GSTR-7 is an important return form under the Goods and Services Tax (GST) system, specifically for entities required to deduct Tax Deducted at Source (TDS). This return is crucial for maintaining transparency in the GST regime and ensuring that tax is properly deducted and paid to the government on time.

The primary purpose of GSTR-7 is to make sure that taxpayers who are liable to deduct TDS under GST do so accurately and report it properly. This return helps the deductor (the person or entity who deducts tax) to stay compliant with GST regulations. Additionally, it allows the deductee (the supplier whose payment is subjected to TDS) to claim the Input Tax Credit (ITC) on the tax that has been deducted.

Timely filing of GSTR-7 is important for both the deductor and the deductee. If the deductor fails to file the return on time, they could face penalties and interest charges. For the deductee, the timely filing ensures that they can claim the deducted tax as ITC, which can be used to offset their own tax liabilities. Therefore, GSTR-7 plays a vital role in the smooth functioning of the GST system by facilitating proper tax deductions and claims.

What is GSTR-7?

GSTR-7 is a monthly return that must be filed by taxpayers who are required to deduct Tax Deducted at Source (TDS) under the Goods and Services Tax (GST) regime. This return serves as a record of the TDS deducted by the deductor and helps in reporting the TDS-related transactions to the government.

TDS under GST was introduced as a way to prevent tax evasion by ensuring that tax is deducted at the source of payment. When certain entities make payments to suppliers for goods or services, they are required to deduct a percentage of the payment as tax and deposit it with the government. This ensures that the tax liability is addressed at the time of the transaction itself, reducing the chances of tax evasion or under-reporting of taxes.

In GSTR-7, the following key details are reported:

- TDS deducted: The total amount of tax deducted from the supplier’s payment.

- TDS liability: The amount of TDS payable and already paid.

- Refunds: Any TDS refund claimed by the deductor.

- Other relevant transactions: Corrections or amendments to previous TDS details, and interest or late fees if applicable.

This form also ensures that the deducted TDS is credited to the supplier’s electronic ledger, enabling them to claim it as Input Tax Credit (ITC) when paying their own GST liabilities.

Who is Required to File GSTR-7?

GSTR-7 must be filed by entities that are mandated to deduct Tax Deducted at Source (TDS) under the GST regime, as outlined in Section 51 of the Central Goods and Services Tax (CGST) Act. These entities are primarily government bodies and specific organizations that regularly deal with large-scale transactions. The purpose of this requirement is to ensure that taxes are deducted at the source when payments are made, helping to reduce tax evasion and improve transparency in tax collection.

Here is a list of entities required to deduct TDS and file GSTR-7:

- Central and State Government departments: Government departments that make payments for goods or services are required to deduct TDS if the contract value exceeds ₹2.5 lakhs.

- Local authorities: Municipal corporations, town councils, and other local governing bodies that engage in significant procurements also fall under this category.

- Government agencies: Agencies or boards set up by the government that undertake public service projects or procurement activities are required to deduct TDS on eligible payments.

- Public Sector Undertakings (PSUs): Government-owned companies that operate commercially must comply with TDS regulations under GST for payments made to suppliers.

- Societies registered under the Societies Registration Act, 1860: Societies that are established or funded by the government for public welfare purposes are also obligated to deduct TDS under GST.

- Other specified entities as notified by the government: The government may, from time to time, notify additional entities that are required to deduct TDS under GST based on specific needs or circumstances.

These entities are responsible for filing GSTR-7 every month, reporting the details of the TDS deducted from payments made to suppliers.

When Should GSTR-7 be Filed?

GSTR-7 is a monthly return that must be filed by entities required to deduct Tax Deducted at Source (TDS) under the GST regime. This return must be submitted every month, even if no TDS deductions have been made during that period.

The deadline for filing GSTR-7 is the 10th of the following month after the tax period in which the TDS was deducted. Timely filing is crucial to avoid penalties and ensure that the deducted TDS is accurately reflected in the credit ledger of the deductee (the person or entity whose tax is being deducted).

Here’s an example of the due dates for filing GSTR-7:

If TDS was deducted in January 2024, the GSTR-7 return must be filed by 10th February 2024.

This regular and timely filing helps in maintaining compliance, ensuring that both deductors and deductees have a clear record of the TDS deducted and credited.

Key Components of GSTR-7

GSTR-7 consists of several important sections that must be filled accurately by the tax deductor to ensure proper reporting of TDS (Tax Deducted at Source) under GST. Each of these components plays a crucial role in providing detailed information about the TDS deductions and payments made during the tax period.

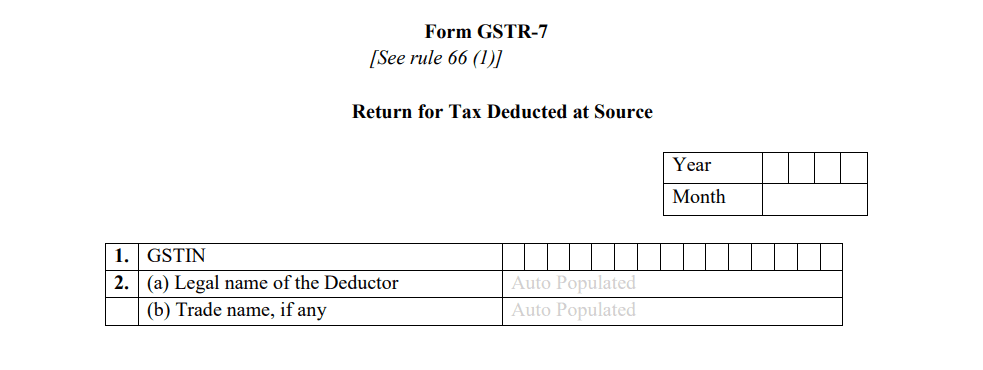

- GSTIN (Goods and Services Tax Identification Number):

This is a unique 15-digit number assigned to every registered taxpayer under GST.

The GSTIN of the deductor (the person or entity deducting TDS) is auto-populated in the GSTR-7 form based on their GST registration.

- Legal Name of Deductor:

The legal name of the tax deductor is also auto-populated in the form when logged into the GST portal.

This name is based on the information provided during the GST registration process.

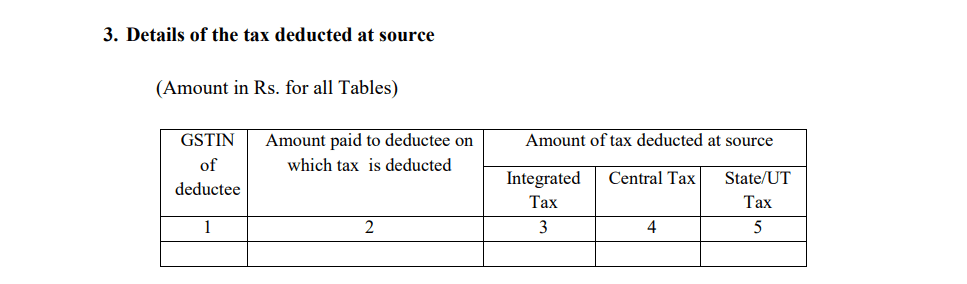

- TDS Details:

This section captures detailed information regarding the TDS deductions made by the deductor:

- GSTIN of the Deductee: The GST identification number of the supplier or person from whom the tax is being deducted.

- TDS Deducted on Payments: This includes the amount of TDS deducted from the payment made to the supplier or deductee.

- Breakdown of TDS: The deducted TDS is divided into CGST (Central GST), SGST (State GST), and IGST (Integrated GST), depending on whether the transaction is intra-state or inter-state.

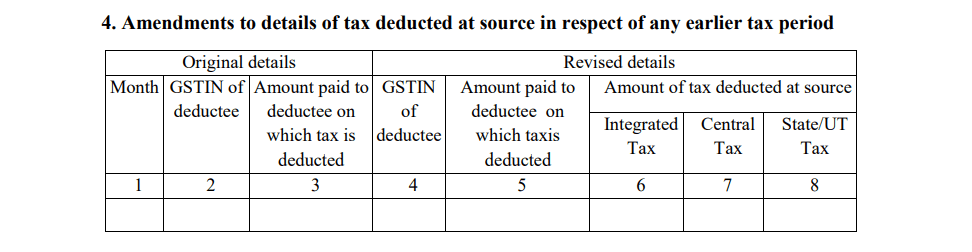

- Amendments:

In case there were errors or omissions in TDS details reported in previous returns, this section allows the deductor to correct those mistakes.

Amendments can include changes to the GSTIN of the deductee, TDS amounts, or any other relevant details from the earlier return period.

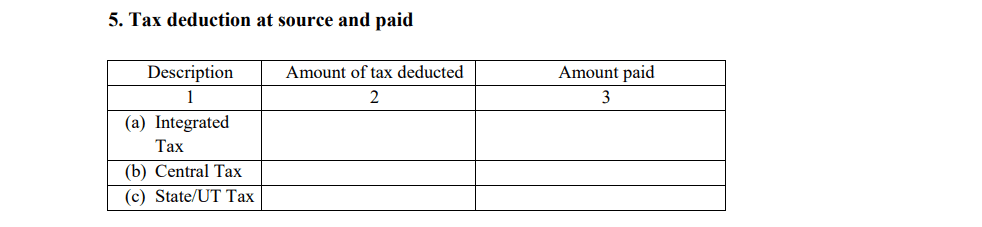

- Payment of TDS:

This section reports the details of TDS amounts that have been deducted and paid to the government.

It includes the breakdown of the amounts paid towards CGST, SGST, and IGST, ensuring that the deducted tax is properly credited to the government.

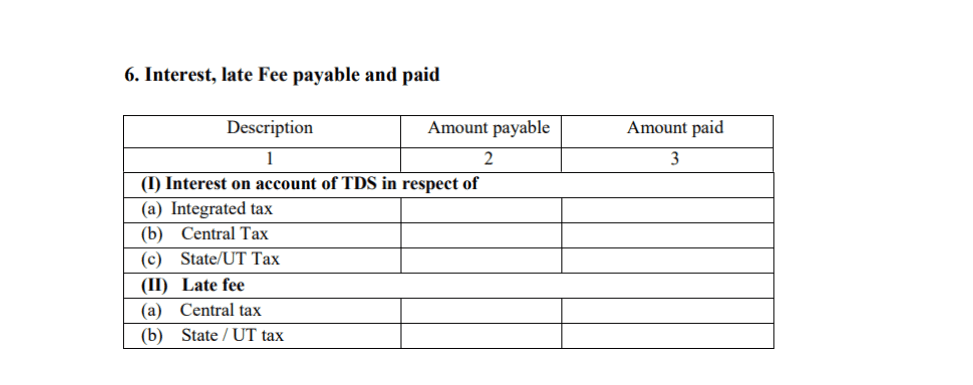

- Late Fee and Interest:

If the GSTR-7 filing has been delayed, or if there are any late payments, the deductor is liable to pay late fees and interest.

This section captures any such penalties, with a breakdown of the late fees and interest paid or payable under CGST and SGST.

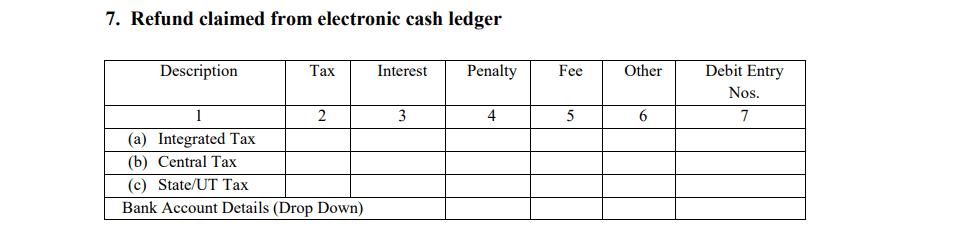

- Refund Claimed:

Sometimes, the deductor may have excess TDS in their electronic cash ledger, which can be claimed as a refund.

This section includes the details of any refund claimed by the deductor for the excess TDS that has been paid.

Each of these components ensures that TDS deductions are accurately tracked and that both the deductor and deductee have clarity on the tax deductions made under GST.

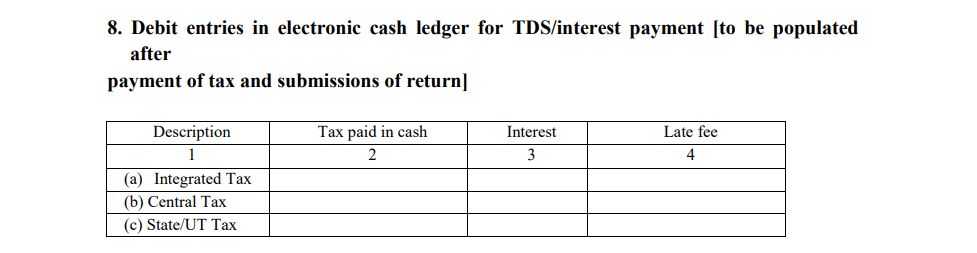

8. Debit entries in electronic cash ledgers for TDS/Interest payments

This section records the debit entries made in the electronic cash ledger for payments related to TDS and any applicable interest. It ensures that the amounts deducted as TDS or incurred as interest are properly accounted for and paid to the government. This section helps track the utilization of funds in the electronic cash ledger towards TDS and interest payments.

Steps to File GSTR-7

Filing GSTR-7 is a straightforward process, but it requires careful attention to ensure that all details related to Tax Deducted at Source (TDS) are accurately reported. Below are the steps to file GSTR-7 on the GST portal:

- Log in to the GST Portal:

Visit the official GST portal at www.gst.gov.in.

Enter your credentials: GSTIN, username, and password, followed by the CAPTCHA code.

Click on the “Login” button to access your account.

- Navigate to the Returns Dashboard:

After logging in, go to the “Services” section on the main dashboard.

Click on “Returns” and then “Returns Dashboard.”

Choose the relevant financial year and the return filing period for which you are submitting the GSTR-7.

- Select GSTR-7:

From the list of return forms, select GSTR-7.

Choose the “Prepare Online” option to begin the filing process.

- Enter TDS Details:

In this section, you will need to provide the details of the TDS you have deducted.

Include the GSTIN of the deductee (the supplier), the invoice number, the amount paid, and the amount of TDS deducted.

Break down the TDS into CGST, SGST, and IGST components as required.

Ensure that all supplier-wise details are accurate.

- Amendments to Previous TDS:

If any TDS details from previous returns need to be corrected, enter the original and revised details under the “Amendments” section.

Ensure that the corrections are valid and properly documented.

- Compute the TDS Liability:

After entering all the necessary TDS details, click on the “Compute Liability” button.

The system will automatically calculate the total TDS liability based on the information provided.

- Make Payment of TDS:

Check the available balance in your electronic cash ledger.

If additional funds are required, make the necessary payment to cover the TDS liability.

You can use the “Payment of Tax” option to clear the amount payable, including any interest or late fees.

- Preview the GSTR-7 Return:

Before submitting the form, click on the “Preview” button to review all the details entered.

Ensure that the details are accurate and that there are no errors or discrepancies.

- Submit the Return:

Once you are satisfied with the accuracy of the information, select the declaration checkbox.

Use either a Digital Signature Certificate (DSC) or an Electronic Verification Code (EVC) to authenticate and submit the return.

- Download the Acknowledgment:

After successful submission, an Application Reference Number (ARN) will be generated.

You will receive an acknowledgment via SMS and email.

Download the filed GSTR-7 return and the ARN for your records.

By following these steps, taxpayers can ensure that their GSTR-7 is filed correctly and on time, avoiding penalties and ensuring smooth compliance with GST regulations.

Late Fees and Penalties for Non-Compliance

Filing GSTR-7 on time is crucial for ensuring compliance with GST regulations. Missing the deadline can result in penalties, which include late fees and interest charges. Here’s what happens when the GSTR-7 filing deadline is missed:

- Late Fees:

For each day the GSTR-7 return is delayed, the following late fees apply:

- ₹100 per day for CGST

- ₹100 per day for SGST

This means a total of ₹200 per day will be charged until the return is filed.

- Maximum Penalty:

The late fees are capped, meaning the maximum penalty you can incur is ₹5,000 for CGST and ₹5,000 for SGST.

This brings the total maximum penalty to ₹10,000 for both CGST and SGST combined.

- Interest on Late Payments:

In addition to the late fees, interest must be paid on the outstanding TDS amount.

The interest rate is 18% per annum.

This interest is calculated from the day after the due date until the date of actual payment.

These penalties emphasize the importance of timely filing of GSTR-7. Deductors should ensure they meet the 10th of the month deadline to avoid these charges, ensuring smooth compliance with GST obligations.

Amendments and Revisions in GSTR-7

Mistakes in filing GSTR-7 can happen, but the GST system allows for corrections in future returns. Here’s how amendments and revisions work:

Process of Amending GSTR-7 for Errors:

Once GSTR-7 is submitted, it cannot be revised. However, any mistakes made in the current month’s filing can be corrected in the subsequent month’s return. To amend, the deductor needs to report the original transaction details along with the corrected information in the designated amendment section of the next GSTR-7 return. Correcting errors in a timely manner is crucial, as it prevents compliance issues and potential penalties. Early amendments also ensure the deductee can claim their Input Tax Credit (ITC) without delay, maintaining accurate tax records and minimizing complications such as discrepancies in ITC claims and scrutiny from tax authorities.

In essence, GSTR-7 is essential for both deductors and deductees. Filing it correctly promotes compliance with tax regulations, prevents penalties, and simplifies accounting processes for the deductor. For the deductee, it ensures transparency in TDS deductions, facilitates claiming ITC, and provides accurate tracking of tax credits, which is vital for financial management and smooth business operations.

Key Takeaways

- GSTR-7 Overview: GSTR-7 is a return form under GST for entities required to deduct TDS, ensuring tax transparency and compliance.

- Purpose: GSTR-7 ensures proper reporting of TDS by deductors, enabling deductees to claim Input Tax Credit (ITC) on the deducted amount.

- Filing Requirement: Entities like government bodies, PSUs, and specified societies must file GSTR-7 monthly.

- Due Date: GSTR-7 should be filed by the 10th of each month following the TDS transaction.

- Key Components: Form includes GSTIN, TDS details, amendments, payment records, and late fees.

- Filing Process: The return can be filed online via the GST portal, ensuring all TDS details are accurately entered.

- Penalties for Non-Compliance: Late fees are ₹200 per day, with a maximum cap of ₹10,000, plus 18% annual interest on unpaid TDS.

- Amendments: Mistakes in a filed GSTR-7 can be corrected in the following month’s return.

- Benefits: Filing GSTR-7 on time helps deductors stay compliant and allows deductees to claim their ITC without delays.

- Conclusion: GSTR-7 is vital for maintaining transparency in the TDS system, ensuring tax deductions are accurate and timely.

FAQs on GSTR-7

1. What happens if I miss the GSTR-7 deadline?

If you miss the GSTR-7 deadline, you will be subject to late fees of ₹100 per day for CGST and ₹100 per day for SGST, totaling ₹200 per day. The maximum penalty is ₹5,000 (₹10,000 combined for CGST and SGST). Additionally, interest at 18% per annum on the unpaid TDS amount will be charged until the amount is paid.

2. Can GSTR-7 be revised after submission?

No, GSTR-7 cannot be revised after submission. However, any errors made in the return can be corrected in the subsequent month’s GSTR-7 filing. It is important to ensure that all details are accurate before submission to avoid complications later.

3. How do I correct a mistake in GSTR-7?

Mistakes in GSTR-7 can be corrected in the following month’s return by updating the correct details in the “Amendment” section of GSTR-7. Ensure to check all information carefully before submitting the amended return.

4. What is the penalty for late filing of GSTR-7?

The penalty for late filing is ₹200 per day (₹100 for CGST and ₹100 for SGST), with a maximum cap of ₹5,000 (₹10,000 combined for CGST and SGST). Additionally, interest at 18% per annum is charged on the unpaid tax from the due date until the payment is made.

5. How can deductees claim ITC based on GSTR-7?

Deductees can claim Input Tax Credit (ITC) based on the details provided in Form GSTR-7A, which is auto-generated once the deductor files GSTR-7. The TDS reflected in GSTR-7A allows deductees to claim ITC, which can be used to offset their tax liability.

Related Posts:

GSTR 7A: Eligibility, Downloading Process, Deadline, Mistakes to Avoid, and FAQS

GSTR 7A: Eligibility, Downloading Process, Deadline, Mistakes to Avoid, and FAQS

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

GSTR 10: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 10: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Everything to know about GSTR 11:Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQs

Everything to know about GSTR 11:Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQs

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses