Key Takeaway

What is IFF?: The Invoice Furnishing Facility (IFF) allows businesses under the QRMP Scheme to report sales for the first two months of a quarter, helping buyers claim ITC promptly.

Eligibility & Benefits: IFF is optional for businesses with a turnover of up to ₹5 crore. It enables timely ITC claims and reduces compliance stress.

How It Works: Businesses report B2B invoices in M1 and M2, which are reflected in the recipient’s GSTR-2A/2B, ensuring faster ITC claims.

Due Dates: IFF must be filed by the 13th of the following month for M1 and M2. Late filing can cause ITC delays but has no penalties.

No Penalties for Non-Filing: Missing the deadline doesn’t incur a penalty, but it delays ITC and can affect business relationships.

Strategic Advantage: Using IFF simplifies compliance, improves cash flow, and builds trust with buyers.

For many small businesses, managing GST compliance can be challenging. Monthly return filing and ensuring buyers can claim Input Tax Credit (ITC) on time often result in delays, errors, and strained relationships.

To address these challenges, the government introduced the Invoice Furnishing Facility (IFF) under the Quarterly Return Monthly Payment (QRMP) Scheme.

The IFF enables businesses to report their outward supplies (sales invoices) for the first two months of a quarter without filing the complete GSTR-1 form. This optional feature reduces compliance stress, allows buyers to claim ITC promptly, and improves cash flow for all parties involved. In this article, we will discuss the IFF, its importance, and how businesses can utilize it effectively

Overview of the Invoice Furnishing Facility (IFF)

A. What is the QRMP Scheme?

The Quarterly Return Monthly Payment (QRMP) Scheme was introduced to simplify GST compliance for small taxpayers with an annual turnover of up to ₹5 crore. Under this scheme, businesses are required to:

- File GSTR-1 (sales details) and GSTR-3B (summary of sales, purchases, and tax payable) on a quarterly basis.

- Pay GST liabilities monthly.

This reduces the filing frequency from 12 times a year to just 4, making it particularly beneficial for small and medium enterprises (SMEs).

B. Challenges for Buyers under the QRMP Scheme

While the QRMP Scheme has streamlined filing for businesses, it created a challenge for their buyers. Buyers rely on Input Tax Credit (ITC) to reduce their tax liabilities, but due to the quarterly filing of GSTR-1 by suppliers, buyers had to wait up to three months to claim ITC. This delay impacted cash flow throughout the supply chain.

C. Introducing the Invoice Furnishing Facility (IFF)

To address these challenges, the Invoice Furnishing Facility (IFF) was introduced under the QRMP Scheme. The IFF is an optional feature that allows businesses to report their outward supplies (sales invoices) for the first two months of a quarter, without filing the complete GSTR-1 form. This timely reporting enables buyers to claim ITC promptly, improving cash flow and reducing delays.

How does the Invoice Furnishing Facility (IFF) Work?

The IFF simplifies the compliance process by offering the following key features:

- Months Covered: The IFF is available for the first two months (M1 and M2) of each quarter. For the third month (M3), businesses must file the complete GSTR-1, covering all outward supplies for the quarter.

- Optional Filing: Unlike GSTR-1, which is mandatory, filing through the IFF is entirely optional. Businesses can decide whether to use it based on their needs.

- ITC for Buyers: Once the outward supply details are submitted through the IFF, they are reflected in the recipient’s GSTR-2A and GSTR-2B forms, allowing buyers to claim ITC without waiting for the full quarterly filing.

Benefits of Using the IFF

The IFF offers several benefits to both businesses and their buyers:

- Accelerated ITC Claims: Buyers can claim ITC sooner, improving their cash flow and reducing financial strain.

- Reduced Errors: By reporting sales data monthly, the IFF helps minimize discrepancies between suppliers and buyers, ensuring smoother reconciliation during quarterly filings.

- Simplified Compliance: The IFF reduces the filing burden for small businesses by allowing them to report sales data only for the first two months of the quarter.

Who Can Use the IFF?

A. Eligibility for the IFF

The IFF is available to taxpayers registered under the QRMP Scheme. Businesses must meet the following criteria:

- Annual turnover does not exceed ₹5 crore.

- They are enrolled in the QRMP Scheme for quarterly GST returns.

B. Who Benefits the Most?

- Businesses Issuing Regular Invoices: Companies with frequent outward supplies benefit by ensuring their buyers can claim ITC without delays.

- Taxpayers with Quarterly Filing Preferences: Those who prefer quarterly filings but need to maintain cash flow for their buyers find IFF highly useful.

C. Advantages of Using the IFF

- Timely ITC Availability: Buyers can claim ITC without waiting for quarterly filings, improving their cash flow.

- Reduced Compliance Stress: Businesses avoid the need for monthly GSTR-1 filings but still support their buyers.

- Minimized Errors: Regular updates ensure fewer mismatches during quarterly reconciliation.

- Flexibility: The optional nature of the IFF lets businesses decide whether to use it based on their needs.

- Customer Satisfaction: Ensuring timely ITC for buyers strengthens trust and fosters long-term business relationships.

Details to Submit in the Invoice Furnishing Facility (IFF)

The Invoice Furnishing Facility (IFF) is a focused mechanism for reporting sales invoices for the first two months (M1 and M2) of a quarter. While it is optional, businesses that opt to use the IFF must submit specific details related to their outward supplies. Here’s a breakdown of the required details:

What should be submitted to the IFF Scheme under GST?

- B2B Invoices: Details of taxable supplies made to registered buyers, including:

- GSTIN of the recipient.

- Invoice number and date.

- Taxable value and applicable tax rates (IGST, CGST, SGST, or CESS).

- Debit and Credit Notes: Any adjustments made to invoices for registered buyers.

- Amendments to B2B Invoices: Corrections or updates for invoices previously reported in earlier tax periods.

Note: The IFF does not require the reporting of B2C transactions or exempt supplies. These should be reported in the quarterly Form GSTR-1.

Criteria for Using the IFF

The IFF is an optional facility and not every taxpayer under the QRMP Scheme needs to use it. To determine whether you should submit IFF, consider the following criteria:

- Registered under QRMP: Only businesses enrolled in the QRMP Scheme are eligible to use the IFF.

- Invoice Reporting Needs: Use IFF if your buyers depend on timely ITC claims and you wish to provide those details in M1 and M2.

- Turnover Limit: The total value of outward supplies reported in IFF should not exceed ₹50 lakh per month.

- Optional Nature: If no outward supplies occur during M1 or M2, there’s no obligation to file IFF.

What is the Due Date for Filing IFF?

A. Due Date for Filing IFF

The Invoice Furnishing Facility (IFF) has a specific timeline for submission, aligned with the monthly GST process under the QRMP Scheme. For the first two months of a quarter, the due date for filing IFF is the 13th of the following month.

Here’s how it works:

- Month 1 (M1): The IFF for the first month of the quarter is due by the 13th of the second month (M2).

- Example: For April (M1) in Q1, the due date is 13th May.

- Month 2 (M2): The IFF for the second month of the quarter is due by the 13th of the third month (M3).

- Example: For May (M2) in Q1, the due date is 13th June.

- Month 3 (M3): No IFF is filed in the third month as all invoices for the quarter are consolidated in Form GSTR-1.

It’s crucial for businesses opting to use the IFF to adhere to these due dates to ensure their buyers can claim Input Tax Credit (ITC) without delays.

B. Consequences of Missing the IFF Due Date

- Impact on Buyers: Your buyers will face delays in claiming ITC, as the invoices will not reflect in their GSTR-2A or GSTR-2B until the GSTR-1 for M3 is filed.

- Reconciliation Issues: Missing the IFF deadline could lead to mismatches between buyer and supplier records, causing compliance complications.

- No Late Fee or Penalty for IFF: Since IFF filing is optional, there are no penalties or late fees for not filing it. However, the delay can affect business relationships due to ITC unavailability for buyers.

C. How to Avoid Missing the IFF Due Date

- Set Reminders: Ensure your accounting team or GST consultant tracks the 13th of every month as a key deadline.

- Prepare Invoices in Advance: Use accounting software to generate and manage invoices for seamless uploading.

- Use Notifications: Stay updated with GST notifications on due dates or extensions, if any.

By filing the IFF on time, businesses can ensure smoother ITC flow for their buyers, minimize compliance risks, and maintain strong business relationships.

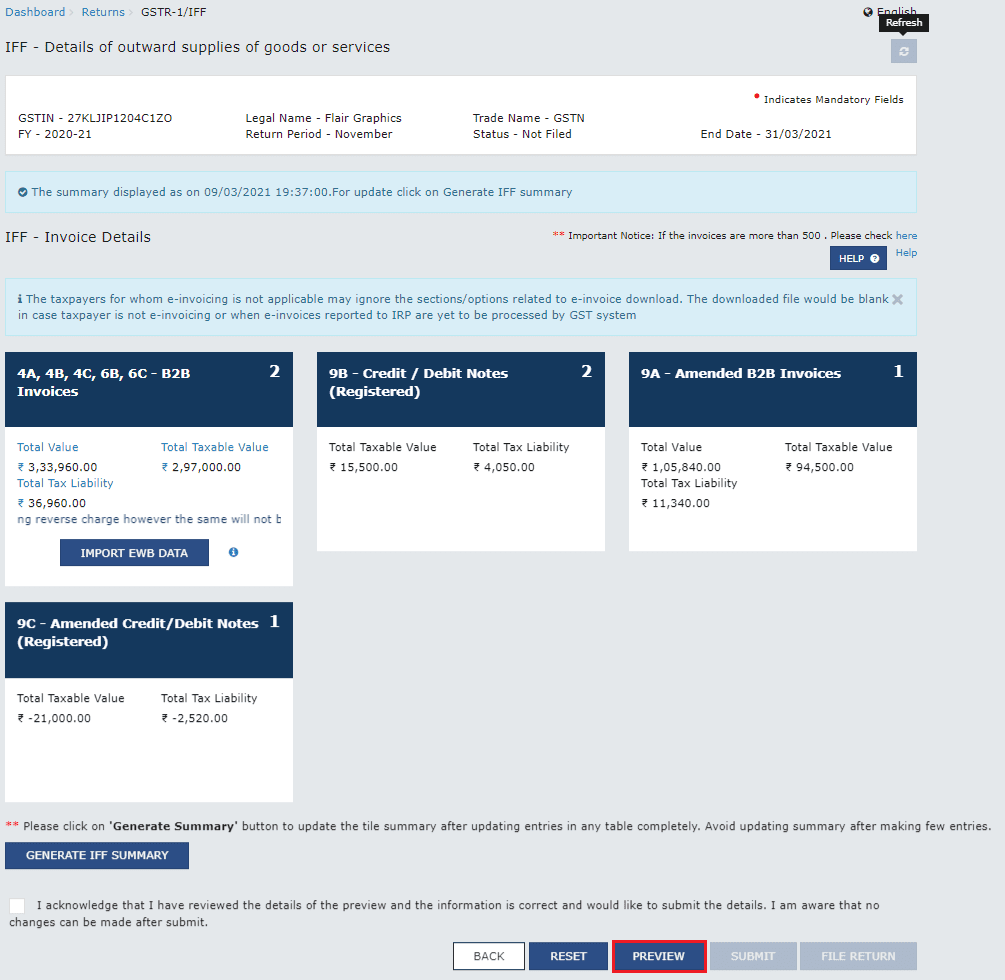

Steps to File IFF for M1 or M2 of a Quarter

- Visit GST Portal and log in with your credentials (username and password). Go to Services > Returns > Returns Dashboard.

- On the File Returns page, select the Financial Year, Quarter, and Month (M1 or M2). Click SEARCH. Under the Invoice Furnishing Facility tile, select:

- PREPARE ONLINE: To directly enter details on the portal.

- PREPARE OFFLINE: To upload a JSON file using the Returns Offline Tool.

B. Move Saved IFF Data to the Current Month

- If records were saved but not filed for M1 or M2, a new Move/Reset feature lets you:

- Move the saved data to the next period (M2 or M3).

- Reset (delete) the saved records and add new data.

- The Move Pop-Up appears only if:

- IFF for M1 or M2 was not submitted/ filed.

- Records exist in the previous month’s IFF.

- Note: Movement is limited to saved records within the same quarter.

C. Enter Details in Various Tables

1. Table 4A, 4B, 4C, 6B, 6C – B2B Invoices

- Click the tile to add invoices for taxable outward supplies to registered persons.

- Enter receiver details (GSTIN/UIN, invoice date, value, etc.) and specify the transaction type (e.g., SEZ, reverse charge).

- Save the details.

2. Table 9B – Credit/Debit Notes (Registered)

- Add details of credit or debit notes issued to registered recipients.

- Input GSTIN/UIN, note number, date, type (credit or debit), and values.

- Save the data.

3. Table 9A – Amended B2B Invoice

- Amend details of previously filed outward supplies.

- Select the financial year, input the invoice number, and update required fields.

4. Table 9C – Amended Credit/Debit Notes

- Amend credit or debit notes issued in earlier periods.

- Select the financial year, enter the note number, and revise as needed.

D. Generate IFF Summar

- Click GENERATE IFF SUMMARY to update the summary after entering details. Summaries are auto-generated every 30 minutes or can be manually triggered every 10 minutes.

- Once the summary is generated, a success message will appear.

E. Preview IFF

- Click PREVIEW to download a draft summary of the Form IFF in PDF format. Review the entries before submission.

- The draft document will have a watermark indicating it is not final.

F. Acknowledge and Submit IFF

- Select the acknowledgment checkbox to confirm the accuracy of the details.

- Click SUBMIT to freeze the uploaded data. No further changes can be made for that month after submission.

Note: If taxable values exceed prescribed limits, an error message will appear. Adjust and resubmit.

G. File Form GSTR-1/IFF Using DSC or EVC

- Click FILE RETURN. On the Returns Filing page:

- Select the declaration checkbox.

- Choose an authorized signatory.

- File using:

- DSC: Select the certificate and sign.

- EVC: Verify using OTP sent to the registered email and mobile.

- Upon successful filing:

- A success message with an ARN is displayed.

- Status changes to “Filed.”

- A final PDF can be downloaded.

This process ensures the timely furnishing of outward supply details and seamless credit transfer to recipients.

Pre-requisites for Filing Invoice Furnishing Facility (IFF)

Before filing the Invoice Furnishing Facility (IFF), ensure the following conditions are met:

1. Registration Under QRMP Scheme

- The taxpayer must be registered under the Quarterly Return Monthly Payment (QRMP) Scheme.

- Businesses with an annual turnover of up to ₹5 crore are eligible for the QRMP Scheme and, therefore, for IFF.

2. Active GSTIN

- A valid and active GSTIN (Goods and Services Tax Identification Number) is mandatory for filing the IFF.

3. Access to the GST Portal

- The taxpayer must have login credentials for the GST portal (www.gst.gov.in) to access the IFF filing section.

4. Valid Invoices

- Details of B2B invoices, including:

- Recipient GSTIN.

- Invoice number and date.

- Taxable value and applicable taxes (IGST, CGST, SGST, or CESS).

- Debit and Credit Notes, if applicable.

- Amendments to previously reported invoices, if needed.

5. Monthly Outward Supply Limit

- The value of outward supplies reported in IFF must not exceed ₹50 lakh per month.

6. Filing Timeline

- The IFF can only be filed for the first two months of a quarter (M1 and M2).

- The due date is the 13th of the following month (e.g., IFF for April must be filed by 13th May).

7. Digital Signature or OTP

- Filing requires either:

- A Digital Signature Certificate (DSC) for authorized signatories.

- An Electronic Verification Code (EVC) sent to the registered mobile number and email.

8. No Pending Returns

- The taxpayer must ensure there are no pending GST returns (such as GSTR-3B or previous GSTR-1) for prior periods.

These pre-requisites ensure smooth filing of the IFF, helping taxpayers meet compliance requirements and enable their buyers to claim ITC promptly.

Will Invoices Reported in IFF Reflect in My Recipient’s Form GSTR-2A/2B?

Yes, invoices reported in the Invoice Furnishing Facility (IFF) are reflected in the recipient’s Form GSTR-2A and GSTR-2B. This is one of the primary advantages of using the IFF, as it ensures that your buyers can claim Input Tax Credit (ITC) promptly. Here’s how it works:

Form GSTR-2A:

Once you file the IFF, the details of the outward supplies are automatically reflected in your recipient’s GSTR-2A on a near real-time basis.

This helps the recipient reconcile their purchase records with your reported sales.

Form GSTR-2B:

The invoices reported in the IFF are also included in the recipient’s GSTR-2B, which is a static ITC statement generated for the recipient on the 14th of every month. This allows them to claim ITC without delays.

Example: If you submit the IFF for April (M1) by 13th May, the recipient will see these invoices in their GSTR-2B for May, generated on 14th May.

Note: Timely filing of IFF is critical, as any delay will prevent the invoices from appearing in the recipient’s GSTR-2A/2B until the quarterly GSTR-1 is filed.

Provisions Governing the Invoice Furnishing Facility (IFF)

The Invoice Furnishing Facility is governed by specific provisions under the Central Goods and Services Tax (CGST) Rules, 2017, particularly those related to the QRMP Scheme. Here are the key provisions:

- Optional Nature:The IFF is not mandatory; it is an optional facility available to taxpayers registered under the QRMP Scheme.

- Turnover Limit:Only taxpayers with an annual aggregate turnover of up to ₹5 crore are eligible for the QRMP Scheme, and hence for the IFF.

- Value Limit:The total value of invoices reported in IFF for a month cannot exceed ₹50 lakh.

- Reporting Period:IFF can only be used for the first two months (M1 and M2) of a quarter. For the third month (M3), all outward supplies must be reported in Form GSTR-1.

- Visibility in GSTR-2A and 2B:Invoices submitted through IFF are automatically reflected in the recipient’s GSTR-2A and GSTR-2B, helping facilitate timely ITC claims.

- No Penalty for Non-Use:There are no penalties for not using the IFF or for delayed submission. However, the facility becomes inaccessible after the due date (13th of the following month).

These provisions ensure that the IFF serves as a flexible tool for small taxpayers, providing them with the benefits of timely reporting without imposing additional compliance burdens.

Conclusion

The Invoice Furnishing Facility (IFF) is a valuable addition to the GST compliance framework, offering flexibility and efficiency for small businesses under the QRMP Scheme. By enabling timely reporting of outward supplies in the first two months of a quarter, the IFF ensures buyers can claim Input Tax Credit (ITC) promptly, improving cash flow and fostering stronger business relationships.

Although optional, its use can significantly reduce compliance stress, minimize errors, and enhance trust with buyers. For businesses aiming to simplify GST processes and support their buyers, leveraging the IFF is a strategic step toward smoother operations and financial stability.

FAQs

Can I File IFF After the Due Date?

No, the IFF cannot be filed after the due date. Once the deadline (13th of the following month) passes, the facility for that month is disabled. If you miss the IFF deadline:

- The details of outward supplies for M1 and/or M2 can only be reported in the quarterly Form GSTR-1 for M3.

- This delay may affect your buyers, as they won’t see your invoices in their GSTR-2A/2B until the GSTR-1 for M3 is filed.

Do I Need to File Invoices in M1 and M2 Every Quarter?

No, filing invoices in M1 and M2 using the IFF is not mandatory. It is entirely optional under the QRMP Scheme. Taxpayers can choose whether to use the IFF based on their specific requirements. Scenarios where filing IFF may not be necessary:

- No outward supplies in M1 or M2.

- Buyers do not require ITC during these months.

- You prefer to report all outward supplies directly in the quarterly Form GSTR-1.

Is there any late fee applicable on late filing of IFF?

No, there is no late fee for delayed or non-filing of IFF, as it is optional. However:

- Buyers will face ITC delays until the quarterly GSTR-1 is filed.

- Missed deadlines can lead to reconciliation issues and affect business relationships.

Related Posts:

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

A Complete Guide to the Types of Invoices

A Complete Guide to the Types of Invoices

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

Understanding the Structure of GST: Simplifying Compliance and Driving Growth in India

Understanding the Structure of GST: Simplifying Compliance and Driving Growth in India

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

Zatca Compliant E-Invoices: A Detailed Guide for Businesses in Saudi Arabia

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS