Key Takeaways:

Mandatory for Turnover Above ₹5 Crores: GSTR-9C is required for businesses with an annual turnover exceeding ₹5 Crores. It ensures proper reconciliation between GST returns and audited financial statements.

Avoid Penalties with Timely Filing: Delays in filing GSTR-9C can lead to penalties of ₹200 per day and interest on unpaid taxes.

Accuracy is Critical: Incorrect filings can result in ITC blockages, reversals, and possible legal repercussions. Precise reconciliation is essential to avoid these issues.

Self-Certification Instead of Audit Certification: For businesses with an annual turnover below ₹5 crores, self-certification is allowed for GSTR-9C. However, for businesses with a turnover exceeding ₹5 crores, CA certification is mandatory.

Compliance Brings Benefits: Timely and accurate filing of GSTR-9C helps businesses avoid penalties, ensures smooth ITC claims, and promotes compliance with GST regulations, reducing the risk of scrutiny or audits.

GSTR-9C is a special form that acts as a reconciliation statement between your company’s financial records and the annual GST returns you’ve already filed. In simple terms, it ensures that the numbers in your audited financial statements align with the figures reported in your GST returns for the year.

Previously, this form was prepared and certified by a Chartered Accountant (CA) or a Cost Accountant. However, businesses with an annual turnover below ₹5 crores can now self-certify the GSTR-9C form. For businesses with turnover exceeding ₹5 crores, CA certification is mandatory, and self-certification is not applicable. This change simplifies the compliance process while maintaining the integrity of the reconciliation.

GSTR-9C is crucial because it identifies and rectifies any differences or mismatches between the returns filed and the actual financials. It ensures that the tax paid, turnover, and input tax credits claimed are accurate. This helps maintain transparency and reduces the likelihood of errors or fraud.

However, not every business needs to file GSTR-9C. Filing this form is mandatory only if your annual turnover exceeds ₹5 crore in a financial year. So, if your business crosses this threshold, GSTR-9C becomes a legal requirement.

Who Needs to File GSTR 9C?

GSTR-9C is required for businesses with an annual turnover exceeding ₹5 crore from FY 2020-21 onwards.

Entities Involved:

The filing of GSTR 9C applies to various types of businesses registered under GST, such as:

- Public and Private Limited Companies: Large or small-scale companies involved in selling goods or services.

- LLPs (Limited Liability Partnerships): Registered partnerships where the liability of the partners is limited.

- Sole Proprietorships and Other Taxable Entities: Individuals or entities that are registered for GST and conduct business activities.

Exceptions:

There are a few categories of businesses that do not need to file GSTR 9C, even if they are registered under GST. These include:

- Taxpayers under the Composition Scheme: Small businesses that have opted for the GST Composition Scheme.

- Casual Taxable Persons: Those who occasionally supply goods or services but don’t have a fixed place of business.

- Input Service Distributors: Entities that only distribute input tax credit and don’t engage in regular sales or services.

Difference between GSTR 9, 9A, 9B, 9C

- GSTR-9: Annual return for regular taxpayers under GST. It provides a summary of outward and inward supplies, taxes paid, and input tax credits claimed during the year.

- GSTR-9A: Annual return for taxpayers under the Composition Scheme. It summarizes quarterly GSTR-4 filings, showing turnover, taxes, and inward/outward supplies for the year.

- GSTR-9B: Annual return specifically for e-commerce operators collecting Tax Collected at Source (TCS). It consolidates data from GSTR-8 filings, detailing supplies through the platform and TCS collected.

- GSTR-9C: Reconciliation statement required for taxpayers with annual turnover above ₹5 crore, to ensure data accuracy between GSTR-9 and audited financial statements.

Components of GSTR 9C

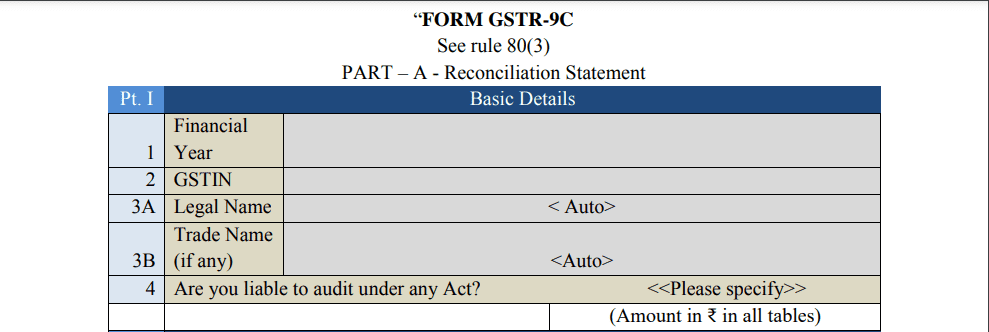

Part I: Basic Details

This section captures the fundamental information about the business, which includes:

- GSTIN: The Goods and Services Tax Identification Number of the business.

- Legal Name and Trade Name: The registered name and the trade name (if any) of the business.

- Financial Year: The financial year for which the GSTR 9C form is being filed.

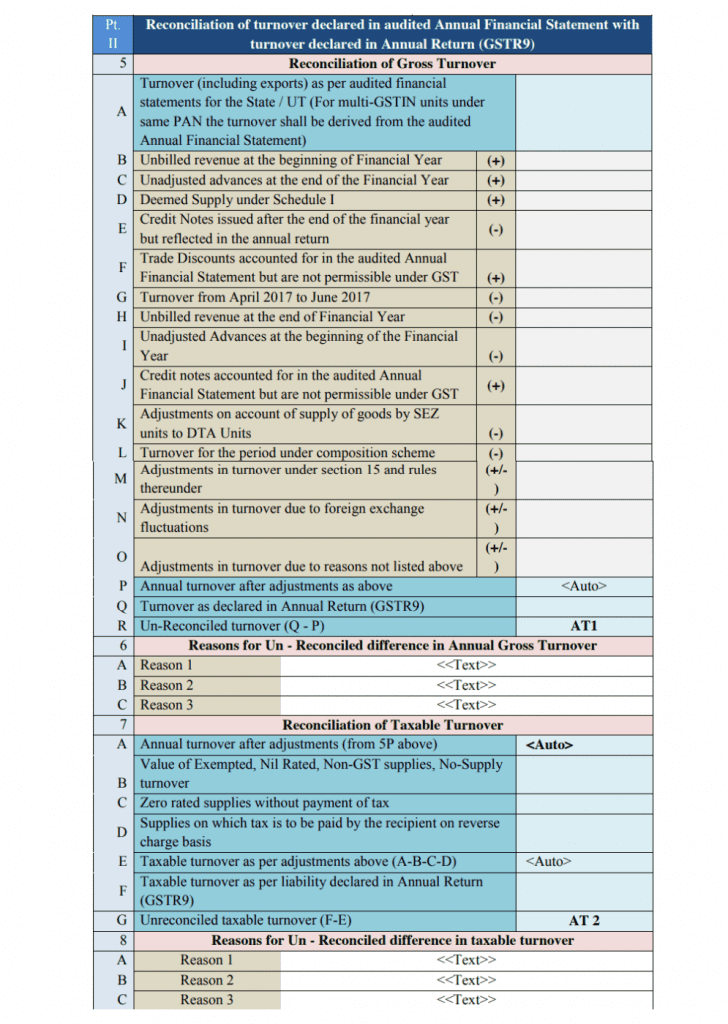

Part II: Reconciliation of Turnover

In this section, businesses need to reconcile the total turnover reported in their audited financial statements with the turnover declared in their annual GST returns (GSTR 9). It includes:

- Total Turnover: The complete turnover generated by the business during the financial year, including taxable, non-taxable, and exempt supplies.

- Taxable Turnover: The part of the turnover that is subject to GST.

- Non-Taxable Turnover: The portion of turnover not subject to GST, including exempt supplies or exports.

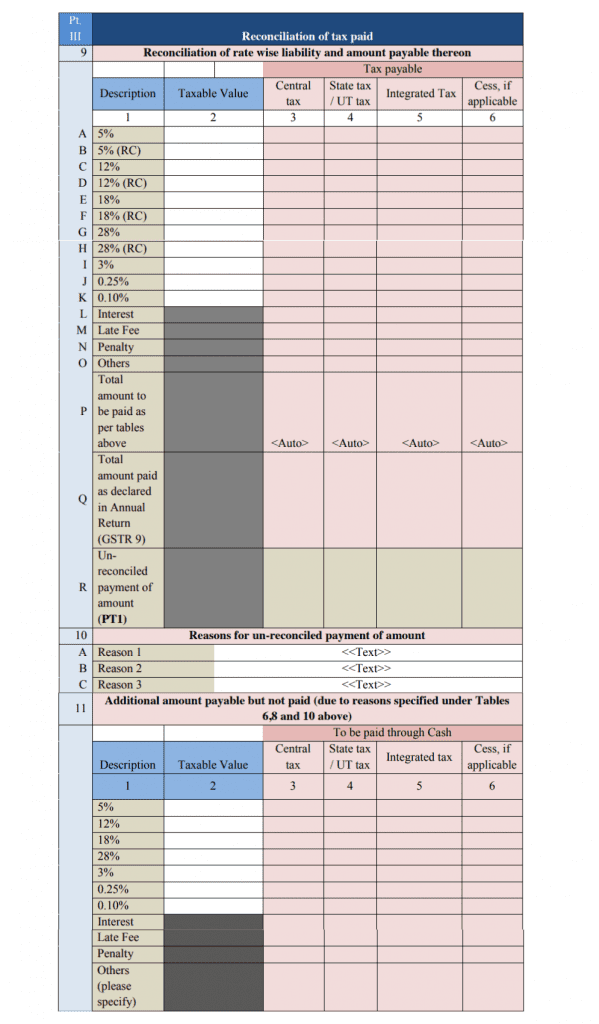

Part III: Reconciliation of Tax Paid

Here, businesses must reconcile the tax liability declared in GSTR 9 with the actual taxes paid during the financial year. This ensures that:

- Declared Taxes vs. Paid Taxes: The taxes you’ve declared match the actual payments made under GST.

- Any underpayments or overpayments are identified and resolved.

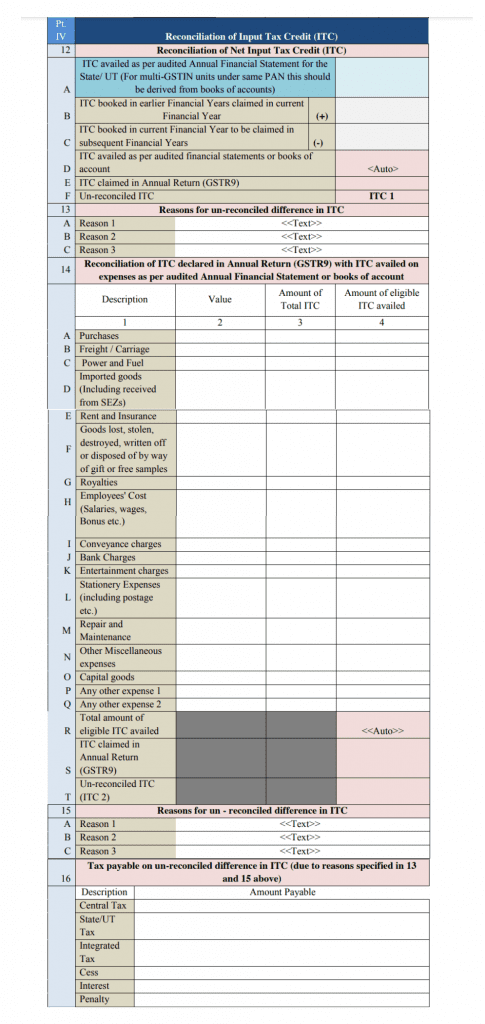

Part IV: ITC Reconciliation

This section focuses on reconciling the Input Tax Credit (ITC) claimed by the business with the actual eligible ITC. ITC is the tax a business can claim back on purchases made for running the business. The reconciliation ensures:

- Claimed ITC vs. Eligible ITC: Any difference between what the business claimed as ITC and what is allowed as per the GST law is highlighted.

Part V: Auditor’s Recommendations

Auditor’s suggestion regarding the additional liability arising from non-reconciliation.

Documents Required for Filing GSTR 9C

To ensure smooth and accurate filing of GSTR 9C, businesses need to have the following documents ready:

1. Financial Statements

- Audited Balance Sheet: A summary of the company’s financial position, showing its assets, liabilities, and equity at the end of the financial year.

- Profit & Loss Statement: A detailed report of the company’s revenues, expenses, and profits/losses during the financial year.

- Cash Flow Statement: A statement that shows how cash is moving in and out of the business through its operating, investing, and financing activities.

These statements are critical because they provide the baseline for reconciling the turnover, taxes, and credits reported in the GST returns with the actual financial performance of the business.

2. Tax Records

- GSTR 9 Form: The annual return form filed under GST, summarizing all the GST returns filed throughout the year. This document acts as a key reference for preparing GSTR 9C.

- All Filed Returns for the Financial Year: This includes monthly or quarterly returns such as GSTR 1 (sales return) and GSTR 3B (summary of sales and tax liability). These returns are used to cross-check the tax payments made against the tax liability declared.

3. Invoice-Level Data

- Sales and Purchase Invoices: Detailed data of all sales and purchase transactions for the year. These invoices are used to reconcile turnover, taxable value, and input tax credits (ITC) claimed by the business.

- Reconciliation of Invoices: A comparison of the invoices recorded in your financial statements versus those filed in the GST returns. This helps identify any mismatches or discrepancies.

4. Other Relevant Documents

- Documents Used for Reconciliation or Audit Adjustments: Any additional records that were used to make adjustments during the audit process, such as credit notes, debit notes, or documents explaining why certain transactions were adjusted. These are crucial to explain any differences that may arise during reconciliation.

Having these documents organized and ready will simplify the GSTR 9C filing process, reduce the chances of errors, and help ensure that the business remains compliant with GST regulations.

Step-by-Step Guide on Filing GSTR 9C

A. Prerequisites for Filing GSTR-9C

Before proceeding to file Form GSTR-9C, make sure the following conditions are met:

- The taxpayer must be registered under GST with a valid GSTIN.

- The taxpayer must have successfully filed Form GSTR-9 (the Annual Return) for the relevant financial year.

- The business should have a turnover exceeding Rs. 5 crore in the previous financial year.

- Login credentials for the GST portal must be valid and active.

B. Steps to Generate the GSTR-9C JSON File

To begin, you need to generate the JSON file for GSTR-9C using the offline utility. Here’s how:

Step 1: Download the Necessary Forms

- Log in to the GST portal using your credentials.

- Download Form GSTR-9 for the relevant financial year.

- Similarly, download the tables from GSTR-9, which will be used to generate the GSTR-9C.

Step 2: Download the GSTR-9C Offline Tool

- Visit the Downloads section on the GST portal and select “Offline Tools”.

- Download the “GSTR-9C Offline Tool”.

Step 3: Prepare the Data Using the Offline Tool

- Open the GSTR-9C Offline Utility and enter the required data into the designated tables.

- After filling in the necessary details, you can preview the draft version of GSTR-9C by generating the PDF.

Step 4: Generate the JSON File

- Once you’ve reviewed the draft, generate the final JSON file. This file will be used for uploading on the GST portal.

C. Uploading the GSTR-9C JSON File to the GST Portal

Now that you have the JSON file, follow these steps to upload it:

Step 1: Log in to the GST Portal

- Use your credentials to log in to the GST portal.

Step 2: Prepare for Upload

- Navigate to the ‘Returns’ tab and select “Annual Return”.

- Choose the appropriate financial year and click ‘Search’.

Step 3: Upload the JSON File

- Select “Prepare Offline” and click the “Upload” button to submit the JSON file.

Step 4: Review and Edit (if necessary)

- After uploading, you can make any necessary changes to the form. If changes are made, you must regenerate and upload the JSON file again.

Step 5: Resolve Errors (if any)

- If you encounter any errors during upload, download the Error Report, correct the errors, and re-upload the updated JSON file.

D. Final Steps for Filing GSTR-9C on the GST Portal

Once the JSON file is successfully uploaded, complete the filing process by following these steps:

Step 1: Upload Supporting Documents

- You will need to upload supporting financial documents, such as the balance sheet and profit & loss statement. These must be in PDF format, with a maximum file size of 5 MB per file. You can upload a maximum of 2 files per section.

Step 2: Save Uploaded Documents

- Ensure you click the “SAVE” button after uploading each document. Failing to do so will result in an error when you proceed to file the return.

Step 3: Preview the GSTR-9C Draft

- You can view the draft version of Form GSTR-9C by clicking the “PREVIEW DRAFT GSTR-9C” button.

Step 4: Proceed to File

- Once all documents are uploaded and saved, the “PROCEED TO FILE” button will be enabled. Click this to proceed to the final verification page.

Step 5: Final Verification and Filing

- On the verification page, confirm the details. Once verified, the “FILE GSTR-9C” button will appear, allowing you to submit the form.

Step 6: Track Your Filing

- After successful submission, you can track the status of your GSTR-9C by navigating to the “Services” tab, selecting “Returns”, and then “View Filed Returns”.

Important Note on Certification

For businesses with an annual turnover exceeding Rs. 5 crore, CA certification is mandatory for GSTR-9C. Self-certification is not applicable in such cases.

Businesses with turnover below Rs. 5 crore may proceed with self-certification, but certification from a CA or CMA is still advisable for extra assurance.

Penalties and Legal Repercussions for Incorrect Filing

1. Standard Filing Date:

The deadline for filing GSTR 9C is generally 31st December following the end of the financial year. For example, if you are filing for the financial year 2022-23, the due date for GSTR 9C would be 31st December 2023. It’s important to file on time to avoid penalties and maintain compliance with GST laws.

2. Penalties for Non-Compliance:

If GSTR 9C is not filed by the due date, the business will be subject to penalties. The penalty for late filing is ₹200 per day, which is broken down into:

- ₹100 per day for CGST (Central GST).

- ₹100 per day for SGST (State GST).

The penalty continues to accumulate every day until the return is filed, and there is no maximum limit on the total penalty amount, meaning it can add up significantly over time. Additionally, interest at the rate of 18% per annum may be charged on any unpaid tax liability from the due date until the actual date of payment.

These penalties are imposed to ensure that businesses file their GSTR 9C on time and maintain proper tax compliance.

3. Financial Penalties:

Filing GSTR 9C with incorrect information, whether due to misreporting or failure to properly reconcile your returns, can result in substantial financial penalties. If discrepancies are found during an audit or inspection, the following penalties may apply:

- General Penalty: If there is a mismatch between the filed returns and actual financial data, businesses may be subject to fines under Section 122 of the CGST Act, which can range from ₹10,000 or 10% of the tax due (whichever is higher).

- ITC Reversal Penalties: If incorrect Input Tax Credit (ITC) claims are identified, businesses may be required to reverse the ITC and pay an additional interest of 18% per annum from the due date of filing.

These penalties emphasize the importance of ensuring accurate reconciliation and filing of GSTR 9C to avoid financial liabilities.

4. Legal Action:

In addition to financial penalties, there are legal consequences for intentionally misfiling or submitting false information under the GST law:

- Prosecution for Fraud: If a business is found guilty of willfully providing false information or committing fraud, it may face prosecution under Section 132 of the CGST Act. This can lead to imprisonment for a term ranging from six months to five years, depending on the amount of tax evaded.

- Seizure of Property: In cases of significant non-compliance or tax evasion, the authorities can initiate proceedings to seize property or assets of the business.

- Cancellation of GST Registration: Repeated instances of incorrect filing or non-compliance may lead to the cancellation of GST registration, effectively stopping the business from legally conducting its operations.

These legal repercussions highlight the need for businesses to file GSTR 9C accurately and on time, as the consequences of non-compliance can be severe, both financially and legally.

Common Mistakes to Avoid

When filing GSTR 9C, accuracy is crucial to avoid penalties and ensure compliance. Here are some common mistakes businesses should avoid:

1. Errors in ITC Reconciliation

- Misreporting Input Tax Credits (ITC) is one of the most frequent mistakes made by businesses. Often, businesses claim ITC based on invoices without properly reconciling it with the actual eligible ITC. This can lead to over-claiming or under-claiming, which results in penalties.

- Tip: Always cross-check ITC claims with your purchase invoices and ensure that the credit claimed is actually eligible under GST laws.

2. Mismatch in Turnover Data

- Inconsistencies between the turnover declared in GSTR 9 and the turnover reported in your audited financial statements are another common issue. This could happen due to unaccounted sales, adjustments, or errors in calculation, leading to discrepancies during reconciliation.

- Tip: Ensure that the turnover figures in both your financial records and GST returns are aligned. Review all adjustments made during the year and properly account for them.

3. Incorrect Filing of Adjustments

- Misstating or omitting adjustments made during the audit process can result in discrepancies. Adjustments, such as rectifying tax liabilities or ITC claims, should be accurately reflected in GSTR 9C. Failing to report these adjustments correctly can lead to misreporting.

- Tip: Keep track of all audit adjustments made during the reconciliation process and ensure they are clearly reflected in the relevant sections of GSTR 9C.

By avoiding these common mistakes, businesses can ensure that their GSTR 9C filing is accurate and compliant, reducing the risk of penalties and further scrutiny from tax authorities.

How to Handle Discrepancies in GSTR 9C

Discrepancies in GSTR 9C can arise during the reconciliation of GST returns and audited financial statements. Here’s how to identify, rectify, and manage such discrepancies:

1. Identifying Discrepancies

Discrepancies can often occur due to the following reasons:

- Turnover Mismatches: Differences between the turnover reported in GSTR 9 and the actual turnover in your audited financial statements. This could be due to omitted sales, incorrect invoice data, or adjustments not recorded properly.

- Tax Payment Variations: Sometimes, the taxes declared in the GST returns may differ from the actual taxes paid. This may happen due to late payment of taxes, incorrect tax rates applied, or calculation errors.

- ITC Mismatch: Differences in the claimed Input Tax Credit (ITC) versus the eligible ITC in your audited records. This usually happens when ITC is claimed on ineligible purchases or if certain invoices are missing during reconciliation.

2. Rectification Process

To correct discrepancies found during the reconciliation process, businesses should take the following steps:

- Amendments in GSTR 9: You can make corrections to your annual return (GSTR 9) to address the discrepancies. For instance, if there are mismatches in turnover or taxes, they can be corrected by revising the figures in GSTR 9. This can be done before finalizing GSTR 9C.

- Filing Revised Returns: If the errors are significant, you may need to file revised returns for the periods in question. Correcting the underlying GSTR 1 (sales) or GSTR 3B (tax payments) returns can help align your financial records and GST returns.

- Documenting Adjustments: Ensure that all audit adjustments, corrections, and rectifications are documented clearly. This will help justify the corrections made in case of any further queries from the authorities.

3. Impact of Discrepancies on ITC Claims

Discrepancies in GSTR 9C can directly impact your Input Tax Credit (ITC) claims. Here’s how:

- ITC Reversal: If discrepancies reveal that you have claimed excess ITC (more than you were eligible for), you will have to reverse the excess ITC. Additionally, you may be required to pay interest on the excess ITC claimed.

- Reduction in Eligible ITC: Errors or discrepancies can reduce the amount of eligible ITC available to you, impacting your overall tax liability. This might lead to a higher tax payable in subsequent filings.

- Delayed Refunds: If ITC discrepancies are not resolved, it may delay any GST refunds that you are expecting, especially if the errors are related to export supplies or zero-rated transactions.

By identifying discrepancies early, taking corrective actions, and ensuring your ITC claims are accurately reconciled, businesses can avoid potential penalties and ensure compliance with GST regulations.

Reconciliation Techniques for GSTR 9C

Accurate reconciliation is critical when filing GSTR 9C to ensure that your financial statements Filing the GSTR-9C form is crucial for businesses with an annual turnover exceeding ₹5 crores, as it requires mandatory certification by a Chartered Accountant (CA).

It promotes transparency, accuracy, and compliance with GST regulations, and failing to file it—or submitting inaccurate information—can lead to financial penalties, ITC reversals, or even legal consequences. Here are some effective techniques to reconcile the key components:

1. Matching Turnover

To reconcile the turnover between your financial statements and GST returns, follow these steps:

- Cross-check with GSTR 1: The first step is to match the sales turnover reported in GSTR 1 (sales return) with your audited financial statements. Ensure that all sales invoices for taxable and non-taxable supplies, including exports and exempted supplies, are accurately recorded.

- Reconcile with GSTR 3B: Verify that the total turnover reported in GSTR 3B (summary return) aligns with both GSTR 1 and your audited financials. This ensures consistency across all returns.

- Consider Adjustments: If there are any adjustments made during the financial year (such as credit notes, sales returns, or discounts), ensure these are properly accounted for in both the GST returns and financial records.

- Tip: Use a detailed invoice-level reconciliation to identify any mismatches between the sales figures reported under GST and in your accounts.

2. Matching ITC Claims

Accurate reconciliation of Input Tax Credit (ITC) is essential to avoid over-claiming or under-claiming credits. Here’s how you can ensure accuracy:

- Compare with Purchase Register: Match the ITC claimed in GSTR 3B with your purchase register and ensure all eligible purchases and expenses are accounted for. Ensure that all vendor invoices are included and verify that ITC is only claimed on eligible inputs.

- Verify with GSTR 2A/2B: GSTR 2A/2B is an auto-populated form that reflects the ITC available to you based on the suppliers’ filed returns. Cross-check ITC in GSTR 3B with GSTR 2A/2B to ensure that the credits claimed match the suppliers’ declarations.

- Address Mismatches: If there are any discrepancies between GSTR 3B and GSTR 2A/2B, follow up with the supplier to ensure they have filed their returns correctly. Any unmatched ITC should be excluded from the claims to avoid penalties.

3. Adjusting for Tax Paid

Reconciling the tax liability declared in the GST returns with the actual taxes paid is crucial for GSTR 9C. Here’s how to do it:

- Compare Declared Liability in GSTR 3B: Start by verifying the tax liability declared in GSTR 3B for each month or quarter against the tax paid as per the financial records. Ensure that the total tax paid during the year matches the liability reported in the returns.

- Check Payment History: Review the actual tax payments made through the GST portal. Compare the payment challans with the declared tax liability to ensure they are consistent.

- Adjust for Late Payments or Errors: If any taxes were paid late or any errors were corrected in subsequent returns, ensure these adjustments are reflected in the reconciliation process. You may need to account for interest paid on late tax payments as well.

By using these reconciliation techniques, businesses can ensure that their GSTR 9C form is accurate and consistent with both their financial records and GST returns, reducing the risk of discrepancies and potential penalties.

Audit Certification for GSTR 9C

1. Role of the Auditor

The Role of Chartered Accountant (CA) in GSTR-9C:

- Verification of Records: The CA reviews and verifies the company’s financial statements, GST returns (GSTR-9), and supporting documents like invoices, purchase registers, and tax payment records. The goal is to ensure that the information provided in GSTR-9C accurately reflects the company’s actual financial performance and GST compliance.

- Reconciliation: The CA reconciles the data in the audited financials with the returns filed under GST to ensure there are no discrepancies in turnover, tax liability, or Input Tax Credit (ITC) claims.

- Certifying Accuracy: After thorough verification, the CA certifies the GSTR-9C form, confirming that the figures are correct and that the form complies with GST regulations. Previously, this form was prepared and certified by a Chartered Accountant (CA) or a Cost Accountant. However, businesses with an annual turnover below ₹5 crores can now self-certify the GSTR-9C form. For businesses with turnover exceeding ₹5 crores, CA certification is mandatory, and self-certification is not applicable.

2. Audit Observations

While CA certification is mandatory for businesses with an annual turnover exceeding ₹5 crores, businesses below this threshold may still choose to attach a CA-certified document for additional assurance, even though self-certification is permitted. During the audit process, if a Chartered Accountant (CA) is involved, they may raise various observations regarding discrepancies or inconsistencies in the business’s GST filings. These observations could include:

- Discrepancies in Turnover: The CA may identify differences between the turnover declared in the GST returns and the audited financial statements. This could result from omitted sales, incorrect invoice entries, or adjustments not recorded properly.

- Mismatch in ITC Claims: The CA might highlight any over-claimed or under-claimed Input Tax Credit (ITC). This could occur if the ITC claimed in the GST returns does not align with the purchase invoices or the data in GSTR-2A/2B.

- Incorrect Tax Payments: If there is a shortfall or excess in the taxes paid compared to the tax liability declared in the returns, the CA will point this out and suggest corrective action.

- Unreported Adjustments: The CA may observe missing or unreported adjustments, such as credit notes, debit notes, or any changes made during the year that were not reflected in the GST returns.

These audit observations are useful in identifying and addressing errors before filing the final GSTR-9C, ensuring that the reconciliation between financial statements and GST returns is accurate and compliant.

3. Impact of Auditor’s Certification

If a Chartered Accountant (CA) document is attached to the GSTR-9C filing, their certification and observations can have significant implications for the filing and compliance process:

- Ensures Accuracy and Transparency: The CA’s certification provides an added layer of assurance that the data reported in GSTR-9C is accurate. This reduces the risk of scrutiny, audits, or penalties from GST authorities, reinforcing transparency in the business’s financial reporting.

- Requirement for Corrections: If the CA identifies discrepancies or issues in the GST filings, the business may need to file amended returns to address these concerns. Ignoring the CA’s observations or failing to correct identified issues could lead to penalties or additional investigations by the tax authorities.

- Legal and Financial Implications: The CA’s certification carries legal weight. If the CA certifies inaccurate information or overlooks significant errors, both the business and the CA could be held liable for penalties. Therefore, the CA’s observations and recommendations should be taken seriously to ensure full compliance with GST regulations and to mitigate potential legal and financial risks.

By relying on the CA’s expertise, businesses can maintain accuracy, transparency, and compliance in their GST filings. The auditor’s certification plays a vital role in safeguarding the business from potential penalties and legal complications.

Challenges Faced During GSTR 9C Filing

1. Complexity of Reconciliation

One of the biggest challenges businesses face while filing GSTR 9C is the complexity of reconciling different financial components:

- Turnover Reconciliation: Matching the turnover in financial statements with the turnover reported in GSTR 9 can be difficult, especially when there are multiple adjustments like sales returns, credit notes, and exempt supplies.

- ITC Reconciliation: Accurately reconciling Input Tax Credit (ITC) claimed versus eligible ITC can be tricky, particularly if invoices are missing, mismatched, or if vendors have not filed their GST returns correctly.

- Tax Liability Reconciliation: Ensuring the taxes declared in GSTR 9 match the actual taxes paid throughout the year involves careful tracking of all payments made, late fees, and interest charges, which can often lead to discrepancies.

- Turnover Reconciliation: Matching the turnover in financial statements with the turnover reported in GSTR 9 can be difficult, especially when there are multiple adjustments like sales returns, credit notes, and exempt supplies.

- ITC Reconciliation: Accurately reconciling Input Tax Credit (ITC) claimed versus eligible ITC can be tricky, particularly if invoices are missing, mismatched, or if vendors have not filed their GST returns correctly.

- Tax Liability Reconciliation: Ensuring the taxes declared in GSTR 9 match the actual taxes paid throughout the year involves careful tracking of all payments made, late fees, and interest charges, which can often lead to discrepancies.

2. Documentation Gaps

Filing GSTR 9C requires extensive documentation, and businesses often face challenges due to:

- Missing Invoices: Incomplete or missing invoices for purchases or sales can make it difficult to reconcile turnover and ITC.

- Financial Discrepancies: Inconsistencies between the data recorded in the financial statements and the data reported in GST returns may arise due to human error, leading to incorrect filing.

- Lack of Proper Record-Keeping: Many businesses struggle with maintaining organized and up-to-date records, which are necessary for accurate reconciliation.

3. Technology and Portal Glitches

The GST portal is the online platform where all returns and forms are filed, but users often face:

- Portal Downtime: Frequent issues with the portal being down during peak filing times can delay the submission process.

- Technical Glitches: Errors while uploading data, slow processing, or incorrect generation of GSTR forms are common problems encountered on the GST portal.

- Digital Signature Issues: Some users face difficulties with digital signature certificates (DSC), especially during final submission, which can further delay the filing process.

Impact of Filing Errors on Input Tax Credit (ITC)

1. ITC Blockage

Filing errors in GSTR 9C can have a direct impact on your Input Tax Credit (ITC) claims. If the information in GSTR 9C, particularly related to turnover or purchases, doesn’t match the details in GSTR 2A/2B or the filed returns, it can lead to ITC blockage. This means:

- Claiming Ineligible ITC: Mistakes in reporting may result in claiming ineligible ITC, which can later be blocked by the authorities, leading to higher tax liabilities.

- ITC Verification Delays: If discrepancies arise due to errors in filing, the GST authorities may initiate further scrutiny, delaying the verification and approval of your ITC claims.

- Effect: This blockage may result in the business being unable to utilize ITC for future tax payments, leading to increased cash outflows.

2. ITC Reversal

In certain cases, businesses may be required to reverse ITC if discrepancies are discovered. ITC reversal may occur in the following situations:

- Excess ITC Claimed: If, after filing GSTR 9C, it is found that the business has claimed more ITC than eligible, the excess amount must be reversed, and the business will need to pay the corresponding tax along with 18% interest from the date of claim.

- Supplier Non-Compliance: If your supplier has not filed their returns or has not reported your purchase correctly, this may result in ITC being reversed. In such cases, the buyer is held responsible for reversing the ITC claimed.

- Effect: Reversal of ITC can affect cash flow, as the business would need to pay additional tax or lose the ITC benefit until the issue is resolved.

Conclusion

Timely and accurate filing of GSTR-9C not only helps avoid penalties but also builds trust with tax authorities, reducing the likelihood of unnecessary scrutiny or audits. By staying compliant and ensuring all reconciliations—such as turnover, tax paid, and ITC—are properly completed, businesses can safeguard their financial health and maintain a seamless tax reporting process.

Related Posts:

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Master GST Reconciliation: Process, Tools, and Best Practices

Master GST Reconciliation: Process, Tools, and Best Practices

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses