

- GSTR-3 must be filed by the 20th of the following month. For example, for transactions made in July, GSTR-3 must be filed by the 20th of August.

- Missing this deadline can result in late fees and interest charges.

4. Payment of Taxes Before Filing:

- All tax liabilities (GST on sales) should be paid before filing the GSTR-3 return.

- Taxes can be paid using the input tax credit (ITC) balance or by depositing cash in the electronic cash ledger.

5. Include Details of Advances Received:

- Any advances received for future sales must be reported and tax paid on these advances.

- Even if goods or services haven’t been supplied yet, the tax liability on advances is due.

6. Report Reverse Charge Mechanism (RCM) Transactions:

- If you’ve purchased goods or services subject to reverse charge, you must report the applicable taxes and pay them.

- These taxes can be claimed as input tax credit in future returns, but they must be reported accurately in GSTR-3.

7. Verify and Reconcile Data:

- Before submitting GSTR-3, reconcile the details of sales, purchases, input tax credit, and tax liability to avoid discrepancies.

- Any errors or mismatches between GSTR-1, GSTR-2, and GSTR-3 should be resolved before filing.

8. Late Filing Penalties:

- If you miss the filing deadline, a late fee of ₹50 per day (₹25 for CGST and ₹25 for SGST) will be charged until the return is filed.

- If you have nil tax liability, the late fee is reduced to ₹20 per day (₹10 each for CGST and SGST).

- In addition to the late fee, interest at 18% per annum will be charged on any outstanding tax liability.

9. Revise GSTR-3:

- GSTR-3 cannot be revised once it is filed. Therefore, it’s crucial to double-check all entries before submitting the return.

- If any errors are found after filing, they can only be corrected in the next month’s return.

10. Claiming Input Tax Credit (ITC):

- Input tax credit (ITC) on purchases can only be claimed if the supplier has uploaded their invoices and filed their GSTR-1.

- ITC is crucial in reducing the final tax liability and must be claimed accurately.

11. Electronic Verification:

- Once all the details are filled in, the return must be digitally signed or electronically verified using an OTP or digital signature certificate (DSC).

12. Adjustments for Credit Notes and Debit Notes:

- If any credit or debit notes were issued or received during the month, they should be reported in GSTR-3, and the necessary adjustments should be made to the tax liability.

By following these rules, businesses can ensure that their GSTR-3 filing is accurate, timely, and compliant with GST regulations. Proper filing helps avoid penalties and ensures smooth GST compliance.

What happens if GSTR-3 is not filed?

If GSTR-3 is not filed, the consequences can have both financial and legal implications for a business. Here’s what can happen if GSTR-3 is not filed:

1. Late Fees and Penalties:

- A late fee will be imposed for missing the filing deadline. The late fee is ₹50 per day (₹25 for CGST and ₹25 for SGST), with a cap of ₹5,000.

- If you have nil tax liability, the late fee is reduced to ₹20 per day (₹10 for CGST and ₹10 for SGST).

2. Interest on Outstanding Tax Liability:

- If there is any outstanding tax liability that was not paid because GSTR-3 wasn’t filed, an interest of 18% per annum will be charged on the unpaid amount. The interest is calculated from the due date of filing GSTR-3 until the actual payment is made.

3. Inability to File Subsequent Returns:

- GSTR-3 is part of a monthly filing process, and if it is not filed for a particular month, it prevents the business from filing subsequent GST returns like GSTR-1 and GSTR-3B. This creates a backlog, making it harder for the business to comply with GST regulations.

4. Loss of Input Tax Credit (ITC):

- Failing to file GSTR-3 means that input tax credit (ITC) on purchases may not be fully available. This can increase the business’s tax liability since they can’t claim the tax already paid on purchases to reduce the tax payable on sales.

5. Legal Consequences and Notice from GST Authorities:

- If the return is continuously not filed, the taxpayer may receive a show cause notice from the GST department. If the return is still not filed after receiving the notice, further action could be taken, including penalties or cancellation of the GST registration.

6. Impact on Compliance Rating:

- The GST system maintains a compliance rating for all registered taxpayers. If GSTR-3 is not filed on time, it could negatively affect the business’s compliance score, which may influence future transactions and assessments by the authorities.

7. Potential Business Disruptions:

- Non-filing of GSTR-3 can disrupt business operations, especially when it comes to making GST payments, claiming refunds, or conducting business with clients who may prefer working with compliant businesses.

8. Blocking of E-Way Bills:

- If GSTR-3 is not filed for a specific period, the business may not be able to generate e-way bills, which are required for transporting goods. This could result in delays in deliveries and affect the business’s ability to operate smoothly.

What is required to file GSTR-3?

Before filing GSTR-3, there are several important steps and prerequisites that a business must complete to ensure the process goes smoothly and accurately. Here’s what needs to be done first:

1. Ensure Filing of GSTR-1 and GSTR-2:

- GSTR-3 is auto-populated based on the information provided in GSTR-1 (outward supplies) and GSTR-2 (inward supplies).

- Businesses must file GSTR-1 (sales) and GSTR-2 (purchases) for the relevant tax period before proceeding with GSTR-3.

2. Reconcile Sales and Purchase Data:

- Cross-check your sales and purchase records with the data in GSTR-1 and GSTR-2 to ensure there are no discrepancies.

- Make sure that all invoices for both sales and purchases have been accurately recorded.

3. Confirm Input Tax Credit (ITC) Eligibility:

- Review and verify your input tax credit (ITC) details before filing. ITC is the tax paid on purchases that can be claimed to reduce your tax liability.

- Ensure that the input tax credit claimed matches the details provided by your suppliers in GSTR-1.

4. Calculate Tax Liability:

- Accurately calculate your total tax liability, including GST on sales (output tax), GST paid on purchases (input tax credit), and any tax payable under the reverse charge mechanism.

- Include any adjustments required for advance payments or previous tax periods.

5. Ensure Payment of Tax Liability:

- Any outstanding tax liability (the difference between output tax and ITC) must be paid before filing GSTR-3.

- Taxes can be paid using the electronic cash ledger or electronic credit ledger. Make sure there is enough balance in the ledger to cover the liability.

6. Prepare and Gather Relevant Documents:

- Ensure that you have all necessary documents and records, including sales invoices, purchase invoices, credit notes, debit notes, and records of tax paid.

- Proper documentation will help reconcile data and avoid discrepancies during filing.

7. Review Reverse Charge Mechanism (RCM) Details:

- If your business is subject to the reverse charge mechanism, ensure that the appropriate taxes have been calculated and are ready to be reported in GSTR-3.

8. Check for Amendments or Corrections:

- If there are any errors or discrepancies in previously filed returns (GSTR-1 or GSTR-2), these should be amended before filing GSTR-3.

- Make sure that any corrections needed from earlier returns are addressed in GSTR-3.

9. Complete Digital Signature or E-Verification Setup:

- Ensure that the Digital Signature Certificate (DSC) or Electronic Verification Code (EVC) is set up, as you will need to use one of these to authenticate and submit the return.

10. Ensure Timely Filing:

- GSTR-3 should be filed by the 20th of the following month. Missing this deadline will result in late fees, interest, and potentially legal notices from GST authorities.

How to file GSTR 3?

Filing GSTR-3 involves several steps and can be done online through the GST portal. Even though GSTR-3 has been replaced by GSTR-3B for now, here’s a step-by-step guide for how to file GSTR-3, should it be reintroduced in the future:

Step-by-Step Process to File GSTR-3:

Step 1: Log In to the GST Portal

- Go to the GST Portal.

- Use your GSTIN (GST Identification Number) and password to log in to your account.

- Once logged in, select the ‘Returns Dashboard’ from the menu.

- Select the financial year and the return filing period (month) for which you want to file GSTR-3.

- Under the returns section, you’ll find the option for ‘GSTR-3’. Click on it.

Step 3: Verify Auto-Populated Data

- Part A of GSTR-3 is auto-populated using the data from your previously filed GSTR-1 (sales) and GSTR-2 (purchases).

- Review the auto-filled details, including your sales, purchases, and tax liabilities.

Step 4: Enter Additional Details in Part B

- In Part B, manually enter any missing details such as:

- Payment of taxes: Include the taxes you owe, calculated after adjusting the input tax credit.

- Advance payments: Report any advances received for goods or services yet to be supplied.

- Reverse charge liabilities: Include taxes on goods/services where you are liable to pay tax under the reverse charge mechanism.

- Interest and late fees: If applicable, enter any interest or late fees for delayed filing or payment.

Step 5: Claim Input Tax Credit (ITC)

- Verify the input tax credit claimed on purchases, including imports and reverse charge transactions.

- Ensure the ITC matches the data from GSTR-2 and the information provided by your suppliers.

Step 6: Pay Any Tax Liability

- Tax liability (if any) must be paid before submitting the return. You can pay the tax using:

- Electronic Cash Ledger: Deposit cash into this ledger and use it to pay the outstanding tax.

- Electronic Credit Ledger: Utilize the input tax credit available in this ledger to offset your tax liability.

- Ensure you have enough balance in your cash or credit ledger to pay the required tax.

Step 7: Verify and Submit GSTR-3

- Review all the details entered carefully, including the auto-populated data and the manually entered information in Part B.

- After verifying everything, click on the ‘Submit’ button to freeze the data entered.

Step 8: File the Return with DSC or EVC

- After submission, file the return using one of these two methods:

- Digital Signature Certificate (DSC): If you are a company or LLP, you must use a DSC to verify and submit the return.

- Electronic Verification Code (EVC): For other taxpayers, an EVC sent to your registered mobile number or email can be used to file the return.

Step 9: Generate Acknowledgment (ARN)

- Once the return is filed successfully, an Acknowledgment Reference Number (ARN) is generated. Keep this ARN as proof of filing.

- You can download the filed GSTR-3 return and keep a copy for your records.

Step 10: Reconcile and File Subsequent Returns

- After filing GSTR-3, make sure to reconcile the data with your books of accounts and ensure there are no discrepancies.

- Filing GSTR-3 on time allows you to file subsequent returns like GSTR-1 and GSTR-3B without issues.

Common Challenges and Issues in GSTR 3 Return Filing

1. Mismatch of Input Tax Credit (ITC)

- One of the major challenges in GSTR-3 filing is reconciling the input tax credit (ITC) claimed in GSTR-2 with the invoices uploaded by suppliers in GSTR-1. Any mismatch can lead to discrepancies and cause delays in filing.

2. Inaccurate Details in GSTR-1 and GSTR-2

- Errors or omissions in GSTR-1 (outward supply) or GSTR-2 (inward supply) can complicate GSTR-3 filing. Since GSTR-3 is based on these forms, inaccuracies require corrections before proceeding.

3. Late Filing Penalties

- Missing the deadline for filing GSTR-3 can result in late fees and penalties. Businesses often struggle to meet filing deadlines due to the complexity of reconciling data from different forms.

4. Complex Reconciliation Process

- Reconciling GSTR-1, GSTR-2, and GSTR-3B can be a difficult task, especially for businesses with high volumes of transactions. Ensuring accuracy across these forms is critical to avoid non-compliance.

5. Technical Glitches on the GST Portal

- Frequent technical issues on the GST portal, such as slow processing or system crashes during peak filing periods, can disrupt the filing process and lead to delays.

6. Frequent Changes in Compliance Rules

- The GST regime is subject to regular updates, which can make it challenging for businesses to stay compliant. Understanding new rules and updates is crucial for accurate GSTR-3 filing.

7. Lack of Automated Tools

- Many businesses still rely on manual processes for filing GSTR-3, increasing the risk of human errors. Lack of automated accounting tools can make it difficult to handle large datasets efficiently.

8. Difficulty in Revising Returns

- If a mistake is made in GSTR-3, revising the return is not an easy process. Once filed, corrections can be time-consuming, often leading to delays and potential penalties.

9. Cash Flow Management for Tax Payment

- GSTR-3 filing involves the payment of tax liability. Businesses with cash flow issues may face difficulties in meeting their tax liabilities on time, leading to interest charges.

10. Vendor Compliance Issues

- In some cases, vendors may not file their GSTR-1 forms on time, affecting the ITC reconciliation process for the buyer. This creates delays and affects the filing of GSTR-3.

Tips and Best Practices for GSTR 3 Return Filing

1. Reconcile GSTR-1 and GSTR-2 in Advance

- Before filing GSTR-3, ensure your GSTR-1 (outward supplies) and GSTR-2 (inward supplies) are reconciled correctly. Any mismatches should be addressed to avoid discrepancies in GSTR-3.

2. Ensure Timely Filing

- Filing GSTR-3 on time avoids late fees and penalties. Create reminders for upcoming due dates, and avoid last-minute filings, especially during high-traffic periods on the GST portal.

3. Use Accounting Software for Automation

- Leverage GST-compliant accounting software to automate invoice generation, tax calculations, and filing processes. Automation minimizes human error and simplifies data handling.

4. Stay Updated with GST Rules

- GST regulations change frequently, so it’s essential to stay updated on the latest amendments and circulars. Subscribing to GST newsletters or consulting with a tax professional can help you stay compliant.

5. Maintain Detailed Records

- Ensure all tax invoices, credit notes, and debit notes are maintained accurately. Record-keeping is crucial for reconciling data and complying with audits.

6. Perform Regular ITC Reconciliation

- Perform regular reconciliation of Input Tax Credit (ITC) with GSTR-2 to avoid discrepancies during GSTR-3 filing. Cross-check ITC claims with vendor invoices and their GSTR-1 filings to ensure alignment.

7. Address Vendor Non-Compliance

- Proactively communicate with vendors to ensure they file GSTR-1 on time and provide correct invoice details. This will prevent ITC mismatches in your GSTR-3 filing.

8. Review and Verify Data Before Submission

- Double-check all figures, invoices, and tax calculations before finalizing GSTR-3. Errors can lead to penalties or additional scrutiny during audits.

9. Use the Offline Utility Tool

- The GST portal provides an offline utility tool to prepare and upload GSTR-3. This can be useful if you experience issues with the online portal, especially during peak times.

10. Seek Professional Help When Necessary

- For businesses with complex transactions or large volumes of data, seeking professional assistance from a GST consultant can help avoid errors and ensure compliance with regulations.

11. Plan for Tax Payments

- Ensure you have enough cash flow or credit to meet your tax liability on time. Set aside funds for tax payments well in advance to avoid penalties or interest charges for delayed payments.

12. Address Errors in Previous Returns

- If you identify errors in earlier returns (GSTR-1 or GSTR-2), correct them in the current filing. Though GSTR-3 cannot be revised, adjustments can be made to rectify past errors.

13. Monitor GST Portal for Technical Updates

- Stay informed about scheduled maintenance or downtimes on the GST portal. Filing returns during off-peak hours can help avoid delays caused by portal traffic.

14. Cross-Check Payments and Liabilities

- Verify that the tax paid matches the liability in your GSTR-3 form. Any mismatches between tax payable and tax paid can lead to notices from the tax authorities.

How to Revise GSTR-3

Unfortunately, GSTR-3 cannot be revised once it is filed. Unlike some other tax forms, the GST portal does not allow modifications to GSTR-3 after submission. This makes it crucial to ensure that all the details are accurate before filing the return. However, there are a few ways to address errors made in GSTR-3:

1. Correcting Errors in Subsequent Returns

- If you discover an error in GSTR-3 after filing, you can make adjustments in subsequent returns, such as GSTR-3B for the following tax period. Any discrepancies in tax payments, ITC claims, or outward supplies can be adjusted in future returns.

2. Amending GSTR-1 or GSTR-2

- Since GSTR-3 is based on the information provided in GSTR-1 (Outward Supply) and GSTR-2 (Inward Supply), errors in GSTR-3 can sometimes be corrected by amending GSTR-1 or GSTR-2 forms. These forms can be revised, and any corrections will reflect in the subsequent GSTR-3 filing.

3. Use of GSTR-9 (Annual Return)

- Businesses can correct any errors made in GSTR-3 when they file the GSTR-9 (Annual Return). GSTR-9 provides an opportunity to reconcile all the supplies, ITC claims, and payments made throughout the financial year. Mistakes or omissions in GSTR-3 can be rectified during this process.

4. Claiming Missing ITC in Subsequent Periods

- If there was an error in claiming Input Tax Credit (ITC) in the current GSTR-3 filing, it can be adjusted in the subsequent tax period. You can claim the missing ITC in the future GSTR-3B filings as long as it falls within the allowed timeframe.

5. Adjustments via GSTR-3B

- GSTR-3B, the simplified summary return, allows for adjustments in the subsequent tax period. If you made an under-reporting or over-reporting error in GSTR-3, you can adjust the figures in GSTR-3B of the next month to rectify your tax liability or ITC.

6. Contacting GST Authorities

- In case of significant errors that may affect compliance, it may be helpful to consult a GST professional or approach the GST authorities. They may guide you on how to manage such errors or provide recommendations for corrective action.

Key Takeaways:

- GSTR-3 Overview: A crucial monthly GST return form capturing total tax liability by combining sales and purchase data.

- Current Status: Replaced by GSTR-3B, but still important for accurate tax calculations and compliance.

- Key Details: Covers turnover, purchases, input tax credit, and tax liabilities. Requires prior submission of GSTR-1 and GSTR-2.

- Reconciliation: Helps in reconciling input tax credit and ensuring correct tax payments and eligible refunds.

- Importance: Filing GSTR-3 correctly prevents late fees, legal consequences, and maintains a clean tax record.

- Error Correction: Cannot be revised, but errors can be corrected in future filings.

- Best Practices: Stay compliant with GST rules and use automation tools for accurate reporting and smooth filing.

FAQs

- What is the impact of GSTR-3 on ITC?

GSTR-3 helps businesses claim input tax credit (ITC) based on purchases reported in GSTR-2, which reduces their tax liability on sales.

- What is the auto-population feature in GSTR-3?

GSTR-3 auto-populates data from GSTR-1 (sales) and GSTR-2 (purchases), ensuring accuracy in tax calculations.

- Is GSTR 3 filed monthly or quarterly?

GSTR-3 is filed monthly.

- What is the turnover limit of GSTR 3?

All registered businesses under GST, regardless of turnover, are required to file GSTR-3.

- Am I required to file a return if there are no transactions?

Yes, a nil GSTR-3 must still be filed even if there are no transactions.

- When is an NRI required to file GSTR-3?

Non-resident taxable persons must file GSTR-3 if they have conducted taxable supplies in India.

- How to know if the GSTR-3 filed is a valid return?

A valid GSTR-3 return is acknowledged with an Acknowledgment Reference Number (ARN) after successful submission.

- The Primary Purposes of GSTR 1 and GSTR 2 in GSTR 3 Filing?

GSTR-1 provides details of sales, and GSTR-2 provides details of purchases, which together help in calculating the correct tax liability in GSTR-3.

- What constitutes GSTR-3?

GSTR-3 includes details of sales, purchases, tax liabilities, input tax credit claims, and tax payments.

- Is there any taxpayer who is not required to file GSTR-3?

Taxpayers under the composition scheme and small businesses with no taxable transactions are not required to file GSTR-3.

- What is the mode of filing GSTR-3 with the authorities?

GSTR-3 is filed online through the GST portal.

- Can the date of filing GSTR 3 be extended?

Yes, the government may extend the filing due date in special circumstances.

- Can I file my GSTR 3 for a tax period if I have not filed GSTR 3 for a previous tax period?

No, GSTR-3 for the current period cannot be filed until the previous periods are cleared.

- When will a return filed by me be considered invalid?

A return is invalid if not signed digitally or if mandatory details are missing.

- How is the self-verification of the return done?

GSTR-3 is self-verified using a Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

- What happens if I don’t pay the full tax liability as calculated by the system?

If full tax is not paid, interest and penalties will be imposed.

- What are TDS and TCS credits and how are they used to set-off the tax liability?

TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) credits can be applied to reduce tax liability while filing GSTR-3.

- How is the tax credit set-off against the tax liability calculated in GSTR 3?

Tax credits (input tax credit) are deducted from the total tax payable to arrive at the final liability in GSTR-3.

- What should be included in the GSTR-3 compliance checklist?

Ensure GSTR-1 and GSTR-2 are filed, calculate tax liability, reconcile invoices, and claim ITC before filing GSTR-3.

- What if I face technical difficulties while filing GSTR 3 online?

You can report the issue to the GST helpdesk and request an extension or resolution.

- Can I claim an input tax credit (ITC) for goods or services that are not directly related to my business?

No, ITC can only be claimed for business-related goods and services.

- What happens if there is a mismatch between my GSTR 3 and my suppliers’ GSTR 1?

A mismatch can lead to discrepancies in input tax credit claims, and corrections may need to be made in subsequent returns.

- What is the format for filing GSTR-3?

GSTR-3 is filed in a structured format with sections for sales, purchases, tax liabilities, and ITC claims.

- Is it mandatory to file GSTR-3 online?

Yes, GSTR-3 must be filed online through the GST portal.

- How to confirm the return is filed?

After filing, a confirmation message with an Acknowledgment Reference Number (ARN) is generated.

- Can I file GSTR-3 without filing GSTR-1 and GSTR-2?

No, GSTR-1 and GSTR-2 must be filed first as they auto-populate the data for GSTR-3.

- Who Should and Should Not File GSTR 3?

Regular and non-resident taxable persons should file GSTR-3, while composition scheme taxpayers do not file GSTR-3.

- How to file GSTR 3 online?

Log in to the GST portal, select GSTR-3 under the returns dashboard, review auto-populated data, enter additional details, and submit with DSC or EVC.

Related Posts:

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS