Understanding how tax systems work, especially for non-resident businesses, is crucial in today’s global economy. The Indian Goods and Services Tax (GST) regime has specific requirements for individuals and businesses that conduct activities in the country but don’t have a permanent establishment here.

One of these requirements is the filing of GSTR-5, a return that must be submitted by non-resident taxable persons (NRTPs). This form plays a vital role in ensuring that these entities fulfill their tax obligations in India, even if their presence in the country is temporary.

In this blog, we will walk you through everything you need to know about GSTR-5, from the basics of who needs to file it to the details it must include, how to file it, and the consequences of missing the deadline.

Brief Overview of GSTR-5

GSTR-5 is a specialized GST return form designed for non-resident taxable persons (NRTPs) conducting business in India. These individuals or businesses don’t have a permanent place of business in India, but they still need to report their transactions under Indian tax law.

Importance of GSTR-5 in the GST System

GSTR-5 helps the government track and collect taxes from businesses or individuals who come into India to engage in commerce on a temporary basis. Filing this return ensures that non-resident businesses fulfill their tax obligations, maintaining transparency and compliance within the Indian GST system. For businesses, it ensures that they avoid penalties and stay in good legal standing while operating in India.

This return is critical because it captures key details such as:

- Sales and purchases (outward and inward supplies) during the reporting period.

- Import of goods and capital from overseas.

- Tax liability and payments made.

- Adjustments or amendments to previously filed returns, if any.

By filing GSTR-5, non-resident taxable persons confirm that all their business activities conducted in India during a specific period have been reported correctly.

Who Needs to File GSTR-5?

The GSTR-5 return is mandatory for non-resident taxable persons (NRTPs) conducting business in India. These individuals or businesses are foreign entities that engage in business transactions within India but do not have a fixed place of business or residence in the country.

Who is a Non-Resident Taxable Person?

A non-resident taxable person is someone who:

Does not have a permanent establishment or fixed place of business in India.

Temporarily engages in taxable transactions within India, such as supplying goods, services, or both.

For example, a company based in the US that temporarily sets up a stall at a trade fair in India to sell its products would be classified as a non-resident taxable person under Indian GST laws.

Eligibility Criteria

To qualify as a non-resident taxable person (NRTP) and file GSTR-5, the following conditions apply:

- Temporary Business Operations in India: The individual or business must not be a permanent resident or have a fixed business establishment in India. They come to India to conduct short-term business, such as setting up a temporary booth at an exhibition.

- GST Registration Requirement: Before conducting any business, the NRTP must obtain a temporary GST registration, which is valid for the period they intend to operate in India. This registration is essential to file GSTR-5.

GSTR-5 Filing Due Date

Timely filing of GSTR-5 is critical for non-resident taxable persons (NRTPs) to remain compliant with the GST (Goods and Services Tax) regulations in India. Failing to file on time can result in penalties and other legal consequences.

Regular Filing Deadline

The due date for filing GSTR-5 is the 20th day of the following month. For instance, if you conducted business activities in India during the month of July, you must file your GSTR-5 return by August 20th. This monthly return captures the details of all taxable transactions made in India during the previous month.

This deadline applies to all NRTPs and is a key date to remember in order to avoid late fees and interest.

Special Cases: Filing After Registration Expiry

In certain cases, a non-resident taxable person may need to file GSTR-5 after their GST registration expires. This typically happens when the NRTP’s temporary registration period comes to an end. In such situations, the NRTP must file their final GSTR-5 return within 7 days of the registration expiry.

For example, if an NRTP’s GST registration ends on March 15th, they must file their final GSTR-5 by March 22nd. This final return is crucial to close out any pending transactions and declare all liabilities.

Examples of Filing Deadlines

To clarify, here are a few examples:

- Business conducted in January: The return must be filed by February 20th.

- Business conducted in March: The return must be filed by April 20th.

- GST registration expires on July 10th: The final GSTR-5 return must be filed by July 17th.

Missing these deadlines can lead to penalties and disrupt business operations.

What Details are Required in GSTR-5?

Filing GSTR-5 involves providing detailed information about a non-resident taxable person’s business transactions within India. This section will break down the key details and fields that must be completed when filing the return. Each section is vital to ensure that all transactions and tax liabilities are accurately reported.

Breakdown of Information Sections

Below are the sections required in GSTR-5, along with a brief explanation of what information needs to be filled:

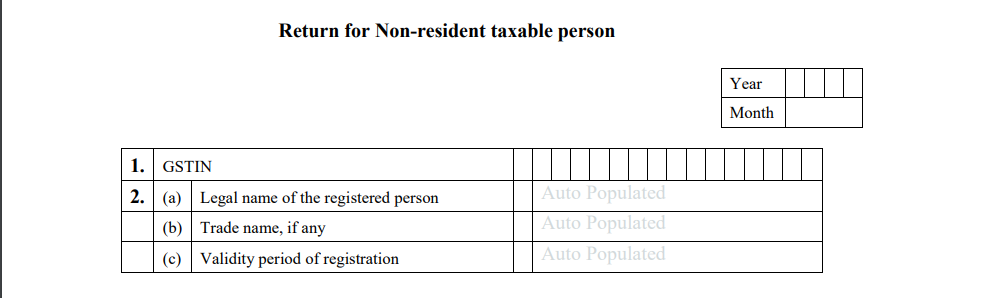

1.GSTIN: The Goods and Services Tax Identification Number assigned to the non-resident taxpayer. It is a unique 15-digit identifier that must be provided on all returns and tax documents.

2. Name of the Taxpayer, Trade Name (if any), and Period: The full legal name of the non-resident taxpayer, as per the GST registration, along with the trade name (if applicable). Additionally, the return period specifies the month and year for which Form GSTR-5 is being filed.

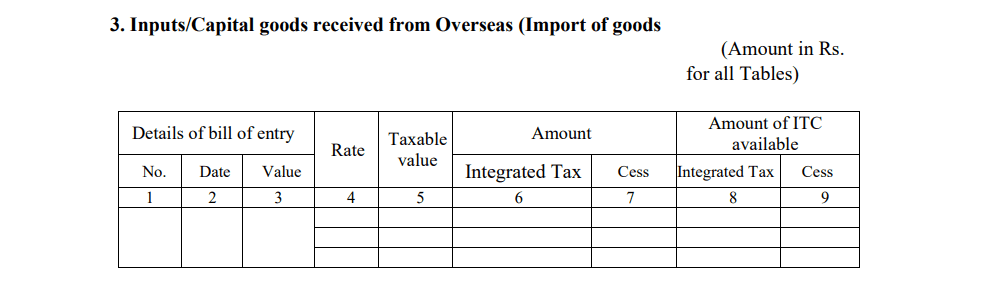

3. Input Capital Goods Received from Overseas (Import of Goods): This section requires details of capital goods imported from outside India. Information like the value of goods, applicable customs duties, and taxes paid on the import needs to be included.

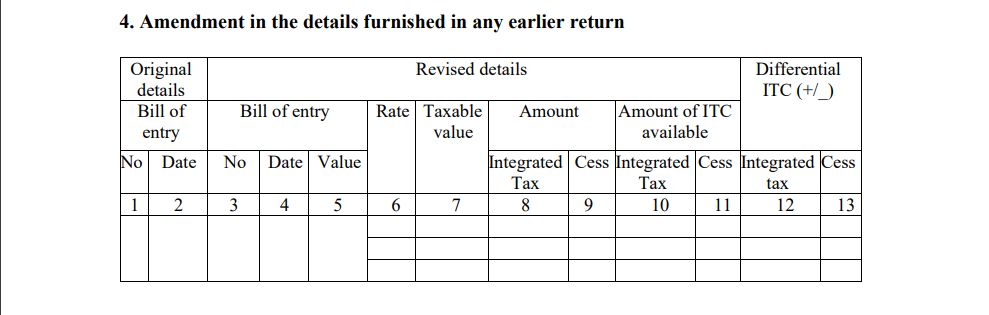

4. Amendment in the Details Furnished in Any Earlier Return: This section allows taxpayers to make corrections or modifications to the details that were submitted in previous GSTR-5 returns. Any amendments in values, tax rates, or errors need to be reflected here.

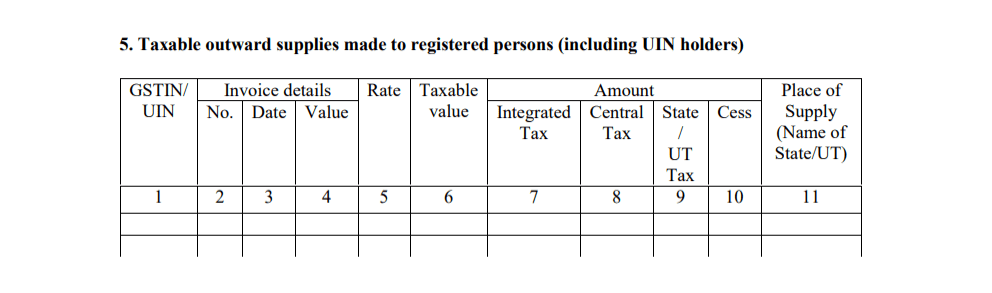

5. Taxable Outward Supplies Made to Registered Persons (Including UIN Numbers): This includes details of all taxable supplies (goods and services) provided to registered taxpayers in India, along with their GSTIN or Unique Identification Number (UIN), if applicable.

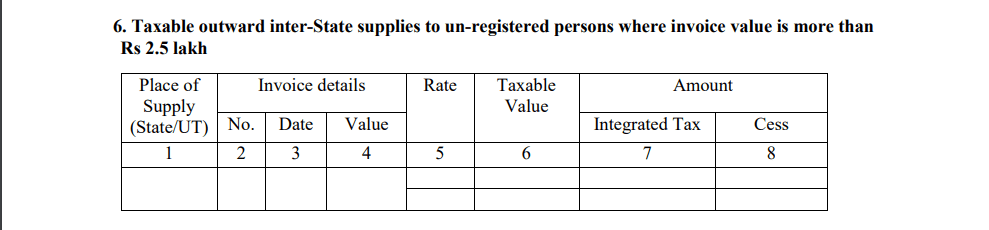

6. Taxable Outward Inter-State Supplies to Unregistered Persons Where Invoice Value is More Than ₹2 Lakh: Any inter-state sales made to unregistered persons where the invoice value exceeds ₹2 lakh should be reported in this section.

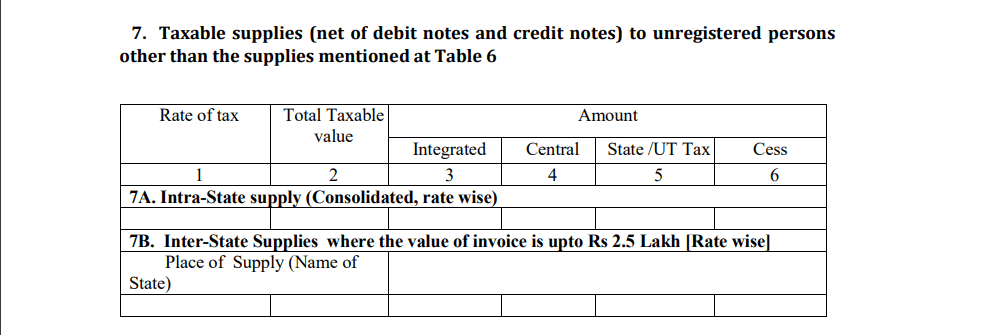

7. Taxable Supplies (Net of Debit Notes and Credit Notes) to Unregistered Persons Other than the Supplies Mentioned at Table 6: This section includes details of taxable supplies to unregistered persons, excluding the ones already mentioned in Table 6. The values should be net of any debit notes or credit notes issued.

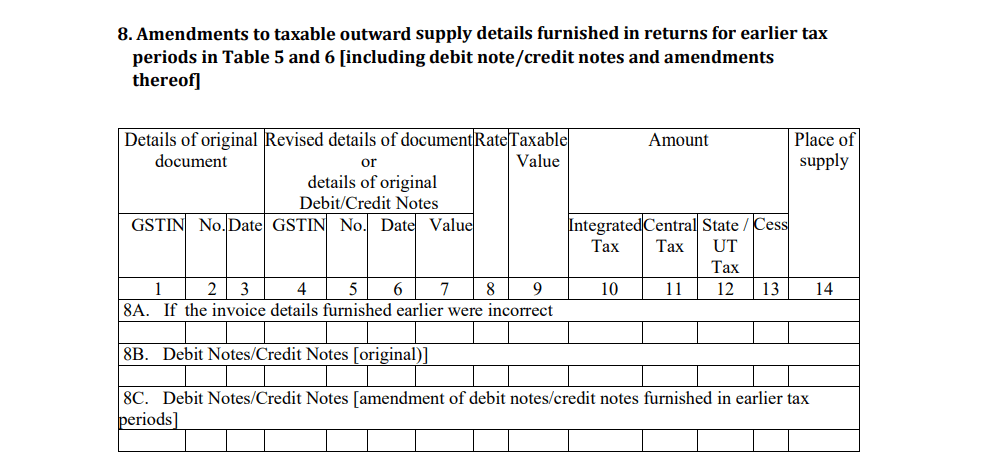

8. Amendments to Taxable Outward Supply Details Furnished in Returns for Earlier Tax Periods in Table 5 and 6 (Including Debit Note/Credit Notes and Amendments Thereof): This section is for any amendments related to the taxable outward supplies made to registered persons (Table 5) or unregistered persons with a high invoice value (Table 6) that were reported in previous periods. It also includes changes due to debit notes, credit notes, or other amendments.

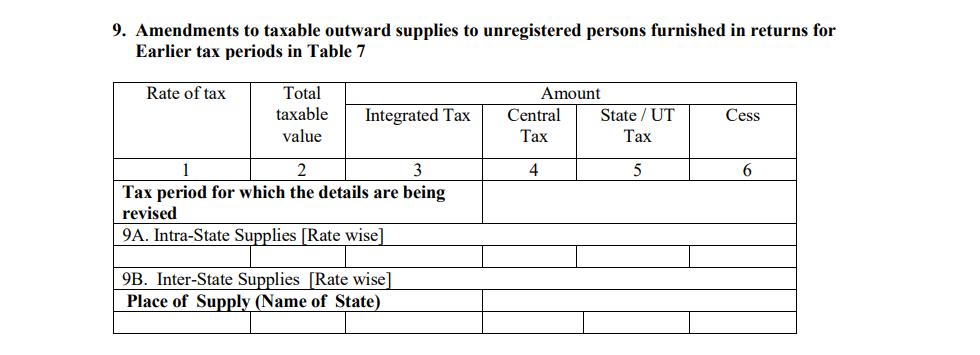

9. Amendments to Taxable Outward Supplies to Unregistered Persons Furnished in Returns for Earlier Tax Periods in Table 7: Any changes or amendments to the taxable supplies made to unregistered persons, reported in Table 7 of earlier returns, are recorded here. This could include corrections in invoice values or tax amounts.

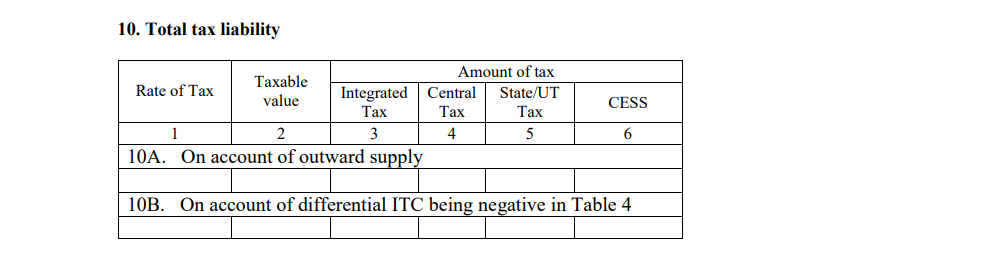

10. Total Tax Liability: The total amount of tax liability for the current return period, calculated based on taxable supplies, input credits, and any amendments. This includes CGST, SGST/UTGST, IGST, and cess, if applicable.

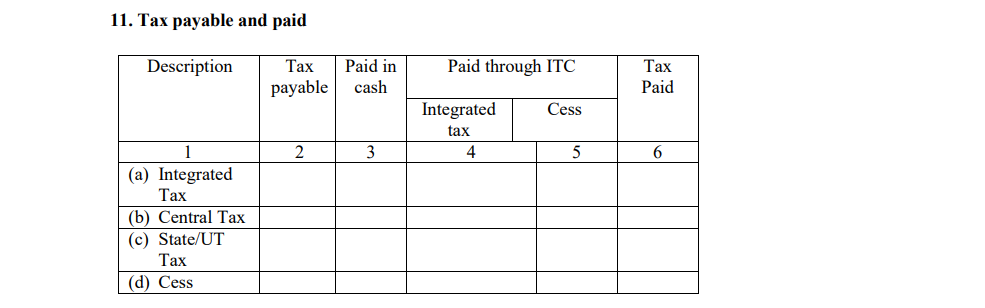

11. Tax Payable and Paid: The amount of tax that is due for payment, along with the amount that has been paid for the period. This section ensures that the taxpayer reports all dues and corresponding payments.

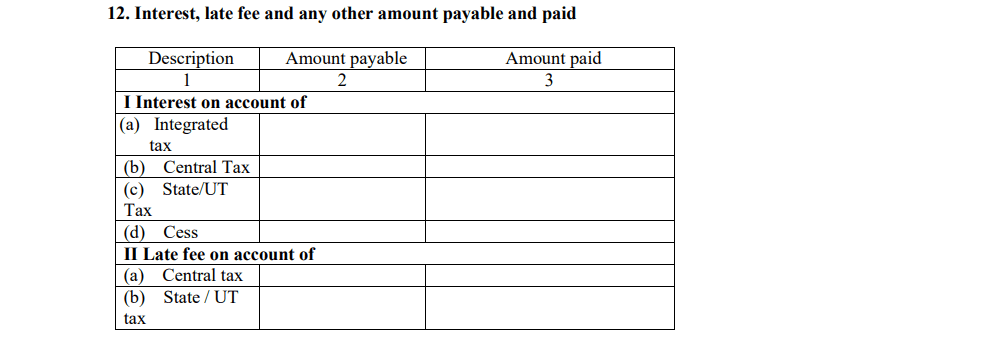

12. Interest, Late Fee, and Any Other Amount Payable and Paid: If there are delays in filing returns or tax payments, the interest and late fees must be recorded here. This section also includes other amounts due, if any, and the payments made against those.

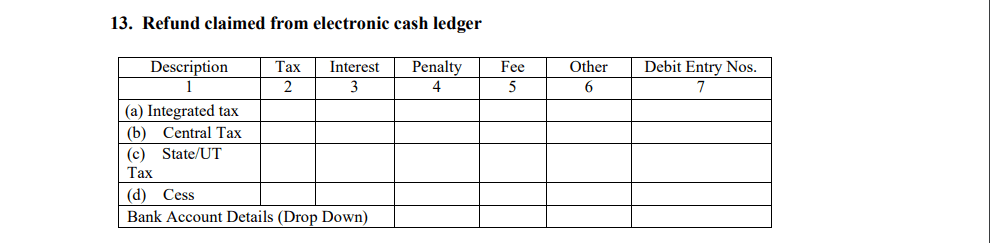

13. Refund Claimed from Electronic Cash Ledger: If the taxpayer has excess cash balance in their electronic cash ledger, they can claim a refund. Details of any such refund claimed should be reported in this section.

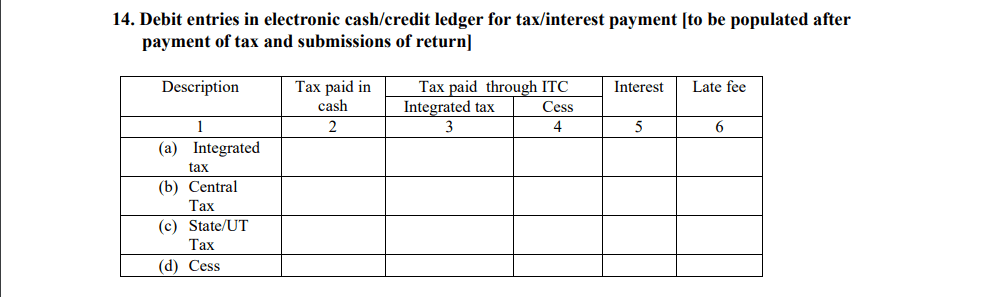

14. Debit Entries in Electronic Cash/Credit Ledger for Tax/Interest Payment (To be Populated After Payment of Tax and Submission of Return): This section will auto-populate with the debit entries from the taxpayer’s electronic cash or credit ledger once the return is submitted and the tax payments are made. This reflects the use of balances from these ledgers for paying taxes and interest.

Now that you have an understanding of the required details, we’ll proceed to the step-by-step guide to filing GSTR-5, which simplifies the entire process.

Steps to File GSTR-5

Filing GSTR-5 is an essential compliance requirement for non-resident taxable persons (NRTPs) operating in India. While the process may seem complex at first, this step-by-step guide will walk you through the process of filing the GSTR-5 return on the GST portal.

Step 1: Gather the Required Information and Documents

Before you begin the filing process, ensure you have all the necessary information and documents ready, including:

- GSTIN (Goods and Services Tax Identification Number)

- Details of outward supplies made during the tax period

- Details of inputs/capital goods imported

- Any applicable debit/credit notes

- Information on previous filings if you need to make amendments

- Tax liability and payment details, if applicable

Having these documents ready will help streamline the filing process.

Step 2: Log in to the GST Portal

To file GSTR-5, log in to the official GST Portal using your credentials:

- Visit the official GST website: https://www.gst.gov.in/

- Use your GSTIN, username, and password to log in.

- Once logged in, navigate to the dashboard where you’ll find the return filing options.

Step 3: Access GSTR-5 Return Filing Section

- From the dashboard, click on the ‘Services’ tab.

- Navigate to ‘Returns’ and select ‘Return Dashboard’ from the drop-down menu.

- Select the appropriate financial year and return filing period.

- Click on ‘Search’, and then select the option for ‘GSTR-5’.

This will open the GSTR-5 form, allowing you to start entering the required details.

Step 4: Fill in the Necessary Details

You’ll need to fill out the GSTR-5 form in several sections, as explained below:

- GSTIN and Taxpayer Information: Verify that your GSTIN and legal/trade name are auto-populated correctly.

- Inputs/Capital Goods from Overseas: Enter details of any imported inputs or capital goods, including Bill of Entry numbers and IGST paid.

- Outward Supplies: Fill in the details of all supplies made to both registered (B2B) and unregistered (B2C) persons, including invoice numbers and amounts.

- Amendments: If needed, make corrections or amendments to previously filed returns.

- Tax Liability: Enter your total tax liability, based on the outward supplies and amendments made during the tax period.

- Interest and Late Fee: If applicable, add any interest or late fee for delayed filing.

- Refunds: If you are claiming a refund from the electronic cash ledger, enter the amount here.

Step 5: Review and Submit the Return

Once all the details are entered:

- Review the entire form to ensure all information is correct. You can preview the return before final submission.

- Check for any errors or omissions, especially in the tax liability and outward supplies sections.

- After verifying the details, select the E-Acknowledgement checkbox and click ‘Submit’.

Note that once you submit the form, no further changes can be made, so it’s essential to double-check everything.

Step 6: Make the Payment of GST Liabilities (if applicable)

If you have a pending tax liability, you will need to make the payment before filing the return. Follow these steps:

- Click on the ‘Proceed to Pay’ option after submitting the form.

- Choose a suitable payment method, such as net banking, credit/debit card, or challan.

- Once payment is made, the system will update your tax payment in the electronic cash ledger.

Ensure that the payment is successful to avoid penalties for unpaid tax liabilities.

Step 7: Download Acknowledgement and Keep Records

After filing the return:

- Once the GSTR-5 is successfully filed, you will receive an Acknowledgement Reference Number (ARN).

- Download the acknowledgment receipt and keep it for your records.

- You can also download a PDF version of the filed return from the portal for future reference.

Having a record of the acknowledgment ensures that you can prove compliance in case of any future inquiries from the GST authorities.

Consequences of Not Filing or Delayed Filing of GSTR-5

Timely filing of GSTR-5 is crucial for maintaining compliance with India’s GST system. Failure to file GSTR-5 on or before the due date can lead to various financial and legal consequences. We will explore what happens if a non-resident taxable person (NRTP) fails to file GSTR-5 or delays the filing.

1. Penalties for Late Filing

The Indian GST system imposes penalties for late filing of returns, including GSTR-5. The penalty structure is as follows:

- Late Fee: A late fee of Rs. 100 per day (Rs. 50 under CGST and Rs. 50 under SGST) is applicable for each day of delay. The maximum late fee is capped at Rs. 5000.

- Nil Return Late Fee: If you do not have any transactions during the period, a reduced late fee of Rs. 20 per day is applicable (Rs. 10 under CGST and Rs. 10 under SGST) until the return is filed. This is applicable for filing nil returns.

Penalties can accumulate quickly if the return is not filed within a reasonable time. It is always better to file the return on time, even if there are no transactions to report.

2. Interest on Late Payment of Tax

In addition to the late filing fee, there is an interest charge of 18% per annum on any unpaid tax liability. The interest is calculated from the day after the due date (21st of the following month) until the tax is paid.

- Interest Calculation: Interest is calculated on the outstanding tax amount, starting from the day after the filing deadline to the actual payment date.

Example: If a non-resident taxable person has a tax liability of Rs. 10,000 and delays filing by 30 days, they would have to pay interest on the outstanding amount for those 30 days.

3. Inability to File Future Returns

If the current month’s GSTR-5 return is not filed, the non-resident taxable person will be unable to file returns for future months. The system will block any future filings until the pending return is submitted.

- Filing Block: This can disrupt the entire tax filing process for subsequent months and may lead to more significant compliance issues, particularly for businesses that operate regularly in India.

4. Possible Legal and Compliance Issues

Non-filing or delayed filing of GSTR-5 can result in further legal complications. Persistent non-compliance may lead to:

- GST Registration Suspension: The GST authorities may suspend the GST registration of the non-compliant taxpayer. This can halt the ability to conduct business legally in India.

- Legal Notices: Repeated non-compliance or failure to file returns may trigger notices from the GST department, requiring the non-resident taxable person to explain the reasons for non-compliance.

- Assessment by Tax Authorities: The tax authorities may assess the tax liability based on available information, and this could lead to higher tax assessments, penalties, or legal action.

What Happens if GSTR-5 is Filed Late?

Filing GSTR-5 on time is essential to avoid financial and compliance penalties. However, if you fail to file it by the due date, there are specific consequences, including the imposition of late fees and interest. Let’s see how penalties and interest are calculated and provide an example to make this clear.

1. Penalties and Interest Calculation

When a non-resident taxable person (NRTP) files GSTR-5 after the due date, both late fees and interest charges apply:

- Late Fee: As mentioned earlier, a late fee of Rs. 100 per day (Rs. 50 under CGST and Rs. 50 under SGST) is charged for every day of delay, up to a maximum of Rs. 5000.

- For nil returns (no taxable transactions), the late fee is Rs. 20 per day (Rs. 10 under CGST and Rs. 10 under SGST), up to a maximum of Rs. 5000.

- Interest on Late Payment: Interest is levied at a rate of 18% per annum on the outstanding tax liability. This interest is calculated from the day after the due date (21st of the following month) until the date the tax payment is made.

2. Example of Penalty and Interest Calculation for Delayed Filing

To make this clearer, let’s look at an example:

Scenario:

A non-resident taxable person (NRTP) with a tax liability of Rs. 20,000 for the month of September delays filing their GSTR-5 return by 30 days.

Here’s how the penalties and interest would be calculated:

- Late Fee:

Late fee = Rs. 100 per day (50 under CGST + 50 under SGST)

Delay = 30 days

Total Late Fee = Rs. 100 × 30 = Rs. 3000 - Interest on Late Payment:

Interest rate = 18% per annum

Tax liability = Rs. 20,000

Delay = 30 days

Interest = (Tax Liability × Interest Rate × Delay in Days) / 365

Interest = (20,000 × 18 × 30) / 365 = Rs. 295.89 - Total Penalty and Interest

Late Fee = Rs. 3000

Interest = Rs. 295.89

Total = Rs. 3,295.89

This total amount would need to be paid in addition to the tax liability of Rs. 20,000. The longer the delay in filing, the higher the total penalty and interest.

3. Late Fee for Nil Returns

If you need to file a nil return (i.e., no business transactions occurred during the month), the late fee is reduced:

- Rs. 20 per day (Rs. 10 under CGST and Rs. 10 under SGST).

- The maximum late fee remains Rs. 5000.

For example, if an NRTP files a nil GSTR-5 return 15 days late, the late fee would be:

Late Fee = Rs. 20 per day × 15 days = Rs. 300

No interest applies in this case because no tax is owed.

How to Amend GSTR-5 Filings?

It’s possible that after filing your GSTR-5 return, you may realize that some details were incorrectly entered, or you missed adding certain information. Fortunately, the GST system allows for amendments to be made in subsequent returns. Let’s understand how to amend previous filings of GSTR-5 and the types of changes that are allowed.

1. Steps to Amend Previous Period Filings

Amendments to GSTR-5 can be made to correct any mistakes or omissions from previously filed returns. Here’s a step-by-step guide to amending GSTR-5:

- Step 1: Log in to the GST Portal

Begin by logging in to the GST portal using your GSTIN and password, just as you would when filing a new return. - Step 2: Navigate to the Return Dashboard

After logging in, click on “Services” and then select “Returns Dashboard” from the dropdown menu. - Step 3: Select the GSTR-5 Form for Amendment

Choose the relevant tax period in which you want to make the amendments and select the option for GSTR-5. You will see an option to prepare amendments for earlier returns. - Step 4: Make the Necessary Amendments

Here, you can make corrections or adjustments in the following areas (which we will explore in detail below). Be sure to carefully review each section where changes are required. - Step 5: Submit the Amended Return

Once all necessary changes are made, review the amendments thoroughly to ensure accuracy. Submit the return and keep a copy of the updated return for your records.

2. Types of Amendments Allowed

There are certain types of amendments that you can make to your previously filed GSTR-5 returns:

- Inward Supplies (Imports):

Amendments can be made to the details of inputs or capital goods imported from overseas. This includes changes to the bill of entry, taxable value, and IGST or cess paid. - Outward Supplies (Sales):

Changes can be made to the details of taxable outward supplies made to registered or unregistered persons, such as amendments to invoice details or the amounts listed. - Amendments to Debit/Credit Notes:

If you have issued debit or credit notes for earlier supplies and need to correct the amounts or add new notes, these details can be amended in the relevant section. - Amendments to Tax Liability:

Any changes to the calculated tax liability, including adjustments based on amended sales or purchase data, can be made. This ensures that the right amount of tax is declared and paid.

3. Time Limit for Filing Amendments

Amendments to GSTR-5 can only be made in the returns filed for subsequent months. It’s important to note that amendments can be made:

- Before the filing of the annual return or

- By the September return following the end of the financial year, whichever is earlier.

This time limit is critical, as any errors identified after this period cannot be corrected through the amendment process and may result in non-compliance penalties.

The ability to amend GSTR-5 filings provides flexibility and ensures that businesses can correct their records without significant repercussions. However, the window for making amendments is limited, so it’s crucial to review each month’s return carefully before submitting it. If amendments are necessary, making them promptly within the allowed period helps avoid further issues down the road.

Key Differences Between GSTR-5 and GSTR-5A

| Aspect | GSTR 5 | GSTR 5A |

| Who Files It? | Non-resident taxable persons (NRTP) supplying goods/services | Non-resident service providers offering OIDAR services |

| Purpose | Reports sales, purchases, and import of goods | Reports electronic services supplied to unregistered customers in India |

| Taxable Supplies | Covers both goods and services | Only for services provided electronically |

| Registration Requirement | Temporary GST registration required | Special registration for OIDAR service providers required |

| Due Date | 20th of the following month | 20th of the following month |

| Nil Return Requirement | Nil returns are not mandatory | Nil returns are mandatory even if no services are provided in a month |

Conclusion

The importance of understanding and complying with GSTR-5 filing cannot be overstated, especially for non-resident taxable persons (NRTPs) who engage in business transactions in India. By filing GSTR-5 on time, businesses ensure they remain compliant with India’s Goods and Services Tax (GST) laws, avoid unnecessary penalties, and maintain a smooth operation in the Indian market.

Whether it’s filing regular monthly returns, making amendments to past filings, or dealing with potential late fees and penalties, knowing the intricacies of GSTR-5 filing will significantly benefit any non-resident entity. The ability to access the right documents, correctly interpret tax liabilities, and submit forms through the GST portal streamlines the tax filing process and keeps businesses running smoothly.

Key Takeaways:

Timely Filing: Filing GSTR-5 by the 20th of every month ensures compliance and avoids late fees or interest charges.

Accurate Information: Ensure that all supply, import, and tax information is correct and well-documented before submitting.

Amendments: Corrections can be made in subsequent returns if necessary, ensuring flexibility and transparency in the filing process.

Penalties for Non-Compliance: Delayed or missed filings can result in fines, interest on tax liability, and potential legal consequences.

Resources Available: Tools such as GST software can greatly simplify the process, helping to ensure accurate and timely filings.

For businesses operating in India, keeping up with GST requirements, especially as a non-resident taxable person, is essential to smooth and hassle-free operations. By adhering to the guidelines and using modern tools and resources, non-residents can continue to engage with the Indian market confidently and compliantly.

Resources and Tools for Simplifying GSTR-5 Filing:

- GST Portal: The official platform for filing GSTR-5 returns, available online.

- GST Software: Platforms like LEDGERS or automated GST tools help manage invoices and prepare filings automatically.

- Consultations: Engage with tax professionals or GST consultants if any uncertainties arise during the filing process.

In conclusion, staying compliant with GST norms through timely and accurate filing of GSTR-5 is crucial for all non-resident taxable persons operating in India. Whether you are a new business exploring the Indian market or an established entity, understanding and properly managing GSTR-5 filings will set the stage for a successful and legally compliant operation in the country.

Frequently Asked Questions (FAQs)

1. Can GSTR-5 Be Filed Offline?

No, GSTR-5 cannot be filed offline. It must be filed online through the GST portal. The authorized person will need to log in using their GST credentials, fill in the details as per the guidelines, and submit the form online.

2. What is the Maximum Late Fee for GSTR-5?

The maximum late fee for GSTR-5 is Rs. 5,000. A penalty of Rs. 100 per day (Rs. 50 under CGST and Rs. 50 under SGST/UTGST) will be imposed until the return is filed. For nil returns, the late fee is Rs. 20 per day (Rs. 10 under CGST and Rs. 10 under SGST/UTGST). The fee accumulates from the due date (20th of the following month) until the return is filed, but it cannot exceed Rs. 5,000.

3. Is It Mandatory to File GSTR-5 Even with No Business Transactions?

No, it is not mandatory for NRTPs to file GSTR-5 if there have been no transactions for the month. However, in cases where a return is required, GSTR-5 must be filed.

For OIDAR service providers (GSTR-5A), a Nil return is mandatory even when no transactions have occurred during the month.

4. What Documents Are Needed for GSTR-5 Filing?

To file GSTR-5, non-resident taxable persons will need the following documents and information:

- GSTIN: Your unique GST identification number.

- Invoices: Both inward and outward supply invoices for the month.

- Bill of Entry: In case of imports, details related to the bill of entry for goods brought into India.

- Payment Receipts: Any payment-related documents for the taxes paid.

- Digital Signature Certificate (DSC): For submitting returns in cases where a DSC is mandatory (such as for companies).

5. What Happens if GSTR-5 is Not Filed on Time?

Failure to file GSTR-5 on time can lead to the following consequences:

- Late Fee: A penalty of Rs. 100 per day, with a maximum of Rs. 5,000.

- Interest on Tax Payment: Interest at 18% per annum will be charged on any unpaid GST liabilities.

- Filing Block for Future Returns: You will not be able to file future returns until the pending GSTR-5 is submitted.

- Legal Issues: Continued non-compliance can lead to further penalties and legal notices from tax authorities.

6. Can GSTR-5 Be Amended After Filing?

Yes, GSTR-5 can be amended in the subsequent filing period if any discrepancies are identified in previous filings. However, these amendments can only be made for outward and inward supply details, and not for other elements such as tax paid or refunds.

7. What is the Difference Between GSTR-5 and GSTR-5A?

The main difference between GSTR-5 and GSTR-5A lies in who is required to file each return:

- GSTR-5: Filed by non-resident taxable persons (NRTP) engaged in supplying goods or services in India.

- GSTR-5A: Filed by non-resident OIDAR service providers who offer electronic services to unregistered consumers in India.

Additionally, GSTR-5 does not require a Nil return, while GSTR-5A mandates a Nil return even if no transactions occurred during the period.

8. Is a Digital Signature Mandatory for Filing GSTR-5?

Yes, a Digital Signature Certificate (DSC) is mandatory for filing GSTR-5 in cases where the taxpayer is a company or an LLP (Limited Liability Partnership). For other types of entities, filing can be completed using an Electronic Verification Code (EVC).

Related Posts:

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

Complete Guide to GSTR-4A for Composition Taxpayers

Complete Guide to GSTR-4A for Composition Taxpayers

Creating A Stellar Business Profile: A Step-by-step Guide

Creating A Stellar Business Profile: A Step-by-step Guide

VAT Return in UAE: What You Need to Know

VAT Return in UAE: What You Need to Know

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

E-Way Bill Threshold: A State-by-State Guide

E-Way Bill Threshold: A State-by-State Guide

GSTR-1 Explained: Everything You Need To Know

GSTR-1 Explained: Everything You Need To Know

The Ultimate Guide to the Best Invoicing and Client Management Software (Updated 2024 List)

The Ultimate Guide to the Best Invoicing and Client Management Software (Updated 2024 List)

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

Best Accounting Software in India: Features, Pricing, Reviews, and more (Updated 2024 List)

Best Accounting Software in India: Features, Pricing, Reviews, and more (Updated 2024 List)

Basic Finance Terms Every Small Business Owner Should Know

Basic Finance Terms Every Small Business Owner Should Know