Form GSTR 7A is a system-generated TDS (Tax Deducted at Source) certificate under the Goods and Services Tax (GST) system. This certificate is automatically created once the deductor, the person or entity responsible for deducting TDS, files their GSTR-7 return on the GST portal. The deductee, the person or business whose income has been deducted, must accept the details uploaded by the deductor for the GSTR-7A certificate to be generated.

The GSTR-7A certificate is important for both deductors and deductees. It serves as proof that the TDS has been correctly deducted and reported. For the deductee, it is crucial because they can use this certificate to claim Input Tax Credit (ITC) and adjust it against their tax liabilities. Without GSTR-7A, the deductee may not be able to claim the credit for the tax deducted.

This streamlined process ensures that TDS deductions under GST are tracked efficiently, benefiting both parties involved.

Who Needs to Get GSTR 7A?

GSTR-7A is specifically issued to those who deduct TDS (Tax Deducted at Source) under the GST system. This includes individuals or organizations that have been given the responsibility to deduct tax from payments made to suppliers of goods or services. These entities, referred to as deductors, need to obtain GSTR-7A as proof that the tax has been deducted and reported accurately.

The following entities are eligible to deduct TDS under GST:

- Government Departments: Any department or establishment of the Central or State government is required to deduct TDS when making payments for supplies of goods or services.

- Local Authorities: This includes municipal corporations and other local governing bodies that fall under the authority of the government.

- Governmental Agencies: These are government-established agencies that conduct various functions on behalf of the state or central government.

- Public Sector Undertakings (PSUs): Companies where the government holds a significant stake (usually 51% or more) are required to deduct TDS under GST on certain payments made to suppliers.

- Authorities and Boards: Any authority or board that has been established by an act of Parliament or State Legislature and is owned or controlled by the government.

- Societies Established by Government: Societies that are registered under the Societies Registration Act, 1860, and are set up by either the Central or State government also need to deduct TDS under GST.

These deductors must obtain GSTR-7A after filing their GSTR-7 return, which reflects the tax they have deducted from their suppliers. The certificate serves as formal documentation that the deductor has fulfilled its legal responsibility under the GST framework.

For any payment that exceeds Rs. 2.5 lakh under a contract, the deductor is required to deduct TDS at the rate of 2% (1% each for CGST and SGST in the case of intrastate supplies, or 2% IGST for interstate supplies). This TDS is then reflected in the GSTR-7A certificate, which both the deductor and the deductee can use for record-keeping and claiming tax credits.

Deadline for Filing GSTR-7

The deadline for filing GSTR-7 is the 10th of the following month. For example, if you have deducted TDS for the month of October, you must file the GSTR-7 return by 10th November. Filing the return on time is important to avoid penalties and ensure that the deductee can claim the TDS amount as Input Tax Credit (ITC) without delays.

Link Between GSTR-7 and GSTR-7A

Once the deductor successfully files Form GSTR-7, the system automatically generates Form GSTR-7A, which is the TDS certificate. This certificate is crucial for both the deductor and the deductee. It confirms that the TDS has been deducted and provides the deductee with the ability to claim the deducted amount as ITC.

In simple terms, GSTR-7 is the form that the deductor files to report TDS, and GSTR-7A is the certificate generated based on that return. Both are essential for maintaining transparency and compliance in the GST system.

Importance of GSTR-7A

Form GSTR-7A plays a crucial role in the GST system as it serves as an official confirmation of the TDS (Tax Deducted at Source) deductions made by the deductor. This certificate is automatically generated after the deductor files Form GSTR-7, and it contains all the essential details regarding the TDS deducted during transactions. The GSTR-7A certificate is an important document for both the deductor and the deductee, ensuring compliance with GST regulations and transparency in tax deductions.

Role of GSTR 7A in Confirming TDS Deductions

The primary role of GSTR-7A is to confirm the TDS deductions made by the deductor. It contains key details such as the amount of tax deducted, the GSTIN of the deductee, the payment value, and the date of deduction. This certificate acts as formal documentation that the TDS deductions have been made and reported correctly, providing a clear record for both parties involved.

How the Deductee Can Use GSTR-7A to Claim Input Tax Credit (ITC)

For the deductee, GSTR-7A is essential because it allows them to claim Input Tax Credit (ITC) for the tax deducted. Once the deductor files GSTR-7 and the GSTR-7A certificate is generated, the TDS details are automatically reflected in the deductee’s tax records. The deductee can then use this certificate to claim ITC, which can be applied to reduce their output tax liability, helping to lower the amount of tax they owe. Without GSTR-7A, the deductee would not have official proof of the TDS deduction, which could delay or hinder their ability to claim this credit.

Availability of GSTR-7A for Both Deductors and Deductees

The GSTR-7A certificate is available to both the deductor and the deductee. Once generated, both parties can view and download the certificate from the GST portal. This ensures that both the deductor has proof of the TDS deducted, and the deductee has the necessary documentation to claim ITC. This dual access fosters transparency and accountability in the tax deduction process, simplifying GST compliance for both sides.

In summary, GSTR-7A is vital for confirming TDS deductions, enabling deductees to claim their ITC, and maintaining a clear and transparent tax deduction record for both deductors and deductees.

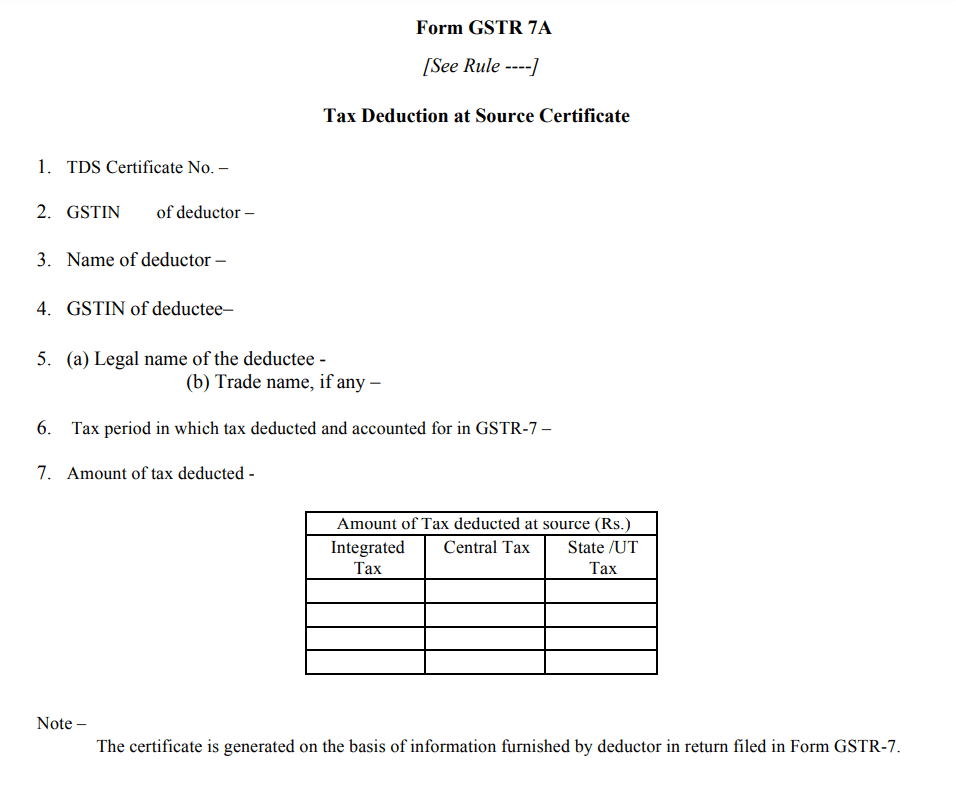

Details Mentioned in GSTR-7A

The GSTR-7A certificate contains all the key information related to the TDS (Tax Deducted at Source) deductions made by the deductor. This certificate is generated automatically after the deductor files Form GSTR-7 and is essential for both the deductor and deductee to maintain accurate tax records. Below is a breakdown of the crucial details included in Form GSTR-7A:

1. TDS Certificate Number

- Each GSTR-7A certificate has a unique TDS Certificate Number that helps identify and track the specific certificate. This number serves as a reference for both the deductor and deductee in case any issues arise related to the TDS deduction.

2. GSTIN of the Deductor

- The GSTIN (Goods and Services Tax Identification Number) of the deductor is mentioned on the certificate. This unique 15-digit number identifies the entity that has deducted the TDS. It helps track and verify the deductor’s GST compliance.

3. Name of the Deductor

- The name of the deductor, which is the person or entity responsible for deducting the TDS, is mentioned on the GSTR-7A certificate. This name ensures proper identification of the deductor who has filed GSTR-7 and deducted TDS during the transaction.

4. GSTIN of Deductee

- The GSTIN (Goods and Services Tax Identification Number) of the deductee is also included in the certificate. This 15-digit unique identifier is assigned to the person or business from whom TDS was deducted, linking the TDS deduction to the correct recipient.

5. Name of the Taxable Person (Deductee)

- The certificate includes the name of the deductee, which is the person or business from whom TDS was deducted during the supply of goods or services. This name ensures that the certificate is linked to the right recipient.

3. Tax Period for Which GSTR-7 is Filed

- The tax period for which the TDS deduction is reported is included in the certificate. This indicates the specific month and year during which the TDS deduction took place, aligning the certificate with the corresponding return period.

6. Payment Value on Which TDS is Deducted

- GSTR-7A also mentions the payment value on which the TDS was deducted. This is the total value of the transaction (goods or services) that was subject to TDS. This helps verify the exact amount on which the tax deduction was applied.

7. Contract and Invoice Details

- The certificate includes contract details and invoice information related to the TDS deduction. This typically includes the invoice number, date, and the contract under which the transaction took place, ensuring that the deduction is clearly linked to a specific transaction.

Each of these details ensures that both the deductor and deductee have a clear and accurate record of the TDS deductions. The information in GSTR-7A is crucial for the deductee to claim their Input Tax Credit (ITC) and for the deductor to demonstrate compliance with GST regulations.

Steps to View and Download GSTR-7A (for Deductors and Deductees)

Both deductors and deductees can view and download the GSTR-7A certificate directly from the GST portal. The process for each is simple and ensures that both parties can maintain proper records of TDS deductions. Below are the steps for deductors and deductees to access their GSTR-7A certificate:

Steps for Deductors:

- Log in to the GST Portal

- Visit the official GST portal at www.gst.gov.in and log in using your credentials (username and password).

- Navigate to ‘Services > User Services > View/Download Certificates’

- After logging in, go to the Services tab on the main menu.

- Select User Services and then click on the View/Download Certificates option.

- Click the ‘TDS Certificate’ Link

- On the certificates page, locate and click the ‘TDS Certificate’ link to proceed.

- Select the Financial Year and Return Filing Period

- A drop-down menu will appear where you can choose the relevant Financial Year and Return Filing Period for which you want to download the certificate.

- Enter GSTIN of the Deductee (Optional)

- You can optionally enter the GSTIN of the deductee to narrow down the certificate for a specific recipient. If you leave this field blank, the system will generate certificates for all deductees for the selected period.

- Click ‘Search’ and Download the TDS Certificate

- After entering the required details, click the Search button. The system will display the relevant certificate(s).

- You can then click the Download link to download the GSTR-7A certificate in PDF format.

Steps for Deductees:

- Log in to the GST Portal

- Deductees must also log in to the GST portal using their credentials (username and password) at www.gst.gov.in.

- Navigate to ‘Services > User Services > View/Download Certificates’

- After logging in, go to the Services tab, click on User Services, and select View/Download Certificates from the options.

- Click the ‘TDS Certificate’ Link

- Click on the ‘TDS Certificate’ link to view the certificates available for you.

- Select the Financial Year and Return Filing Period

- Choose the Financial Year and Return Filing Period for which you want to view the certificate.

- Enter GSTIN of the Deductor (Optional)

- You can optionally enter the GSTIN of the deductor to view the certificate for a specific transaction. If you leave this field blank, it will show the details for all deductors in the selected period.

- Click ‘Search’ and Download the TDS Certificate

- Click the Search button to display the TDS certificate.

- You can then download the certificate in PDF format for your records.

These steps ensure that both deductors and deductees can easily access and download their GSTR-7A certificates, making it convenient to manage tax records and compliance.

Pre-conditions for Generating GSTR-7A

Before a GSTR-7A certificate can be generated, certain conditions must be met by both the deductor and the deductee. These pre-conditions ensure that the TDS process is correctly recorded and validated under the GST system. Below are the key pre-conditions:

1. The Deductor Must File GSTR-7 on the GST Portal

- The deductor (the person or entity responsible for deducting TDS) must first file Form GSTR-7 on the GST portal. This form contains details of the TDS deducted from payments made to suppliers of goods or services.

- Without filing GSTR-7, the system will not be able to generate GSTR-7A, as the certificate relies on the information submitted in GSTR-7.

2. The Deductee Must Accept the Details Filed by the Deductor

- After the deductor files GSTR-7, the deductee (the person or entity from whom TDS is deducted) must accept the details uploaded by the deductor.

- This step is crucial for the deductee to confirm that the correct amount of TDS has been deducted. Only after the deductee accepts the information, the system will generate the GSTR-7A certificate, which is the formal document used by the deductee to claim Input Tax Credit (ITC).

Once these two pre-conditions are fulfilled, the GSTR-7A certificate is automatically generated by the system and can be accessed by both the deductor and deductee. These steps ensure accuracy and compliance with GST regulations, safeguarding both parties involved in the transaction.

Penalties for Non-Filing or Late Filing of GSTR-7A

Filing Form GSTR-7 on time is crucial to ensure that the GSTR-7A certificate is generated. Failure to file GSTR-7 or delayed filing can result in penalties and additional financial costs. Below are the key penalties associated with non-filing or late filing of GSTR-7, which directly impacts the generation of GSTR-7A.

1. Late Fee for Non-Filing of GSTR-7

- If a deductor fails to file Form GSTR-7 by the due date (10th of the following month), a late fee of Rs. 200 per day (Rs. 100 under CGST and Rs. 100 under SGST) is imposed.

- This late fee is capped at a maximum of Rs. 5,000, meaning the total penalty will not exceed this limit regardless of how many days the filing is delayed.

2. Interest for Late Payment of TDS

- Along with the late fee, an interest of 18% per annum is charged on the amount of TDS that was not paid on time.

- The interest is calculated from the due date (the 11th day of the month) until the date the TDS payment is made.

- This additional cost can accumulate quickly if the TDS payment is delayed significantly, increasing the financial burden on the deductor.

3. Consequences of Failing to File GSTR-7

- If GSTR-7 is not filed, the GSTR-7A certificate will not be generated. This impacts both the deductor and the deductee:

The deductor will face compliance issues and penalties.

The deductee will be unable to claim Input Tax Credit (ITC), as they won’t have a valid TDS certificate to support their claim.

- Non-generation of GSTR-7A can lead to complications in the deductee’s tax liabilities, potentially resulting in disputes or delays in credit claims.

In summary, filing GSTR-7 on time is essential not just to avoid financial penalties but also to ensure that the deductee receives their GSTR-7A certificate, which is necessary for claiming ITC.

Can GSTR-7A Be Revised?

Once GSTR-7A is generated, it cannot be revised. This means that any errors or omissions in the TDS details reflected in GSTR-7A cannot be corrected directly in the certificate itself.

How to Correct Errors or Omissions

If there are mistakes in the TDS details provided in the initial GSTR-7 filing, the deductor cannot amend them in the already generated GSTR-7A certificate. However, there is a way to correct these errors in subsequent filings:

- The deductor can make necessary corrections to the TDS details in the next GSTR-7 return for the following month.

- These corrections will then reflect in the next cycle and a revised GSTR-7A certificate will be generated with the updated information.

While this ensures that errors can be fixed, it emphasizes the importance of carefully reviewing the details in the original GSTR-7 filing to avoid discrepancies.

How to Download Multiple GSTR-7A Certificates

If a deductor has deducted TDS from multiple suppliers or deductees during a specific period, multiple GSTR-7A certificates will be generated—one for each GSTIN (Goods and Services Tax Identification Number) of the deductee.

Downloading Multiple GSTR-7A Certificates :

When more than one TDS certificate is available, the GST system does not provide a bulk download option. Therefore, each GSTR-7A certificate must be downloaded individually for every deductee.

To download multiple GSTR-7A certificates, follow these steps for each deductee:

- Log in to the GST Portal using your credentials.

- Navigate to ‘Services > User Services > View/Download Certificates.’

- Click the ‘TDS Certificate’ Link to open the list of available certificates.

- Select the Financial Year and Return Filing Period, as required.

- Enter the GSTIN of the Deductee (optional but useful for narrowing down certificates).

- Click ‘Search,’ and the TDS certificate for that specific deductee will be displayed.

- Download the Certificate in PDF format.

Repeat this process for each deductee to download all the GSTR-7A certificates you need. Although this process is manual, it ensures that every deductee’s certificate is properly accessed and saved.

Conclusion

In summary, GSTR-7A is an essential document under the GST system, serving as the TDS (Tax Deducted at Source) certificate that confirms the deductions made by the deductor and reported through Form GSTR-7. It is automatically generated by the GST system and is crucial for the deductee, as it enables them to claim Input Tax Credit (ITC) on the TDS amount.

Timely filing of GSTR-7 is vital, as failure to file or delay in filing can result in penalties and interest, and prevent the generation of GSTR-7A. This not only affects the deductor but also impacts the deductee’s ability to claim ITC.

Both deductors and deductees should download and keep a copy of the GSTR-7A certificate for future reference, as it is a key piece of documentation that ensures smooth tax compliance and accurate credit claims under the GST system. Proper handling of this document helps avoid complications and ensures that the tax deduction process is transparent and efficient.

FAQs About GSTR-7A

Here are some of the most frequently asked questions regarding GSTR-7A, the TDS certificate under GST, to help clarify its purpose and usage:

1. What is GSTR-7A?

GSTR-7A is a system-generated TDS (Tax Deducted at Source) certificate issued to the deductor and deductee once Form GSTR-7 has been filed by the deductor. It confirms that the TDS has been deducted and reported correctly. The deductee can use this certificate to claim Input Tax Credit (ITC) on the deducted amount.

2. How to Download GSTR-7A from the GST Portal?

To download GSTR-7A, both deductors and deductees can log in to the GST portal and follow these steps:

- Navigate to Services > User Services > View/Download Certificates.

- Click on the ‘TDS Certificate’ link.

- Select the financial year and return filing period.

- Enter the GSTIN of the deductee (optional).

- Click ‘Search’ and download the TDS certificate in PDF format.

3. Do Multiple Certificates Need to Be Downloaded Separately?

Yes, if multiple TDS certificates are available for different deductees, each certificate must be downloaded individually. The GST system does not allow bulk downloads, so you will need to repeat the process for each GSTIN.

4. Is It Mandatory for Deductors to File GSTR-7A?

No, deductors do not need to file GSTR-7A. This certificate is automatically generated by the GST system once the deductor files Form GSTR-7. The responsibility of the deductor is to file GSTR-7 accurately and on time.

5. Can Deductors or Deductees Download and Keep a Copy of the TDS Certificate for Future Reference?

Yes, both deductors and deductees can download and keep a copy of their GSTR-7A certificate from the GST portal for future reference. It is advisable to retain this document as it serves as proof of TDS deduction and is necessary for the deductee to claim Input Tax Credit (ITC).

These FAQs address common queries related to GSTR-7A, helping ensure both deductors and deductees are well-informed about the process and its significance.

Related Posts:

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Everything to know about GSTR 11:Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQs

Everything to know about GSTR 11:Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

GSTR 10: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 10: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance