Cross-border services are becoming increasingly common, and with them comes the need for specific tax regulations. One such important regulation under India’s Goods and Services Tax (GST) system is GSTR-5A.

GSTR-5A is a return form specifically designed for non-resident Online Information and Database Access or Retrieval (OIDAR) service providers. These are businesses located outside of India that provide digital services to Indian consumers.

Understanding GSTR-5A is crucial for both non-resident service providers and the individuals or entities receiving these services in India. It ensures compliance with Indian GST regulations and helps maintain transparency in the reporting of services provided from outside the country.

What is GSTR-5A?

GSTR-5A is a return form specifically for non-resident service providers supplying Online Information and Database Access or Retrieval (OIDAR) services to unregistered persons in India. It ensures that non-resident providers of digital services—such as e-books, streaming platforms, software downloads, and cloud-based services—comply with Indian tax laws by collecting and remitting GST on services consumed in India.

What is OIDAR?

OIDAR stands for Online Information and Database Access or Retrieval Services. These services are delivered digitally with minimal human intervention and are consumed online without any physical interaction. Examples include streaming services (e.g., Netflix, Amazon Prime), cloud storage, online advertising, and e-learning platforms. OIDAR services are taxed under GST to ensure that digital services consumed by Indian residents contribute to the country’s tax revenue, even if the provider is based outside India.

Understanding OIDAR Services

OIDAR services refer to digital services provided through the internet or electronic networks. These services require minimal human intervention and are commonly consumed over the web. Examples of OIDAR services include:

- Access to e-books, music, and videos: When an individual purchases an e-book or subscribes to a digital media service, these are considered OIDAR services.

- Cloud-based services: Services that provide storage or software access via the cloud, such as hosting or software-as-a-service (SaaS), fall under OIDAR.

- Online advertising services: Digital advertising platforms offering their services online to Indian customers.

- Online gaming: Platforms that offer interactive games or downloadable game content over the internet.

- Streaming services: Platforms providing movies, TV shows, and other digital content fall into this category.

Who Needs to File GSTR-5A?

Non-resident service providers who offer OIDAR services to unregistered persons in India are required to file GSTR-5A. This includes:

- Unregistered Individuals: Consumers who use digital services (e.g., downloading e-books or streaming movies) but are not registered under GST.

- Government Bodies and Local Authorities: Non-resident service providers offering services to unregistered government bodies or local authorities must also file GSTR-5A, even though these entities are not businesses.

- Non-Taxable Online Recipients: These are individuals or non-commercial entities receiving OIDAR services for non-business purposes. In such cases, the non-resident provider is responsible for paying GST.

Why is GSTR-5A Important?

GSTR-5A is crucial because it ensures that non-resident service providers contribute their fair share of taxes when supplying digital services to Indian consumers. In an increasingly digital economy, where cross-border online transactions are common, GSTR-5A helps the Indian government track and collect taxes on services consumed in the country.

The Role of GST in OIDAR Services: The Indian government requires non-resident service providers to collect and remit GST on services provided to unregistered Indian consumers. This is done to ensure that digital services consumed within India contribute to the country’s tax revenue, irrespective of the service provider’s physical presence. Filing GSTR-5A ensures that GST is accurately collected on cross-border digital transactions, helping maintain compliance with Indian tax laws and providing a clear record of the services offered.

Key Features of GSTR-5A

GSTR-5A facilitates the filing and reporting of taxes by these non-resident OIDAR service providers. The form allows them to disclose the details of the services they have provided and calculate the amount of GST payable on those services. The following are some important features of GSTR-5A:

1. Mandatory for Non-Resident OIDAR Service Providers

Non-resident digital service providers who supply services to unregistered persons in India must file GSTR-5A. This is applicable even if no transactions have been made during a particular period.

2. Monthly Filing Requirement

GSTR-5A is a monthly return, meaning it needs to be filed every month by the 20th day of the following month. For example, if a service provider has provided services in the month of August, they must file the GSTR-5A by the 20th of September.

3. No Input Tax Credit (ITC)

Since OIDAR service providers operate from outside India, they cannot claim any Input Tax Credit (ITC) for GST paid on services they may have consumed within India. Therefore, the electronic credit ledger is not maintained for GSTR-5A filings.

4. Nil Return Filing

Even if no services were provided during a particular tax period, non-resident service providers are required to file a nil return for GSTR-5A.

Eligibility to File GSTR-5A

GSTR-5A is specifically designed for non-resident OIDAR (Online Information and Database Access or Retrieval) service providers who offer their services to unregistered individuals or entities in India. To understand the eligibility, it is important to define who qualifies as a non-resident OIDAR service provider and the conditions under which they are required to file GSTR-5A.

Pre-requisites for Filing GSTR-5A

To file GSTR-5A, the following conditions must be met:

- GSTIN Registration:

The non-resident service provider must be registered under the GST system in India and hold a valid GSTIN (Goods and Services Tax Identification Number). This is mandatory for filing returns, including GSTR-5A.

- Valid Login Credentials:

The service provider must have a valid login ID and password to access the GST portal. This ensures secure access for filing the return.

- PAN or Passport:

Non-resident service providers must have a valid Permanent Account Number (PAN) or passport details for registration. This enables the service provider to obtain GSTIN and file returns.

- Digital Signature Certificate (DSC) or Electronic Verification Code (EVC):

A valid Digital Signature Certificate (DSC) or an Electronic Verification Code (EVC) is required to authenticate the filing. This ensures that the return is legally signed by the authorized person.

Filing Procedure for GSTR-5A

Filing GSTR-5A is a crucial task for non-resident OIDAR service providers. The process is designed to ensure that the service providers correctly declare their taxable supplies made to unregistered individuals or entities in India. Let’s discuss the step-by-step guide on how to file GSTR-5A through the GST portal.

Step-by-Step Guide to Filing GSTR-5A

Step 1: Access the GST Portal

To file GSTR-5A, the non-resident OIDAR service provider must first access the official GST portal.

- Visit the GST portal at www.gst.gov.in.

- Log in using your valid GSTIN (Goods and Services Tax Identification Number) and password.

Once logged in, follow these steps to reach the GSTR-5A form:

- Go to the Services menu on the top navigation bar.

- Select Returns from the dropdown menu.

- Click on Returns Dashboard from the list.

- In the Returns Dashboard, select the Financial Year and Return Filing Period for which you want to file the return.

- After selecting the return period, click on Search.

Step 3: Select GSTR-5A Form

- In the list of available forms, locate GSTR-5A under the Online Information and Database Access or Retrieval (OIDAR) Services section.

- Click on Prepare Online.

Step 4: Fill in the Required Details

The GSTR-5A form consists of several sections where the non-resident OIDAR service provider must enter relevant details.

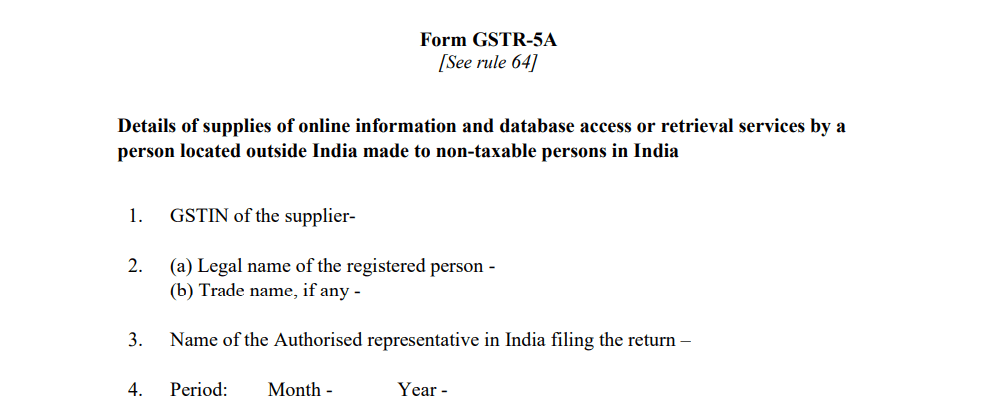

Table 1: GSTIN

This section will be auto-populated with the GSTIN details of the non-resident OIDAR service provider.

Table 2: Legal Name and Trade Name (if any)

- The legal name and trade name (if any) of the registered person will also be auto-filled based on the information in the GST portal.

Table 3: Authorized Representative Name

- Enter the name of the authorized representative responsible for filing the return. If the service provider has appointed an agent in India, their details must be provided here.

Table 4: Filing Period

- Enter the period for which the return is being filed, i.e., the Month and Year for which GSTR-5A is applicable.

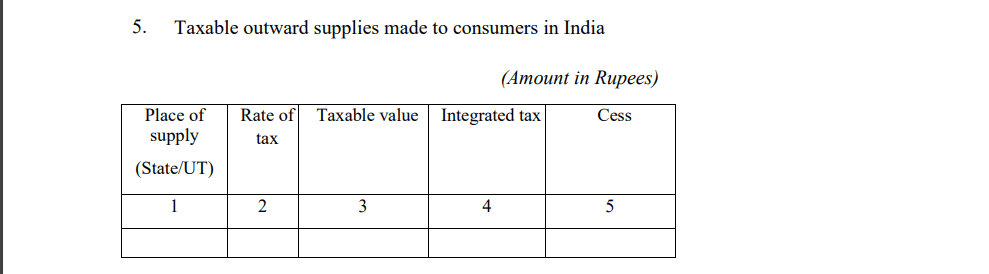

Table 5: Taxable Outward Supplies to Non-Taxable Persons in India

This section is critical as it contains the details of all taxable outward supplies made by the non-resident service provider to unregistered persons or entities in India.

- Place of Supply: Select the place where the supply was made in India.

- Taxable Value: Enter the total value of the taxable outward supplies.

- Tax Rate: Select the applicable tax rate for the services provided.

- Integrated Tax (IGST): Based on the taxable value and tax rate, enter the integrated tax amount applicable to the outward supplies.

- Cess: If applicable, enter the cess amount.

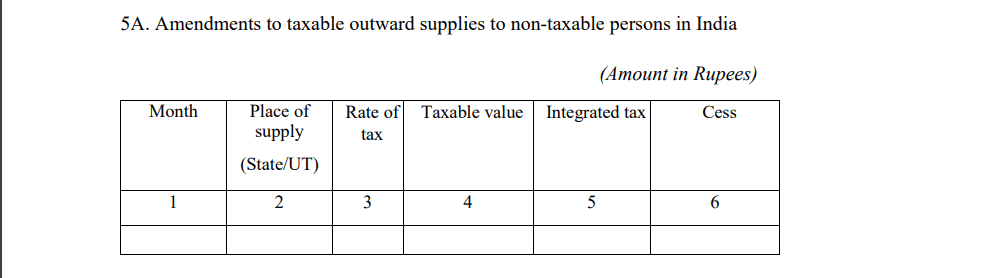

Table 5A: Amendments to Outward Supplies from the Previous Period

If there are any amendments or corrections to the taxable outward supplies from the previous period, they must be reported in this section.

- Provide details of the amended taxable value, amended tax rate, and corrected IGST.

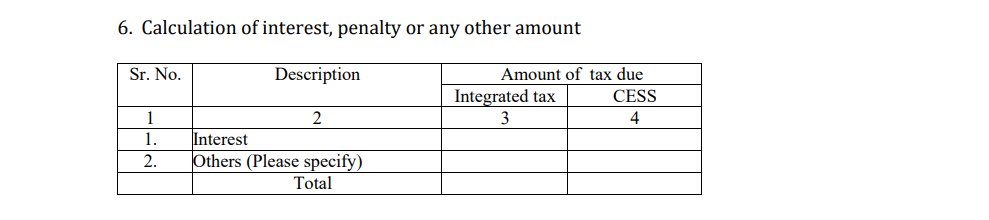

Table 6: Calculation of Interest, Penalty, or Other Amounts

In this table, calculate and report any interest, penalties, or other charges payable due to late filing or non-compliance.

- Interest: Enter the amount of interest calculated for any late payments.

- Penalty: Specify any penalty amounts due for late filing or errors.

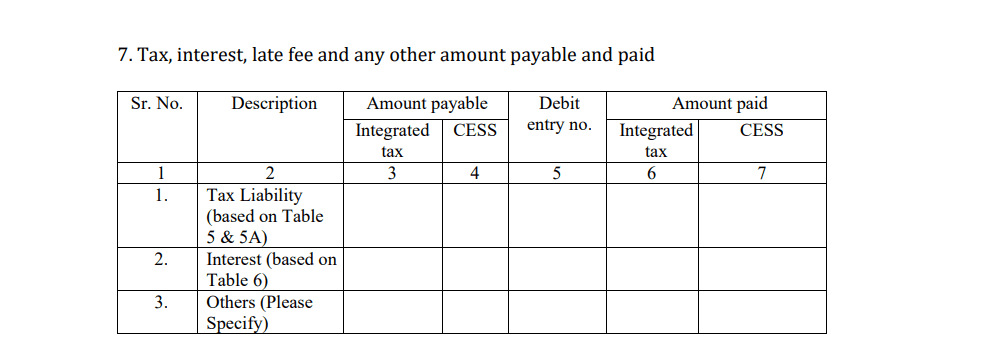

Table 7: Details of Late Fee, Tax, Interest, and Other Payable Amounts

The GST portal will auto-populate this section based on the entries made in Table 5, Table 5A, and Table 6.

- Tax: This includes the total tax liability (IGST).

- Interest: The interest payable due to late payments.

- Late Fees: The late fees applicable for delayed filing.

- Total Payable: The total amount payable, including tax, interest, and any late fees.

Step 5: Preview the Draft

Before finalizing the return, it’s advisable to preview the draft version of GSTR-5A. Follow these steps:

- Click on Preview Draft GSTR-5A.

- The system will generate a PDF file of the return for review.

- Verify all details, especially taxable outward supplies, and tax amounts, before proceeding to file.

Step 6: Payment of Tax and Offset Liabilities

Before filing GSTR-5A, ensure that the Electronic Cash Ledger has sufficient balance to pay off the tax liability.

- If the balance is insufficient, generate a challan and make the necessary payment through the GST portal.

- Once the payment is made, proceed to offset the tax liabilities by clicking on Offset Liability.

Step 7: File GSTR-5A

After reviewing the draft and ensuring all tax liabilities are paid, follow these steps to file the return:

- Click on Proceed to File.

- Choose between File with DSC (Digital Signature Certificate) or File with EVC (Electronic Verification Code), depending on your preference.

- Complete the verification process using the selected method.

Step 8: Acknowledgement

Once the filing is complete, the GST portal will generate an Acknowledgement Reference Number (ARN). The service provider will also receive a confirmation email and SMS with the ARN.

Important Points to Remember:

– Nil Return Filing: If no services were provided during the tax period, a nil return must still be filed.

– Filing Deadline: GSTR-5A must be filed on or before the 20th day of the month following the taxable period.

– Amendments: Any corrections or amendments to the return must be made in subsequent filings through Table 5A.

– Late Fees: Ensure timely filing to avoid late fees, which are ₹200 per day for regular returns and ₹100 per day for nil returns.

What Happens if GSTR-5A is Not Filed?

Failure to file GSTR-5A on time or in a proper manner can result in penalties and interest being levied. The key consequences include:

- Late Fees:

A late fee of ₹200 per day is applicable (₹100 for CGST and ₹100 for SGST) for normal returns and ₹100 per day for nil returns (₹50 for CGST and ₹50 for SGST).

- Inability to File for Future Periods:

If the return for a particular tax period is not filed, the provider will not be able to file the return for subsequent periods until the previous ones are cleared.

- Legal Consequences:

Continuous failure to comply with GST filing requirements could lead to additional penalties or legal action from the authorities.

Important Points to Remember:

No Input Tax Credit (ITC): OIDAR service providers cannot claim Input Tax Credit on any goods or services they might consume within India. Thus, they cannot offset any tax liability using credits from previous purchases.

Filing Requirement Even for Nil Returns: Even if no services are provided during a particular tax period, the service provider is still required to file a nil GSTR-5A return.

Consequences of Non-Filing or Late Filing of GSTR-5A

Non-resident OIDAR service providers must comply with the GSTR-5A filing requirements on time to avoid penalties and legal consequences. Failure to file GSTR-5A within the stipulated deadline can lead to significant financial penalties, which could burden businesses and impact their operations. Let’s explore the consequences of non-filing or late filing and emphasize the importance of timely compliance.

The penalty for late filing of GSTR-5A is as follows:

- For normal returns, a late fee of Rs. 50 per day is applicable (Rs. 25 for CGST and Rs. 25 for SGST).

- For NIL returns, a reduced late fee of Rs. 20 per day is applicable (Rs. 10 for CGST and Rs. 10 for SGST).

The late fee is charged from the day after the due date until the date of filing the return.

Impact on Business Operations

Timely filing of GSTR-5A is crucial for non-resident OIDAR service providers, as non-compliance can have a direct impact on business operations. Some of the consequences include:

- Accrual of Penalties: As mentioned above, late fees for non-filing or late filing can add up quickly. This results in unnecessary financial strain on the service provider.

- Restricted Operations: Persistent non-compliance may lead to additional scrutiny by GST authorities, which could hinder business activities.

- Loss of Reputation: Non-compliance with tax laws can harm the service provider’s reputation, especially if the provider is operating in multiple jurisdictions. This can affect the trust and reliability that clients place in the business.

Suspension of GST Registration

In cases of prolonged non-compliance, where the non-resident OIDAR service provider continuously fails to file GSTR-5A for consecutive tax periods, the GST authorities may take action by suspending the provider’s GST registration. Suspension of GST registration effectively halts the service provider’s ability to legally conduct business in India, leading to the following issues:

- Inability to Conduct Business: Without an active GST registration, the service provider cannot provide services or issue valid tax invoices.

- Loss of Clients: Clients may be hesitant to work with a service provider who is not compliant with tax regulations, which can result in the loss of business opportunities.

Interest on Late Payment of Taxes

In addition to late fees, non-resident OIDAR service providers are also liable to pay interest on any unpaid tax liability that remains outstanding after the filing due date. The interest is calculated as follows:

- Interest Rate: 18% per annum on the outstanding tax amount.

- Calculation: The interest is calculated from the day after the due date until the date on which the tax is paid.

For example, if a service provider owes ₹50,000 in taxes for a specific period and pays the tax 10 days after the due date, the interest will be calculated as follows:

Interest = ₹50,000 x (18/100) x (10/365) = ₹246.57

This interest adds to the overall financial burden of the provider and emphasizes the importance of making timely payments.

Legal Actions and Prosecution

In extreme cases of non-compliance, especially where there is intentional tax evasion, the GST authorities have the power to initiate legal proceedings against the non-resident service provider. The consequences of such actions may include:

- Prosecution: Repeated non-compliance or fraudulent activities can lead to criminal prosecution, resulting in fines, penalties, or imprisonment.

- Asset Seizure: In cases of severe non-payment of taxes, the GST authorities may resort to seizing the assets of the service provider in India to recover the dues.

- Revocation of GST Registration: Continuous non-compliance could lead to the permanent revocation of the GST registration, effectively preventing the service provider from doing business in India.

Importance of Timely Filing and Compliance

To avoid the above penalties and consequences, it is essential for non-resident OIDAR service providers to:

- Maintain Proper Records: Ensure that all outward supplies, taxes, and payments are accurately recorded and updated in the system.

- Set Reminders for Deadlines: Mark key dates on a calendar and set reminders to ensure that the GSTR-5A return is filed before the 20th of each month.

- Ensure Sufficient Balance in the Electronic Cash Ledger: Before filing the return, ensure that the Electronic Cash Ledger has sufficient funds to offset the tax liability.

- Seek Professional Help: In cases where the filing process seems complex or unclear, consider seeking assistance from a tax professional to ensure timely compliance and avoid penalties.

Key Differences Between GSTR-5 and GSTR-5A

| Criteria | GSTR-5 | GSTR-5A |

|---|---|---|

| Nature of the Taxpayer | Filed by non-resident taxable persons (NRTPs) supplying goods/services in India. | Filed by non-resident OIDAR service providers offering digital services in India. |

| Scope of Supply | Covers goods and services provided to registered/unregistered recipients. | Focuses on online services provided to unregistered recipients. |

| Reporting Period | Must be filed by the 20th day of the month following the relevant tax period. | Must be filed by the 20th day of the month following the relevant tax period. |

| Eligibility | Applies to non-resident taxable persons supplying taxable goods/services. | Applies to non-resident OIDAR service providers offering electronic services. |

| Input Tax Credit (ITC) | NRTPs can claim ITC for purchases made during temporary operations in India. | No ITC is available, all taxes must be paid through the Electronic Cash Ledger. |

| Goods vs. Services | Covers both goods and services supplied by NRTPs. | Only covers online services provided by OIDAR service providers. |

| Example Use Cases | Foreign company selling goods at an Indian trade fair or providing consultancy services. | Online service providers offering digital content, cloud storage, or streaming services. |

| Amendments and Adjustments | Allows amendments to previously filed returns, adjusting outward supplies and data. | Allows amendments, particularly in Table 5A, for correcting taxable outward supplies. |

| Late Fees and Penalties | ₹200 per day penalty for late filing, capped at ₹10,000; ₹100 for nil return. | ₹200 per day penalty for late filing, capped at ₹10,000; ₹100 for nil return. |

Frequently Asked Questions (FAQs)

1. What is the difference between GSTR-5 and GSTR-5A?

GSTR-5 is filed by non-resident taxpayers who supply goods or services (or both) to persons in India. GSTR-5A, on the other hand, is specific to non-resident OIDAR service providers who offer digital services to unregistered persons in India.

2. Can a service provider claim Input Tax Credit (ITC) under GSTR-5A?

No, ITC cannot be claimed under GSTR-5A. The form is used exclusively for reporting the supply of services to unregistered persons in India, and no credit ledger is maintained.

3. What happens if I miss the deadline for filing GSTR-5A?

If you miss the filing deadline, you will incur a late fee. The late fee is ₹200 per day for a regular return and ₹100 per day for a NIL return. The late fee is capped at ₹10,000 per return.

4. Can I file GSTR-5A if I haven’t filed the previous month’s return?

No, the current period’s return cannot be filed unless all previous returns have been submitted. You must clear all previous tax liabilities before filing the current GSTR-5A return.

5. Do I need to file GSTR-5A if there were no transactions during the tax period?

Yes, you are still required to file a NIL return for the tax period. Failing to file a NIL return will still result in late fees if not submitted on time.

6. What happens after I file GSTR-5A?

Once you successfully file GSTR-5A, you will receive an Acknowledgement Reference Number (ARN) via email and SMS. This confirms that your return has been submitted successfully, and you can download the filed return for your records.

7. What services are classified as OIDAR under GST?

- OIDAR services include, but are not limited to:

- Providing access to e-books, music, and online advertisements.

- Cloud-based services and data storage.

- Online gaming services.

- Streaming of digital content such as movies and TV shows.

8. How do I make payments for GSTR-5A?

Payments can be made through the Electronic Cash Ledger on the GST portal. You can generate a challan and make payments via net banking, credit card, or other available options.

Conclusion

In conclusion, GSTR-5A plays a vital role in ensuring compliance for non-resident Online Information and Database Access or Retrieval (OIDAR) service providers offering services to unregistered persons in India. As the digital economy continues to expand, the GSTR-5A form serves as a crucial mechanism for the Indian government to track and tax services that are delivered remotely through the internet without any physical interaction.

Here are the key takeaways from the blog:

Mandatory Filing: GSTR-5A must be filed by non-resident OIDAR service providers every month, even if no business transactions occurred during the period.

Applicability: This return applies specifically to services provided to unregistered, non-taxable persons in India.

No Input Tax Credit: OIDAR service providers cannot claim ITC under GSTR-5A, and no electronic credit ledger is maintained for this form.

Late Fees: Delays in filing GSTR-5A will result in late fees, with specific charges applied depending on whether it’s a regular return or a NIL return.

Compliance: Filing GSTR-5A within the due date and keeping up with tax payments is essential to avoid penalties and remain compliant with GST regulations.

By following the guidelines provided in this blog, businesses can streamline their compliance process, ensuring they meet the necessary requirements under India’s Goods and Services Tax (GST) framework. This not only helps non-resident OIDAR service providers avoid hefty penalties but also contributes to the fair distribution of tax obligations across the global digital economy.

If you are a non-resident OIDAR service provider and unsure about filing your GSTR-5A return, it’s always a good idea to seek professional assistance to ensure full compliance and avoid any complications down the line.

Related Posts:

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

Complete Guide to GSTR-4A for Composition Taxpayers

Complete Guide to GSTR-4A for Composition Taxpayers

GSTR-1 Explained: Everything You Need To Know

GSTR-1 Explained: Everything You Need To Know

E-invoicing in Malaysia: What it is, Timeline, Key Features, and more

E-invoicing in Malaysia: What it is, Timeline, Key Features, and more

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

VAT Invoicing in UAE: Everything You Need to Know (Types, Formats, Rules, FAQs, and more)

VAT Invoicing in UAE: Everything You Need to Know (Types, Formats, Rules, FAQs, and more)

Best Accounting Software in India: Features, Pricing, Reviews, and more (Updated 2024 List)

Best Accounting Software in India: Features, Pricing, Reviews, and more (Updated 2024 List)

9 Ways To Make Your Invoicing Process More Effective

9 Ways To Make Your Invoicing Process More Effective

All Your Accounting FAQs Answered

All Your Accounting FAQs Answered

E-invoicing In GST: A Complete Guide

E-invoicing In GST: A Complete Guide

Filing ITR As A Freelancer? Know The Rules That Apply In India

Filing ITR As A Freelancer? Know The Rules That Apply In India